- With Average Daily Volumes of $10bn in 2025, trading 200 times per day, KRW swaps are the 14th largest market (outside of the G6 major currencies).

- The swaps market is split across onshore and offshore products, with up to 95% of volumes cleared in 2025.

- The offshore market, settled in USD, appears to be much larger than the onshore market, with both LCH SwapClear (for clearing) and Tradeweb (for execution) major players.

Where do KRW Swaps Rank on the Global Picture?

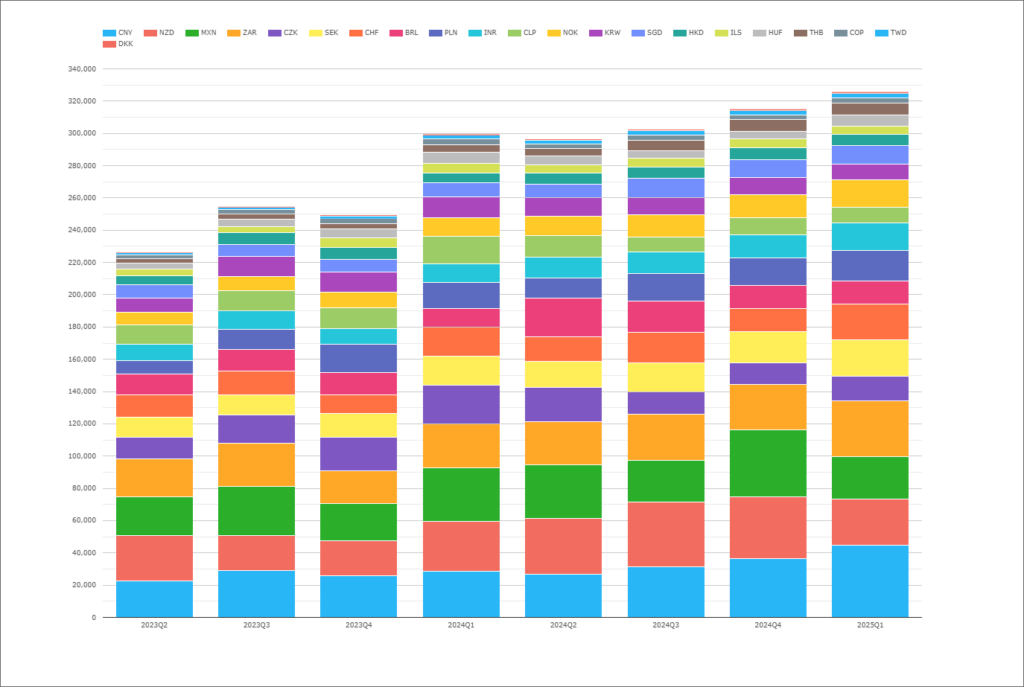

CCPView allows us to compare the relative size of KRW swap markets to other currencies. Taking out the “G6” – USD, EUR, GBP, AUD, CAD and JPY – we see the below:

Showing;

- Average Daily Volumes (ADVs in $m) in Cleared Interest Rate Derivatives from CCPView.

- The chart excludes the top six currencies by volumes (USD, EUR, GBP, JPY, AUD and CAD). These six currencies represent over ~95% of total cleared volumes (see Four Trends in Swaps Data).

- For the volumes displayed on the chart (not total cleared volumes), KRW represents 3-5% of ADVs, and sits as the 14th most traded swaps market in Q1 2025.

- Looking at other markets, CLP has seen similar volumes in 2025, whilst THB is some 25% smaller than its neighbour.

- The market would have to grow by 55% to reach the “top 10” of these other currencies.

