Last week we covered SOFR First in Swaptions and did so the day after the November 8th commencement date. Now that we have more data, let’s look at what this shows.

Week One – SOFR Swaptions

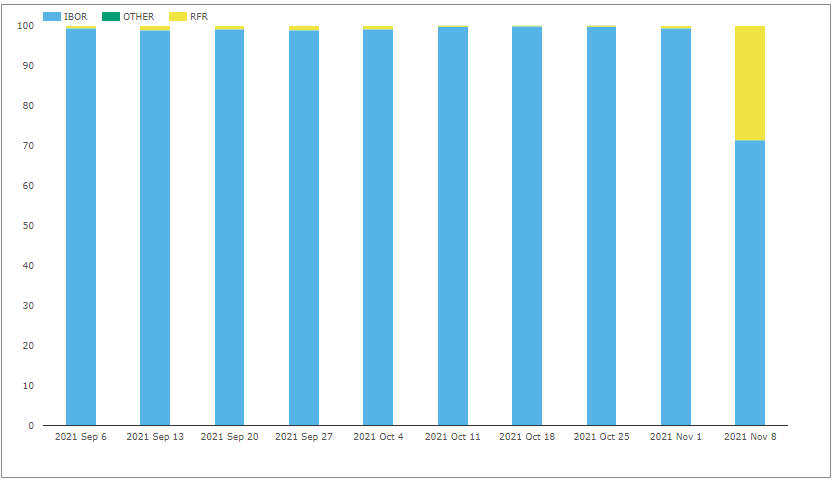

In SDRView Researcher, we select USD Swaptions and categorize by reference index as IBOR or RFR.

Showing that in the week starting November 8th, 29% of volume (notional terms) was in SOFR Swaptions, a huge jump from under 1% in prior weeks. (In trade count terms it was 22%).

(Before anyone gets excited about the Other legend, I need to clarify that this is bad data, someone reporting a couple of Off SEF trades and not populating the underlying with any floating rate option).

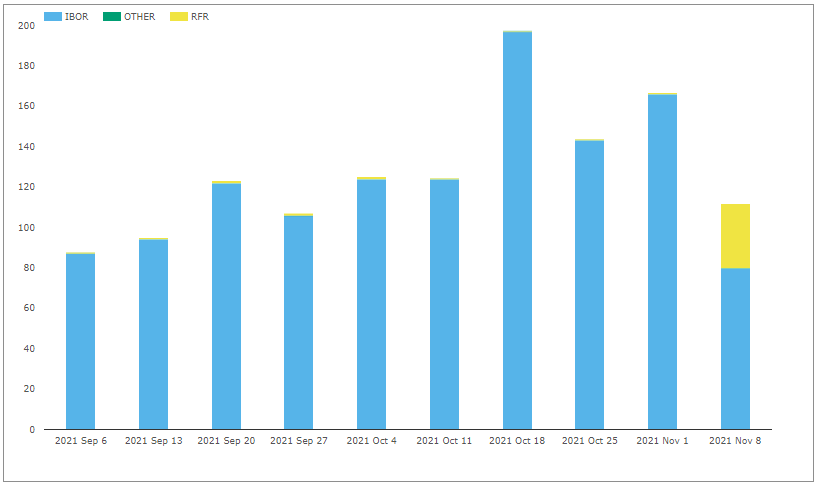

And changing the above chart to show gross notional by week.

Showing that while volumes were lower last week (due to the November 11, Veterans Day holiday), over $32 billion of SOFR Swaptions traded, compared to $80 billion of USD Libor Swaptions.

Inter-Dealer Volume

We noted in last week’s blog that under the CFTC MRAC SOFR First for non-linear derivatives initiative:

- interdealer brokers were encouraged to change conventions to SOFR

- dealers encouraged to specify physical settlement

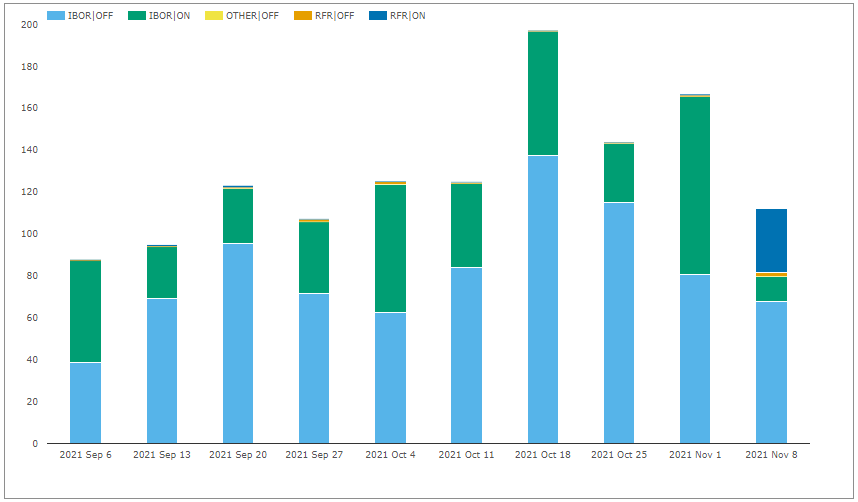

So let’s further categorize our volume into Ref Index and On/Off SEF.

