- We look at continued growth in cleared NDF volumes.

- NDFs now see over $2Trn in Open Interest.

- Average Daily Volumes are now greater than $65bn.

- NDFs in 5 currency pairs dominate cleared OTC volumes.

NDF Cleared Volumes

CCPView shows that cleared NDF volumes continue to grow:

Showing;

- Average Daily Volumes are hitting successive new highs as 2024 evolves.

- Up to the last week of September, we now see ADVs over $65bn in cleared NDFs. This excludes FX Options and Forwards.

- As we have noted in the past, March is normally the most active month. This year we have seen the March peak surpassed in August and so far in September in terms of Average Daily Volumes.

- LCH ForexClear has a 99%+ market share in NDF clearing.

- Comder volumes in USDCLP have reduced substantially. We haven’t seen a notable increase at ForexClear in USDCLP, with volumes pretty steady since last Summer. What gives?

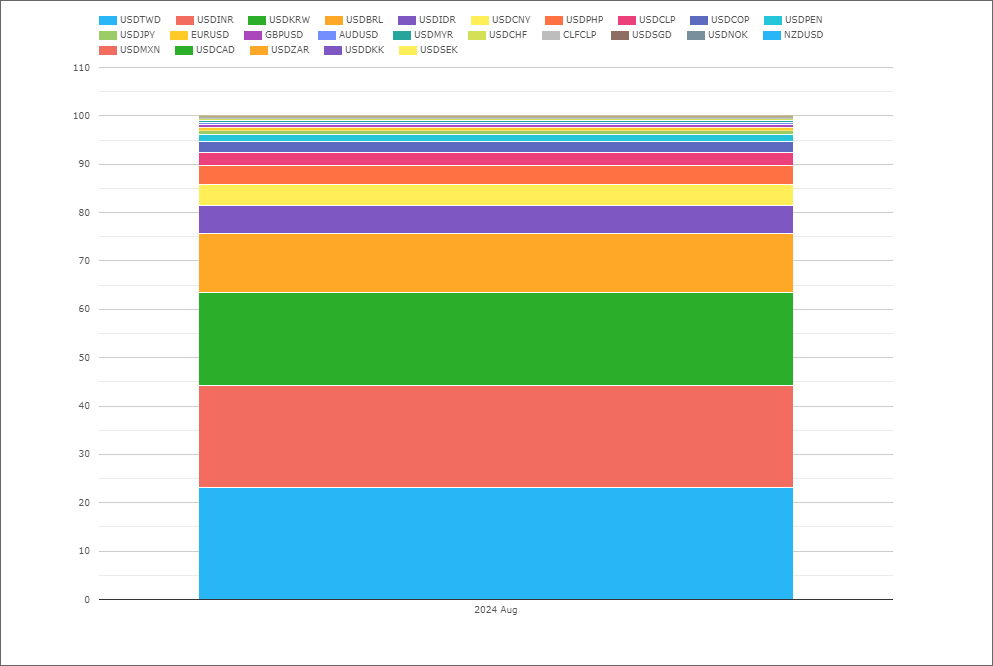

Which NDF Currency Pairs are the largest?

Looking into the August 2024 data per currency pair shows:

- 23% of volume in TWD

- 21% is in INR

- 19% in KRW

- 12% in BRL

- 5% each in CNY and IDR

- 4% in PHP. I won’t go on!

- 85% of volumes are in the 5 largest currency pairs.

