- The recent CME USD LIBOR conversion shows the power of netting for futures contracts.

- The standardisation of futures contracts increases the netting potential substantially compared to OTC contracts.

- Data shows that converted Eurodollar contracts have largely netted versus existing SOFR futures.

- The resulting Open Interest changes suggest that it was a particularly efficient risk management process.

This is an interesting journey through the data for those of you interested in what happened following CME’s conversion to SOFR for Eurodollar contracts (April 14th 2023) and the first USD conversion of LIBOR swaps at CME to SOFR (April 21st 2023).

Eurodollars

The once mighty Eurodollar contract is no more. (If you didn’t already know that, please subscribe to the blog!). As per the CME press release over the weekend:

The key take-aways are:

- CME converted an Open Interest of 7.5 million Eurodollar contracts into SOFR equivalents.

- $4Trn in cleared USD LIBOR swaps were converted to SOFR.

Let’s see how all of that played out in the data. Should be simple, right?

Futures Open Interest

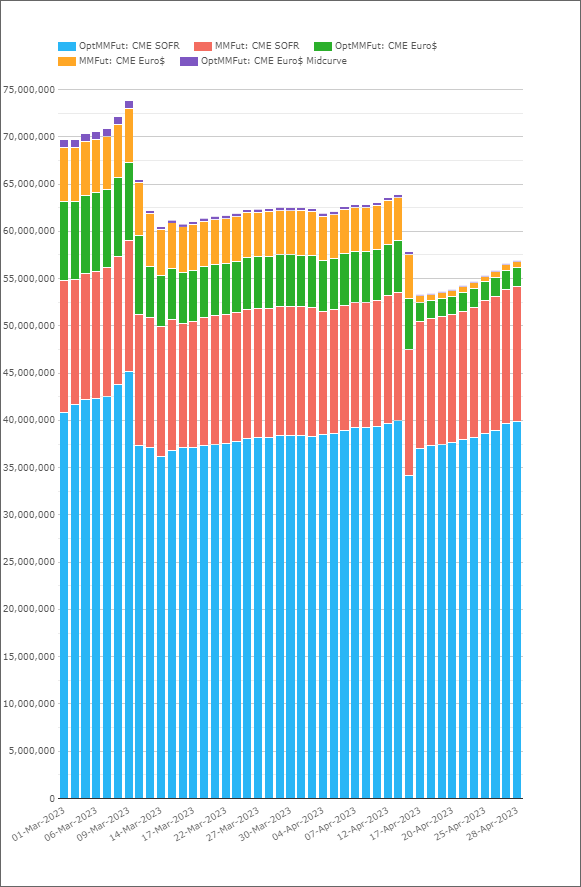

First up – Futures. Was it reasonable to expect all of the Open Interest in Eurodollars to be transferred into SOFR contracts? Let’s look at the data for March-April:

Showing;

- Daily Open Interest across Eurodollar and SOFR Futures and Options since March.

- You can see three big drops in Open Interest on the chart. The biggest two are actually due to the monthly expiries of SOFR options, highlighting just how much bigger the SOFR market is compared to Eurodollars.

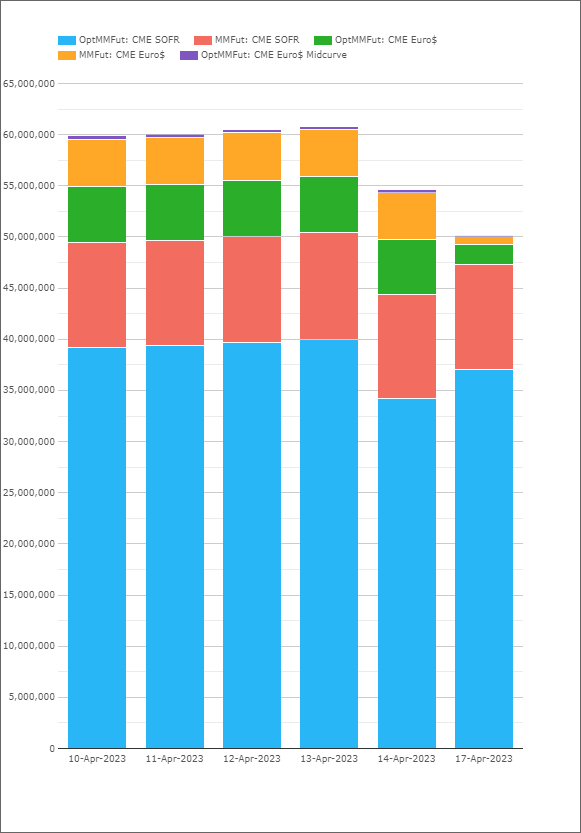

- Zooming in to look at the change in Open Interest from April 10th to close on April 17th:

- Showing;

- There were 4,580,375 Eurodollar contracts live on April 14th. On April 17th, this had shrunk to just 735,668. That small remainder is the Open Interest in the May and June 2023 contracts, that were not converted.