The new navy blue stack in the Nov 8 bar showing the jump in On SEF SOFR volumes to $30.5 billion, which is greater than the dark green stack of On SEF Libor volumes of $12 billion.

Given that On SEF Swaptions volume is all from the D2D Brokers (BGC, IGDL, TP, Tradition), we can agree that it is indeed the inter-dealer volume that has moved to SOFR.

While Off SEF volume last week was $68 billion Libor and $2 billion SOFR.

Remember all these notionals above are subject to capped notional rules, resulting in an understatement of the actual notional transacted. Using SEFView, we can get the actual On SEF notional traded and a breakdown by each venue, but as time is short before my deadline, will leave that to another day.

The ISDA definitions are now updated and the SOFR ICE Swap Rate is being published daily.

However the lack of any field on the SDR public dissemination to distinguish physical from cash settlement means we cannot tell if the market convention of inter-dealer trades is now physical settlement (i.e. on exercise you get the swap) as opposed to cash settlement.

Expiry and Tenors Traded

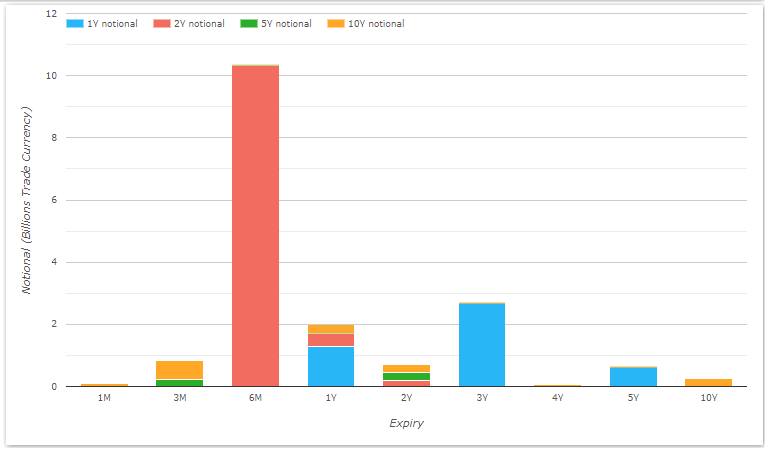

In SDRView Professional, we can get a matrix of expirys and tenors traded on a specific date or in a period.

Showing the volume of $18 billion on November 10, 2021, categorized by expiry and tenor:

- 6M into 2Y by far the largest with $10 billion from 27 trades, all payers or receivers

- 3Y into 1Y with $3 billion from 7 trades, all straddles.

- 1Y into 1Y, 2Y, 10Y with $2 billion.

- Expirys ranging from 1M to 10Y

- Tenors of 1Y, 2Y, 5Y and 10Y

- (there is detail on the strikes and premiums of each trade, in the drill-downs)

So we are seeing trades in many points of a Swaption Vol Cube

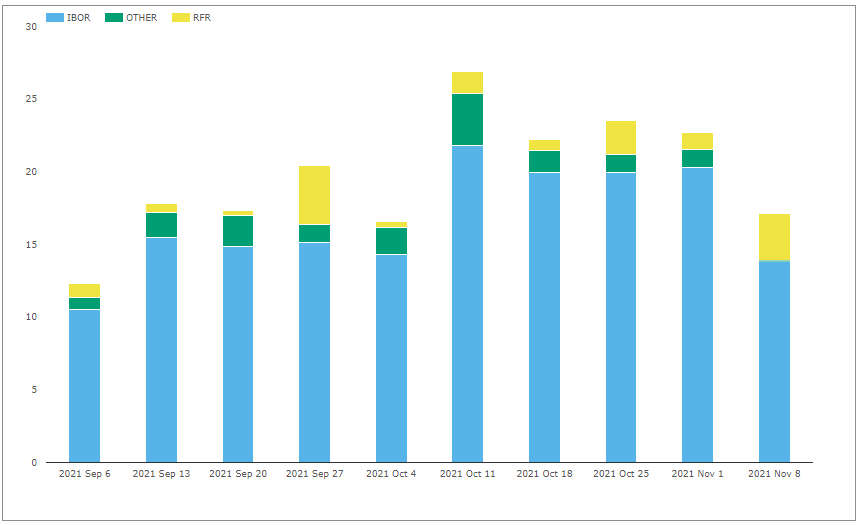

Caps and Floors

Next another non-linear derivative product, CapFloors, smaller than Swaptions but important nonetheless.

Showing that out of the overall volume of $17 billion in the week of November 8-12, $3 billion or 19% was linked to SOFR. A few other interesting points to note here:

- SOFR CapFloors have been trading each week for a while now

- They reference either a SOFR 30-Day Average Rate or the usual daily SOFR

- And while ON SEF trading in SOFR did jump last week, there has been reasonable volume Off SEF each week prior to that, driven by market/customer demand

- The Other in the charts includes FedFunds, NYFed30, SIFMA Muni, CMS and BSBY

That’s all for today.

We will keep an eye on how non-linear RFR volumes progress.