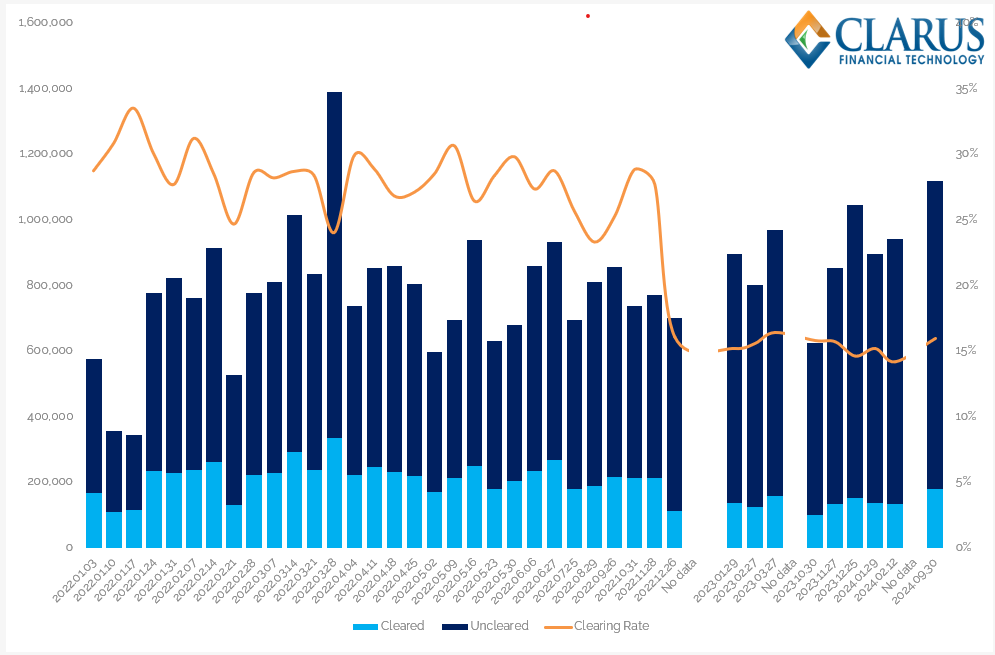

NDF Clearing Rates

Regular readers will know that we use the CFTC weekly Swaps Report to monitor how much of the NDF market is cleared. The large increase in volumes has typically resulted in Clearing Rates going higher – i.e. more of the overall market being cleared. However, this trend suffered a set-back in 2023 when the data methodology appeared to change:

Showing;

- Weekly traded USD notional equivalents as reported in the CFTC swaps report for FX product type “NDF”.

- Historically, these volumes tended to reconcile with our own CCPView data. Since 2023 this has not been the case.

- In terms of numbers;

- Historically, Clearing Rates were as high as ~30% according to the CFTC data.

- However, since 2023 the data has suggested a very stable rate at 15%.

- This coincided with a note published in the data file, stating:

“Methodology changes are too numerous to fully list in this note, we outline a few of the more significant adjustments below. Improvements include:

CFTC Weekly Swaps Report

- Better identification of duplicative records across SDRs

- Updated inter-affiliate identifications

- More extensive tracking of swap lifecycle events, such as allocations or compressions

- Other data cleaning and data standardization efforts”

It is difficult to ascertain which of these data changes has caused the apparent drop in Clearing Rates (the reported CFTC cleared volumes are now much lower than our total cleared figures in CCPView). Are inter-affiliate trades a big proportion of NDF clearing and trading? It would seem strange for a bank to choose to post Initial Margin and default fund contributions to a CCP just for internal trades. If anyone has an insight, please drop it in the comments below.

Thankfully, the CFTC published their first updated Swaps Report in over six months this week, so we can monitor the data.

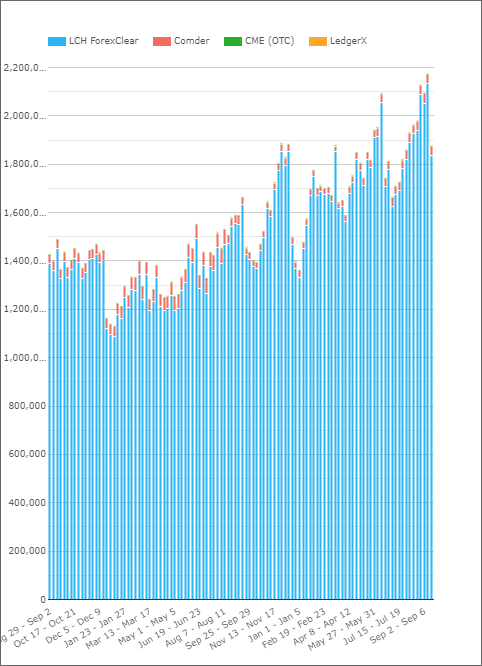

Risk in NDFs

Putting doubts over the Clearing Rate aside, the record volumes are certainly resulting in more risk being cleared. The Open Interest in NDFs has hit new records, recently surpassing $2Trn for the first time:

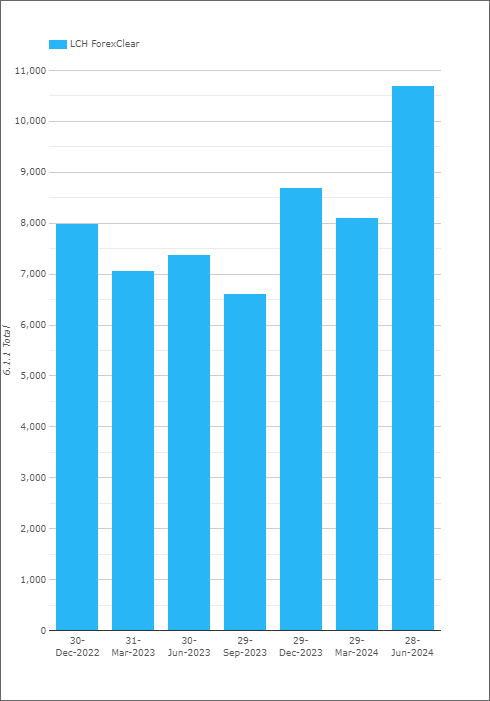

Up until June 2024 (the latest data), that also means there is more and more Initial Margin being posted at ForexClear:

These large increases have mainly been driven by House IM, which has increased from $6bn to $9.4bn. Client IM has also increased, but from a low base ($0.6bn to $1.2bn).

In Summary

- Cleared NDF volumes continue to increase, with Average Daily Volumes in excess of $65bn.

- Open Interest has recently surpassed $2Trn for the first time.

- Initial Margin related to cleared OTC FX is now greater than $10bn.