- There were also 5,419,443 Eurodollar options contracts live on April 14th. On April 17th, this had shrunk to 1,994,891. Again, the remainder are options versus May and June 2023 contracts..

- All 293,700 Eurodollar midcurve options were also converted.

- That gives us a grand total of 7,562,959 Eurodollar contracts that were converted between April 14th and 17th – exactly in line with the CME Press Release, which is a relief!

Tracking the SOFR Open Interest is equally interesting:

- The biggest change in SOFR Open Interest actually occurred from the 13th to 14th April, before conversion.

- This is because there was a significant amount of Open Interest in April options this year (about 5.75m contracts I believe).

- Some of these Options positions expiring in April will have been on underlying June SOFR contracts (as well as others). Those positions expiring in the money will have been delivered June SOFR contracts, which appear to have netted against existing Open Interest to a decent degree.

- The Open Interest in CME SOFR futures was then virtually unchanged (+66,210 contracts) between close 14th and close 17th.

- This small change in Open Interest shows that there was considerable netting between existing SOFR positions and the converted Eurodollars.

- CME SOFR options are easier to understand. Open Interest in the options contracts increased by 2,858,060 contracts – not dissimilar to the 3,424,552 Eurodollar contracts that were converted, with some netting versus existing SOFR options positions to be expected.

SOFR Trading Activity

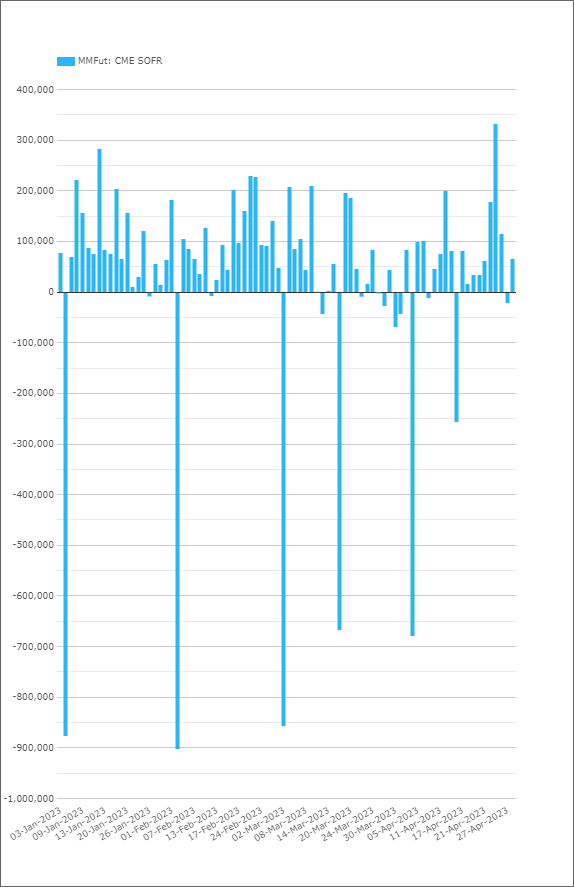

CCPView also tracks the daily change in SOFR Open Interest. This is shown in USD equivalents below for each day in 2023 (note that this is measured in USD millions rather than the contract counts used for previous charts):

We can see that:

- It is very unusual for the Open Interest in SOFR futures (i.e. excluding Options) to change by any more than ~$200bn equivalent per day.

- Roll dates (e.g. IMM and monthly options expiries) seem to account for a reduction in OI of between $600-900bn equivalent.

- The conversion of Eurodollar contracts does not stand out on the chart above at all.

This highlights just how efficient netting is in futures. So much of the converted Eurodollar Open Interest netted versus existing SOFR positions that it ended up being an almost neutral exercise overall.

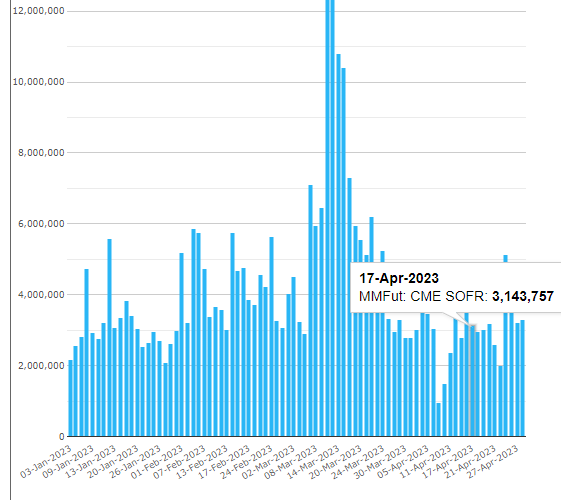

Adding to this impression, the daily volume traded in SOFR on April 17th was far from unusual. Around 3.1m contracts traded, very much in line with surrounding activity:

That such a momentous occasion as the conversion of the Eurodollar contract can go almost unnoticed in the data is quite extraordinary. It speaks to:

- The huge advantages of netting in standardised, commoditised and liquid products like futures.

