Central Counterparties recently published their latest CPMI-IOSCO Quantitative Disclosures and in this article I will highlight a few of the key trends, similar to my article on 3Q 2016 trends.

Background

Under the voluntary CPMI-IOSCO Public Quantitative Disclosures by CCPs, over two hundred quantitative data fields covering margin, default resources, credit risk, collateral, liquidity risk and more are published each quarter with a quarterly lag.

CCPView now has six sets of quarterly disclosures, from 30 Sep 2015 to 31 Dec 2016 inclusive, which means we can observe both trends over time at one CCP and compare CCPs to each other.

Lets take a look at some of the main disclosures.

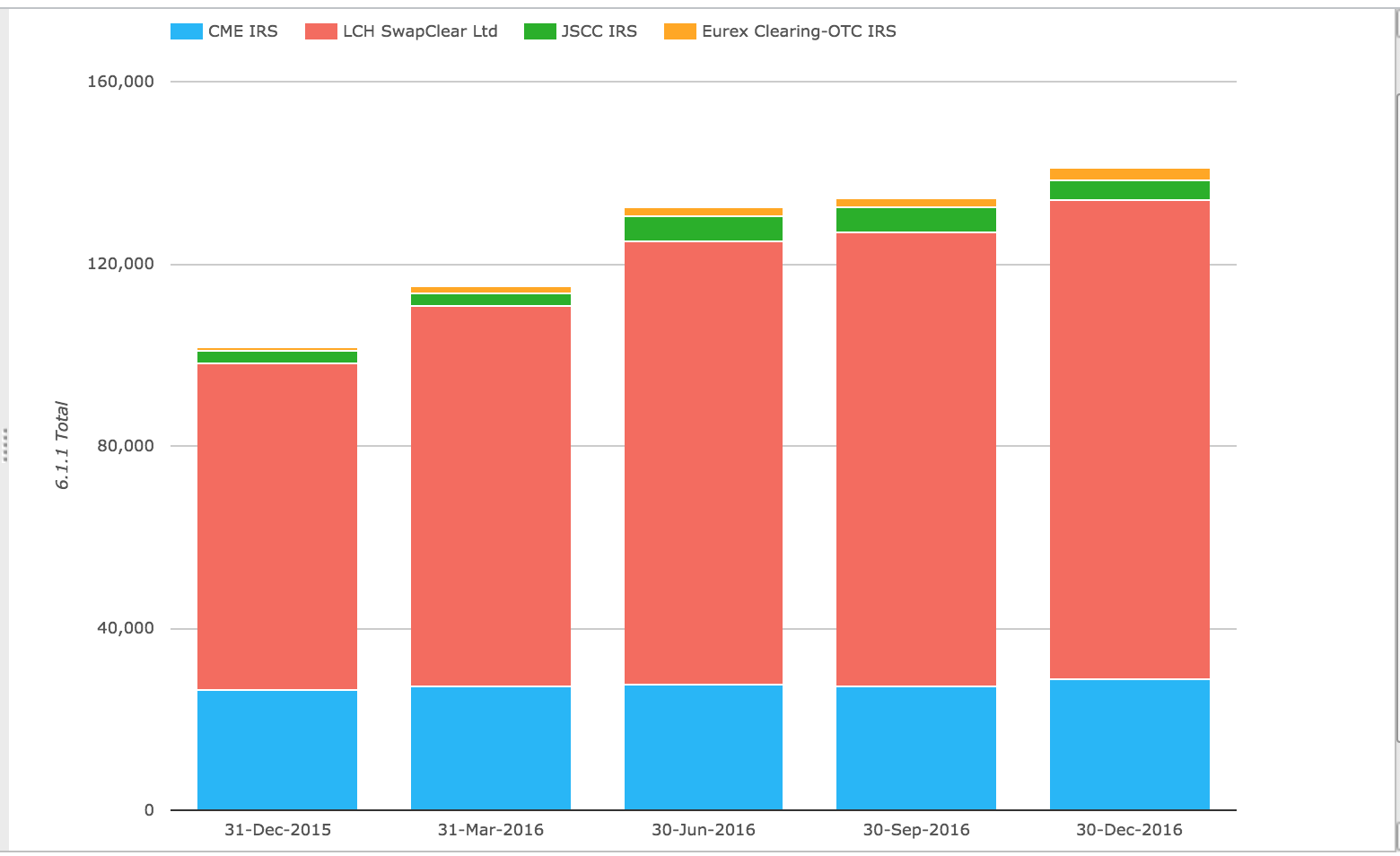

Initial Margin for IRS

Starting with the Initial Margin requirement for Interest Rate Swaps.

Showing:

- Total IM for these four CCPs was $141 billion on 30-Dec-2016