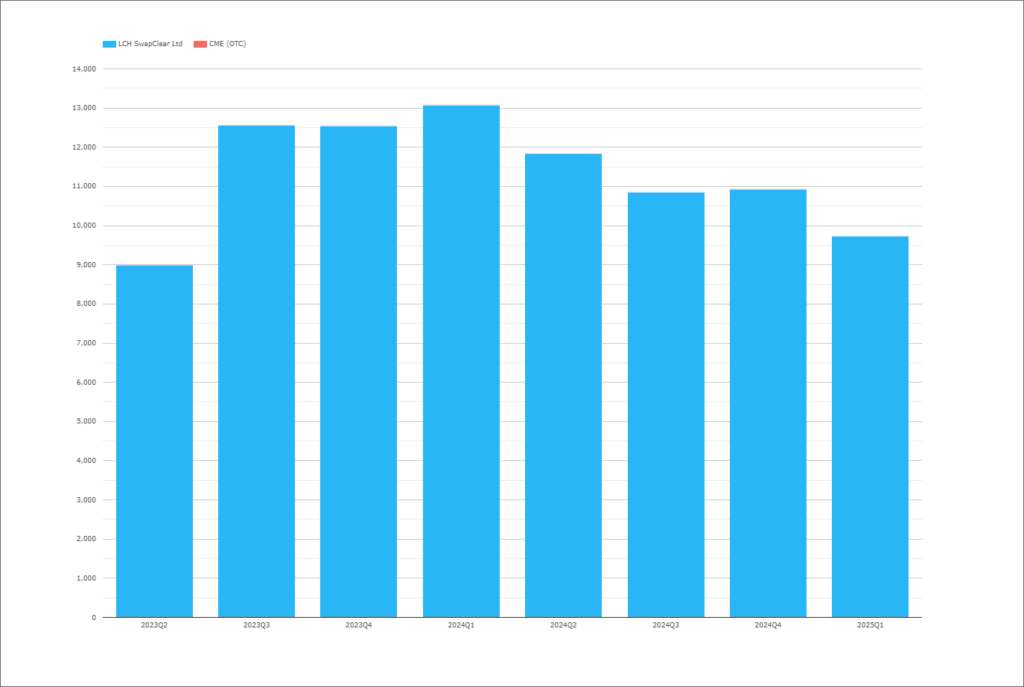

Are All Volumes Cleared at LCH SwapClear?

Our CCPView data shows that almost all KRW swaps are cleared at LCH. Whilst CME do offer KRW clearing, there are rarely any volumes:

Showing;

- Unusually for a Clarus blog, we are not talking about “all time record volumes”.

- Maybe that makes this chart particularly interesting? Why have Rates volumes not accelerated in KRW like they have in other markets over the past couple of years?

- Difficult one to answer – readers thoughts are welcome in the comments section below!

Well educated market participants may notice that the chart looks at only offshore clearing. KRX Clearing, a Korea-based CCP, caters for the onshore market and just last year announced that they have cleared over 2,000 Trn KRW (equivalent to $1.5Trn) in the past ten years.

How does this compare to our offshore data? LCH SwapClear cleared well over $3Trn equivalent in 2024 alone, and has an Open Interest over $1.5Trn. This therefore suggests that the offshore market is much larger than the onshore market – potentially 20 times larger.