- How well informed market participants were.

- How efficient risk management can be!

And What About OTC Conversion?

To shine a bright light on exactly how efficient conversion of Eurodollars was, we actually saw a big increase in “Open Interest” (notional outstanding) of SOFR swaps as a result of the LIBOR conversion for OTC swaps.

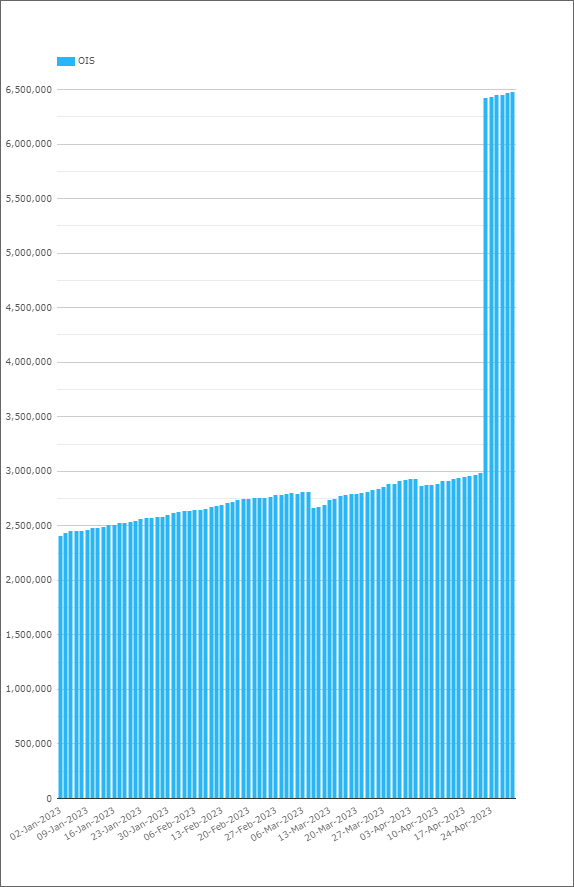

Showing;

- Notional outstanding of USD OIS swaps at CME.

- Can you spot the conversion date of USD LIBOR positions?!

- As per the press release, $4Trn of USD LIBOR notional was converted.

- This resulted in an increase in the Notional Outstanding of ~$3.4Trn.

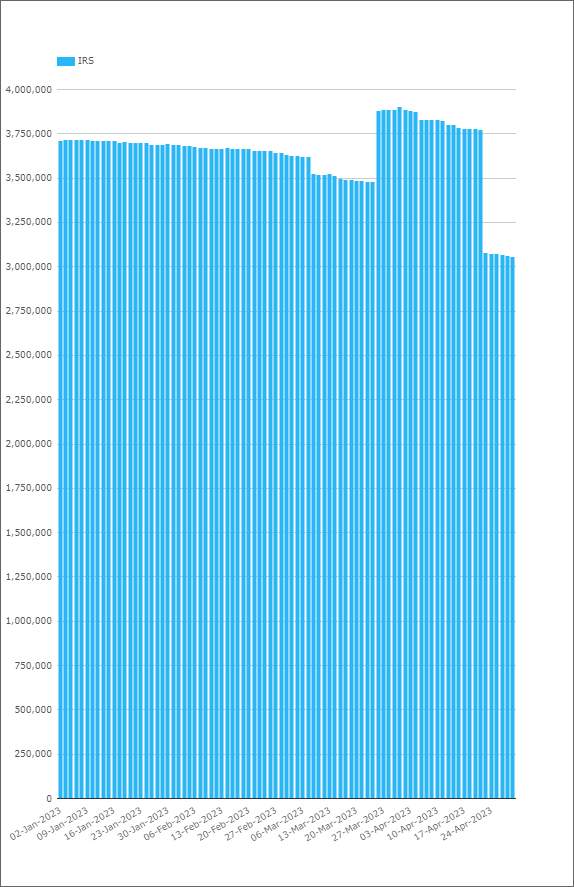

For completeness, when we cross-check that versus the drop in Notional Outstanding for USD IRS at CME:

We see a completely different number – Notional Outstanding dropped by “just” $0.7Trn. However, this was entirely expected because;

- Each LIBOR swap was converted into a short-dated LIBOR swap (a “stub” period) for any fixings deemed “representative”.

- Plus a new SOFR swap for all periods after that date.

- For full details see our conversion blog.

- Therefore, we see almost $3Trn of “new” Notional Outstanding added as a result of existing trades and their stub periods being rebooked.

- And a corresponding decrease of ~$4Trn for long-dated notional outstanding.

In Summary

- Most of the conversion of USD LIBOR positions at CME is now complete.

- The success of the processes highlights some key differences between futures and OTC markets.

- The Eurodollar conversion resulted in highly efficient netting of futures.

- Standardised products really show their value in exercises like these.

The data above shows that it is very difficult to anticipate the impact of the conversion exercise on the ISDA-Clarus RFR Adoption Indicator. Check back next week to find out….