- Up from $134 billion on 30-Sep-2016, an increase of 5% (in USD)

- Up from $101.7 billion on 31-Dec-2015, an increase of 39% (in USD)

- LCH SwapClear is by far the largest with $105 billion

- CME IRS is next with $28.8 billion, up from $27.2 billion on 30-Sep-2016

- JSCC IRS with $4.5 billion is down from the $5.5 billion on 30-Sep-2016

- Eurex Clearing OTC IRS at $2.5 billion is up from $2 billion on 30-Sep-2016

While Initial Margin at a single point in time is influenced by many factors in the period (new volume, compression, volatility), it is a good measure of the relative size and systemic importance of a CCP.

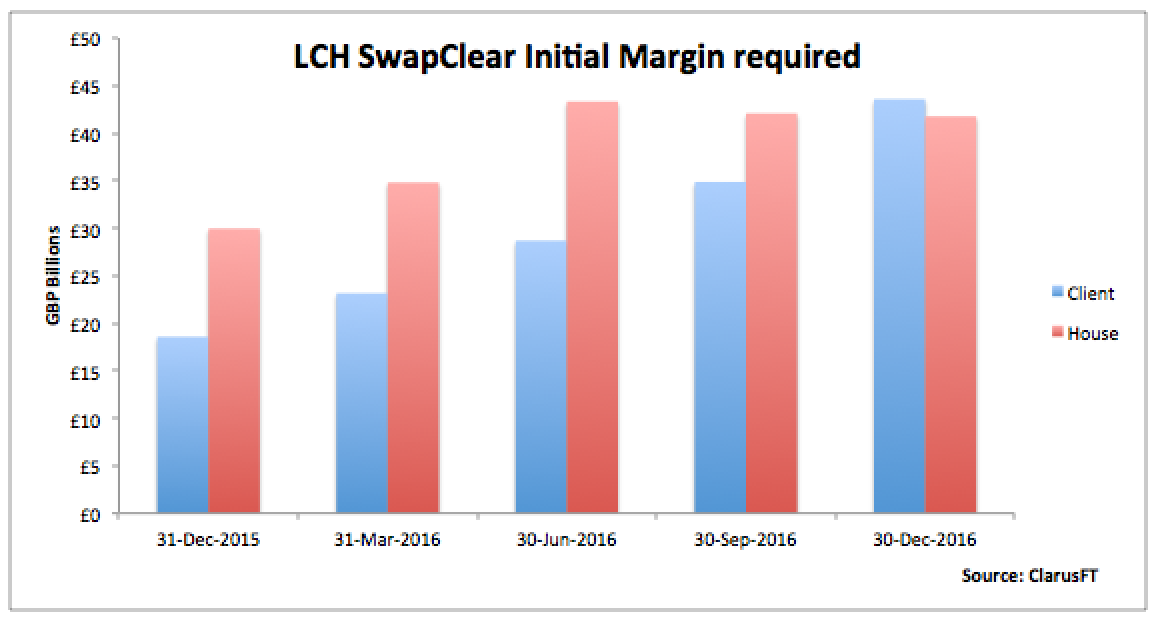

An interesting observation and one that I highlighted in my article in Risk.net, Swaps Data: ETD vs OTC, is that LCH SwapClear Client Margin has for the first time exceeded House Margin.