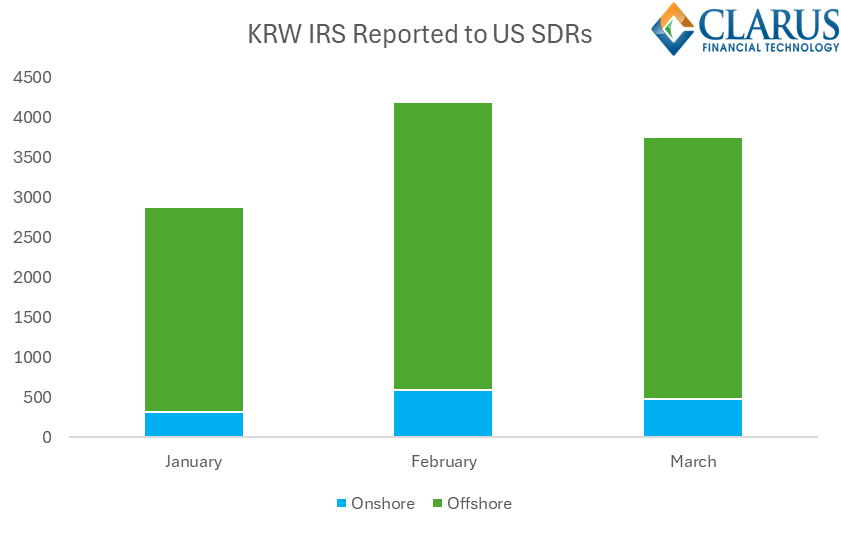

We also see KRW-settled IRS reported to SDRs – i.e. onshore swaps. However, at least 87% of KRW swaps reported to SDRs in 2025 have had a settlement currency of USD:

It is unsurprising to discover an offshore bias for trades reported to US SDRs. But it would be super helpful to have KRX data in CCPView, providing an accurate representation of the global market. We plan to follow up with KRX to see if we can incorporate their volume data in CCPView.

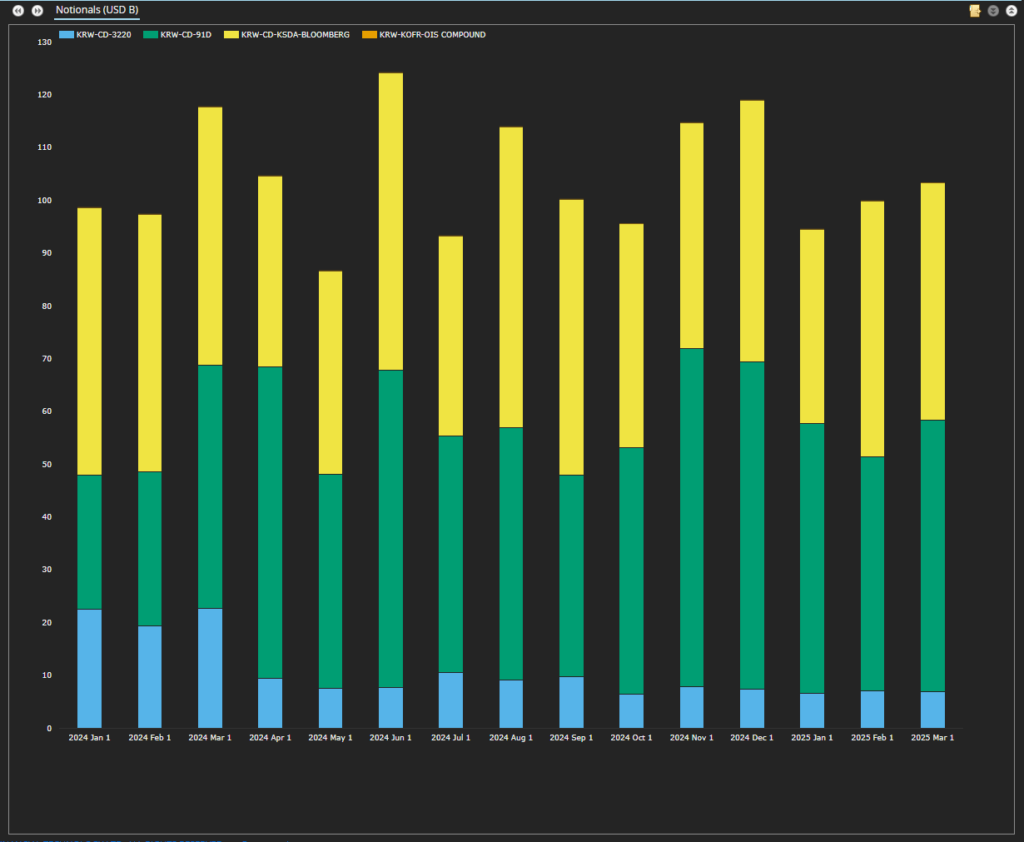

What Product Trades in KRW Swaps?

