Derivatives innovation: Swap Connect and CNY swaps

This blog looks at Swap Connect, a service enabling offshore parties to trade and clear deliverable CNY swaps. Key takeaways Read on for Swap Connect’s market impact and the unique features of its trade acceptance approach, booking model and margin process. All the charts, data, and statistics in this blog were sourced from CCPView. CNY […]

What’s new in JPY swaps in 2025?

Following our blog in April 2024, we further explore the volume expansions and market transitions in JPY IR derivatives. Key takeaways Cleared OTC interest rate derivatives (IRD) volumes As noted in our quarterly CCP IRD volumes blog, JPY IRD volumes exploded in 2024 and 2025. I wanted to look over a longer period to see […]

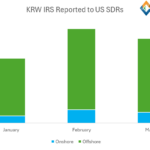

What You Need to Know About KRW Swaps

Where do KRW Swaps Rank on the Global Picture? CCPView allows us to compare the relative size of KRW swap markets to other currencies. Taking out the “G6” – USD, EUR, GBP, AUD, CAD and JPY – we see the below: Showing; Are All Volumes Cleared at LCH SwapClear? Our CCPView data shows that almost all […]

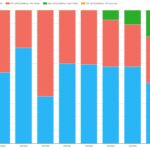

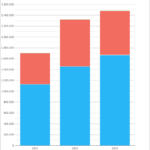

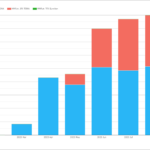

CNY Swaps – What’s New?

When I last wrote about CNY Swaps back in 2020, I found that CNY swaps were the 9th most traded currency in cleared Interest Rate Derivatives. They have since increased in size significantly, and are now the 7th largest swaps market. Updating the data from CCPView; Showing; CCP Market Share CNY is one of the seven […]

INR Swaps – What’s New?

This will be my last blog of the year, and the last one before we get into some retrospectives about 2024. It is therefore a good opportunity to add to the “What’s New” series, and look at INR swaps. Unlike MXN, which had a near five-year gap between blogs (!), I wrote about INR swaps […]

JPY Swap Clearing – Why do dealers prefer JSCC?

And equally “Why do clients prefer SwapClear?” The Data It was only recently that I provided a general overview of the JPY Swaps Market in 2024. As so often happens, that blog sparked some conversations, which sparked some number crunching, leading us here. Last time, I noted that the JSCC-LCH basis had shown a significant […]

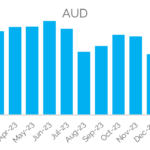

What’s New in AUD Swaps in 2024?

With so many AUD blogs behind us, I figured it was high time we started adding dates to the titles – otherwise I’ll never remember what I wrote and when! The previous AUD articles are linked below: These blogs are quite enjoyable to write, as it gives me an opportunity to “surf” the data and pull […]

What’s New in JPY Swaps in 2024?

Covering; ISDA AGM in Tokyo I thought I would try to be helpful with the timing of this blog. The ISDA AGM is due to take place April 16-18 in Tokyo: Most delegates will take time to also see Tokyo-based clients, and will therefore be discussing the JPY swap market whilst doing so. So consider […]

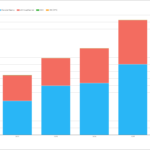

What You Need to Know About INR Swaps

Where do INR Swaps Rank on the Global Picture? CCPView allows us to compare the relative size of INR swap markets to other currencies. Taking out the “G6” – USD, EUR, GBP, AUD, CAD and JPY – we see the below: Showing; Let’s look further into the INR Swaps market. Two Thirds of Cleared Volumes are […]

JPY TONA Futures: A Rising Star in the RFR Market

*I hope our readers don’t mind, but I chose to accept a little help from Bard this week. With so much web traffic generated via Google searches, I thought it a worthwhile experiment. TIBOR Cessation No two markets are the same, and we see this in the adoption of RFR trading. Whilst JPY LIBOR is […]