Showing that LCH SwapClear Client IM has grown 135% in 2016 (in GBP terms) to reach £43.5 billion, while House IM has grown 40% over the same period to reach £41.8 billion.

We expect this trend in Client IM exceeding House IM to continue further as more clients clear and as client accounts are typically more directional than house dealer accounts.

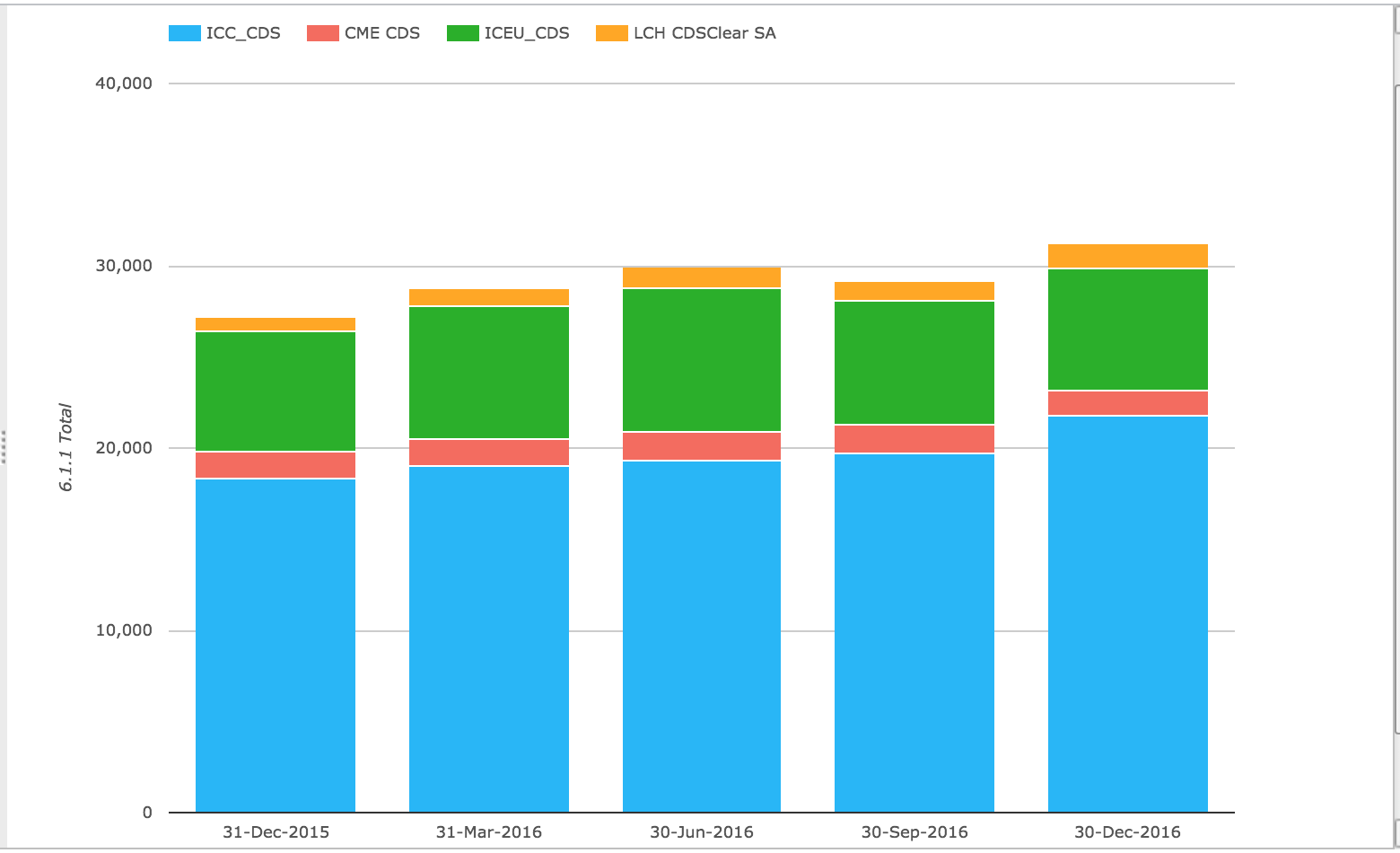