When Tod previously looked at KRW swaps, he stated:

These appear to be the same conventions whether a swap is traded onshore or offshore. The only difference is whether the cashflows are settled in KRW (onshore) or converted at a standard FX fixing into USD (offshore). LCH only clear Non-Deliverable Swaps (NDIRS) for KRW and hence settle all payments (margin and contractual cash-flows) in USD (The precise FX fixing being used is surprisingly hard to find. Any readers care to submit the source in the comments please?).

Tod’s blog was published way back in 2017. Have KRW markets managed to transition away from a term rate in the meantime?

Showing;

- Not much appears to have changed – all swaps are still traded versus a term “CD-KSDA” index.

- There is apparently a fledgling OIS market, with the odd trade reported.

- I wonder if this is a case of chicken vs egg – the market waiting for LCH to start clearing KRW OIS?

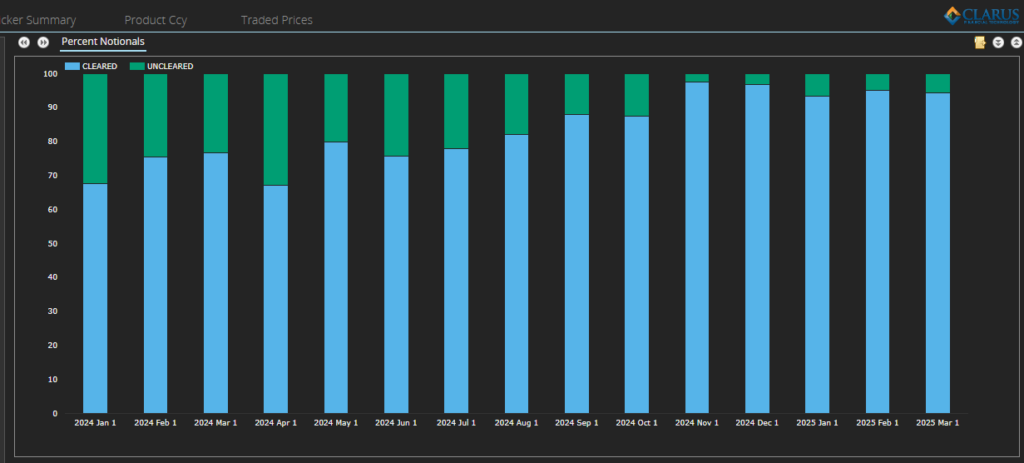

Most KRW Swaps are Cleared

95% of the market is now cleared;

Showing;

- Clearing has increased from 67% to 95% over the past 18 months alone.

- That is an impressive move over such a short period of time!

The Uncleared Margin Rules went into effect in 2021 for Korean entities, so this does not appear to be a move caused by regulations. As Tod reported back in 2017, banks should be incentivised by the UMRs to move exposures to CCPs, increasing netting opportunities and avoiding grossing-up Initial Margin positions. But why the recent appetite for Clearing is somewhat puzzling – there doesn’t appear to be any change in the status of KRX, and the CFTC website only references KRX in terms of KOSPI futures, not OTC clearing.