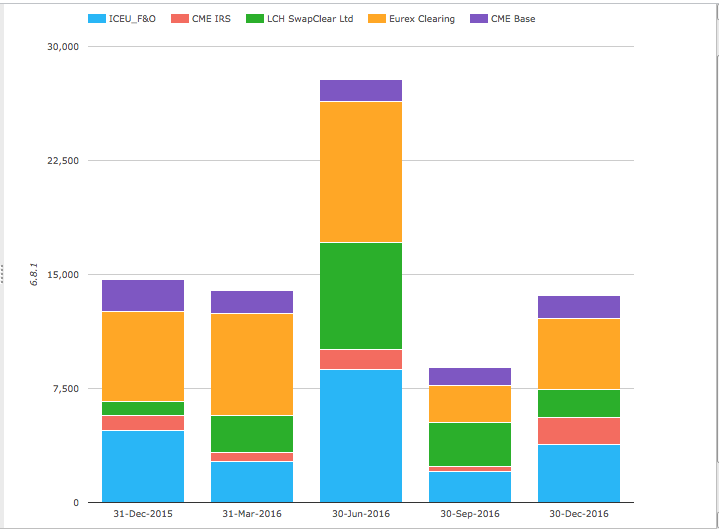

Initial Margin for CDS

Next lets look at the Initial Margin requirement for Credit Default Swaps.

Showing:

- Total IM for these four CCPs was $31 billion on 31-Dec-2016

- Up from $29 billion on 30-Sep-2016, an increase of 7% (in USD)

- Up from $27 billion on 31-Dec-2015, an increase of 15% (in USD)

- ICE Credit Clear the largest at $21.7 billion, up from $19.7 billion on 30-Sep-2016