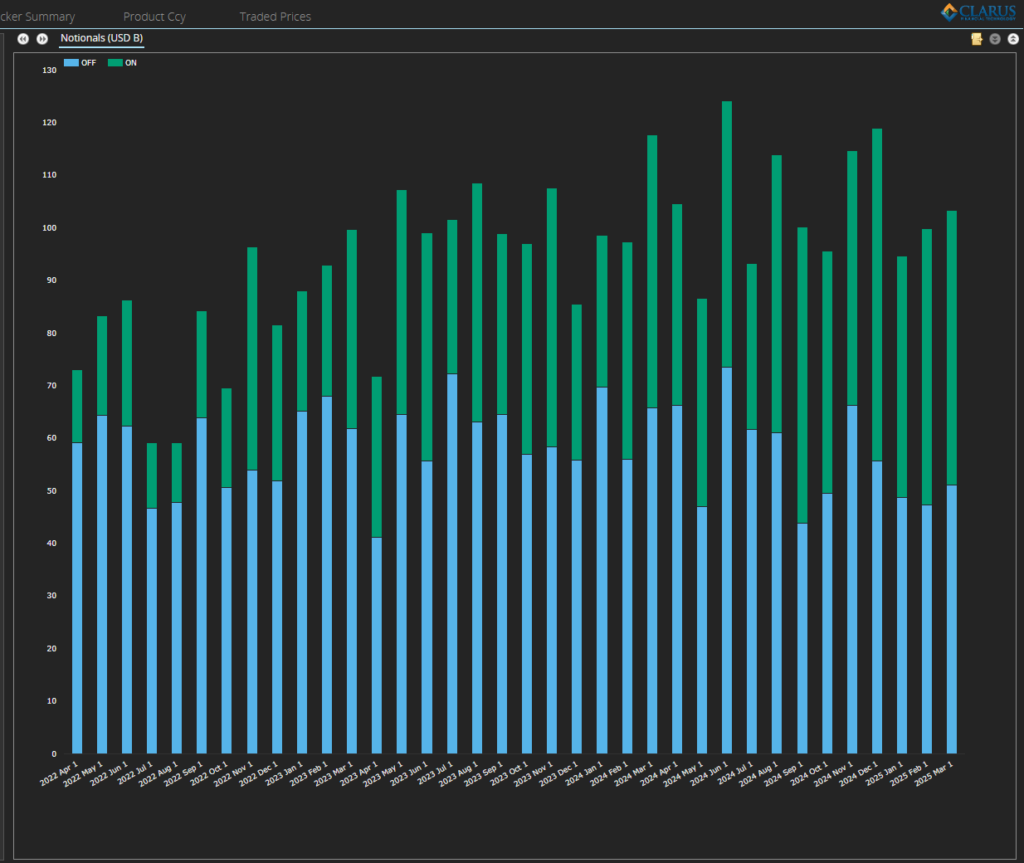

There is a healthy SEF Market in KRW!

The popularity of SEFs, largely for their workflow benefits, has been a real feature in this series of blogs. I am pleased to report this is no different for KRW. SEF trading now makes up a significant portion of volumes:

Showing;

- SEF trading becoming more popular.

- 2022 saw about 75% of notional executed off-SEF.

- 2025 has now seen 50% of notional executed on a SEF.

Tradeweb make up the vast majority of these volumes, with very little reported on a SEF in D2D markets. This is somewhat similar to the story we saw for CNY swaps, another market with onshore/offshore dynamics.

In Summary

- Global Market Positioning: KRW swaps are the 14th most traded cleared swaps market outside the top six global currencies, contributing 3–5% of average daily volumes (ADVs) in Q1 2025. To break into the top 10, KRW volumes would need to grow by approximately 55%.

- Clearing & Market Structure: Nearly all offshore KRW swaps are cleared at LCH (as Non-Deliverable Interest Rate Swaps settled in USD), with minimal activity at CME. Although Korea’s domestic CCP, KRX, has cleared $1.5 trillion over the past decade, LCH cleared over $3 trillion in 2024 alone—suggesting offshore dominance. Most swaps still reference the term “CD-KSDA” index, with limited uptake of OIS.

- Trading Trends & Transparency: The cleared proportion of KRW swaps has surged from 67% to 95% in just 18 months, likely due to market preference rather than new regulation. SEF trading has also risen, with 50% of volumes now executed on SEFs in 2025 (mainly via Tradeweb), indicating a maturing and increasingly transparent offshore market.