- ICE Europe Credit next with $6.7 billion, similar to prior quarter

- LCH CDSClear with $1.4 billion, up from $1.1 billion on 30-Sep-2016

- CME CDS with $1.4 billion, down from $1.5 billion on 30-Sep-2016

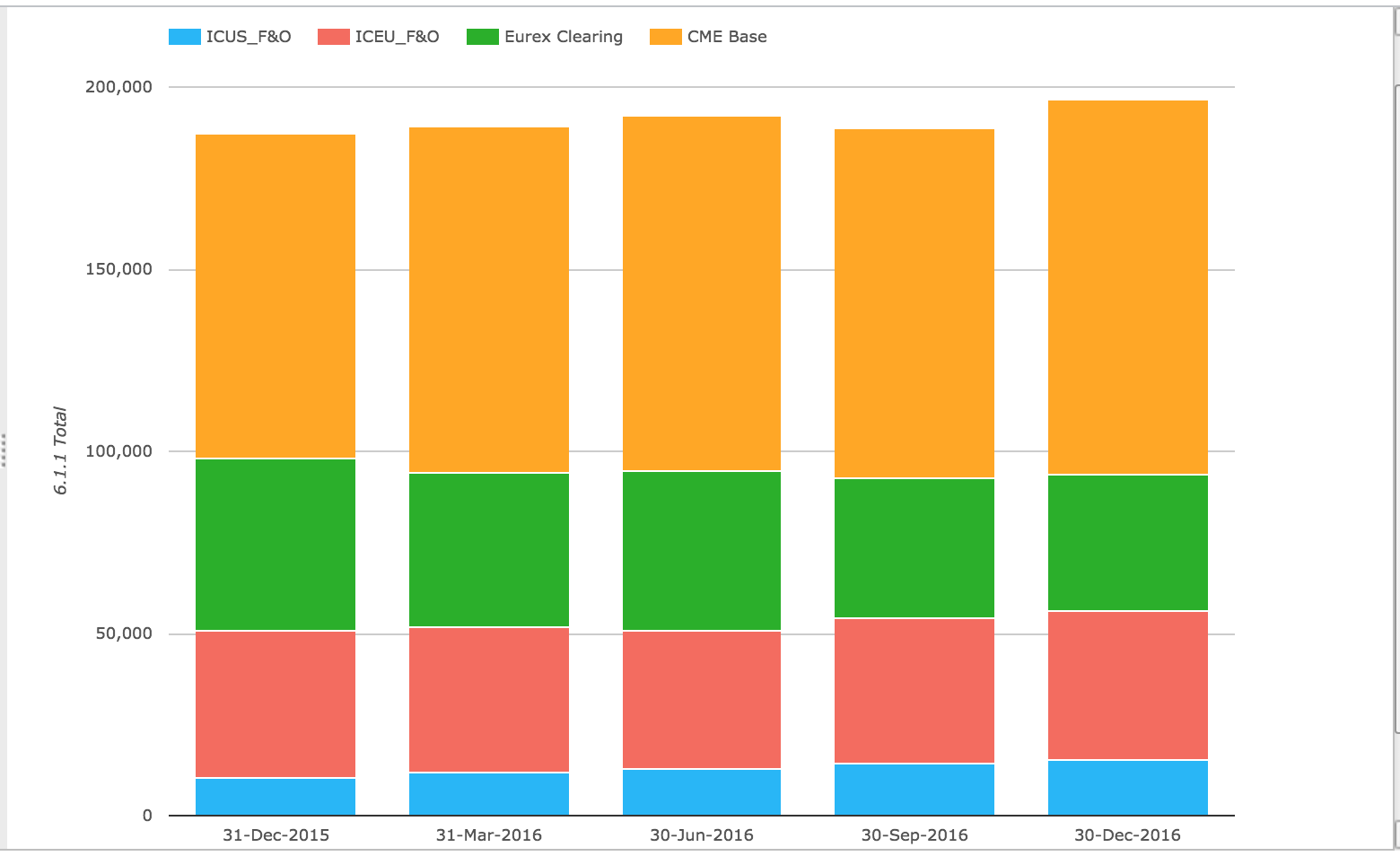

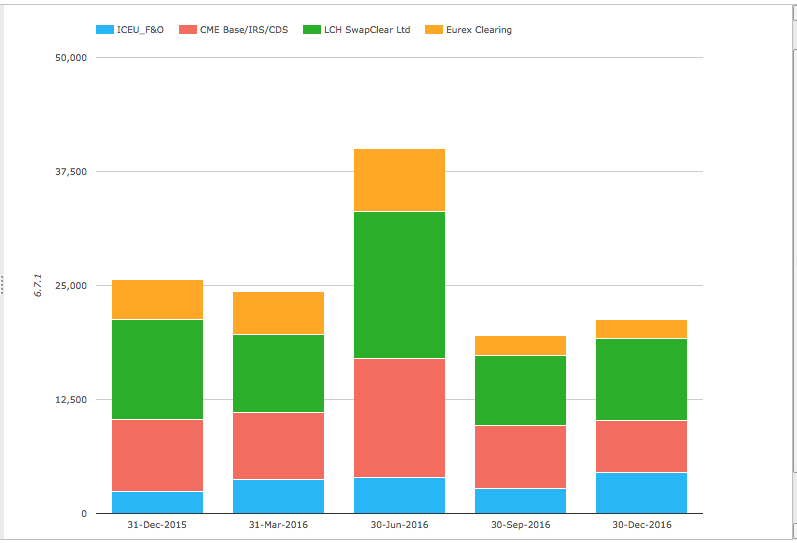

Initial Margin for ETD

Next Initial Margin for ETD (Futures & Options).

Showing:

- Total IM for these CCPs was $194 billion on 30-Dec-2016

- Up 4% from the $186 billion a year earlier

- CME Base is the largest with $103 billion, up from $96 billion on 30-Sep-2016

- ICE Europe F&O is $40.6 billion, up from $40 billion on 30-Sep-2016

- Eurex Clearing is $35.3 billion, down from $36.5 billion on 30-Sep-2016

- ICE US F&O is $15.4 billion, up from $14.3 billion on 30-Sep-2016

OTC vs ETD Margin

A quick comparison of the OTC IM (IRS + CDS) and the ETD IM from the previous section shows:

- ETD IM is $194 billion

- OTC IM is $141 billion + 31 billion = $172 billion.

- Making ETD significantly larger than OTC

However this understates the relative size of the ETD risk compared to OTC as typically ETD is margined on a one or two day MPOR basis, while OTC on a five day MPOR, meaning that a comparable ETD IM would be between 1.5 to 2.0 times higher (using square root of time).

VM and IM Calls

The flows of VM and IM between CCPs and their members are another interesting disclosure.

First the maximum total variation margin paid to the CCP on any business day.

Showing:

- The US Election on 8th Nov did not cause a massive jump in VM calls (as Brexit did)

- The aggregate maximum daily VM for these 4 CCPs in the last quarter was $21.3 billion

- Up from the $19.5 billion in prior quarter

- LCH SwapClear the largest with $9 billion on one day in the quarter

- CME next with $5.6 billion

- ICE Europe F&O with $4.5 billion

- Eurex Clearing with $2 billion

Next the maximum aggregate initial margin call on any business day over the period. (Note for some CCPs these figure includes intraday VM, so the IM component would be lower).

Showing:

- The aggregate maximum daily IM for these 5 CCPs was $13.6 billion

- Up significantly from the $9 billion in the prior quarter, but well below the high 2Q high of $28 billion

- Eurex Clearing the largest with $4.7 billion (this is likely to include large intra-day VM)

- ICE Europe F&O with $3.8 billion (again possibly including intra-day VM)

- LCH SwapClear, CME IRS and CME Base with $1.9 billion to $1.5 billion

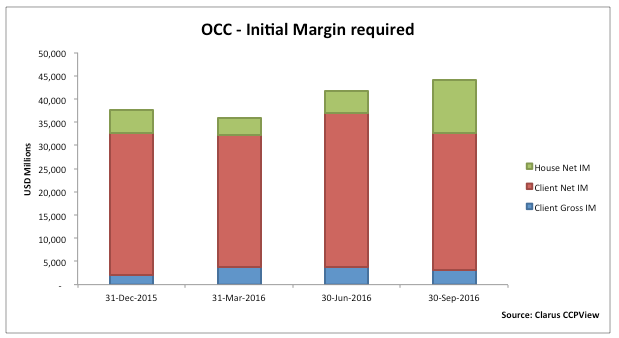

More CCPs – OCC

We continue to add more disclosure data into CCPView and a noteworthy recent addition is The Options Clearing Corporation (OCC), which clears Equity Options in the US.

Lets look at the size of OCC, by using Initial Margin as the metric.

Showing that:

- Total IM on 30-Sep-2016 was $44 billion

- (This is the latest data currently available)

- Client Net IM is the largest component at $29.4 billion

- House Net IM is $11.3 billion

- Total IM is up from $41.7 billion on 30-Jun-16

- And up from $37.5 billion on 31-Dec-2015

- A growth of 17% in this 9 month period.

So the OCC is a significant Clearing House indeed and one that we intend to look into in more detail as we start to include more Equities Clearing data.

More Disclosures

CCPView has a lot more CPMI-IOSCO Disclosures covering Interest Rate Derivates (IRD), Credit Derivatives (CDS), Futures and Options (ETD), currently from fifteen Clearing Houses each with many Clearing Services and we continue to add more.

With over 200 quantitative data fields and six sets of quarterly figures from these major CCPs, there is no lack of information for analysis and discussion.

If you are interested in this data please contact us for a CCPView subscription.