Whilst ostensibly this blog is about the March 2023 edition of the ISDA-Clarus RFR Adoption Indicator, I cannot let pass the disappearance of the largest futures contract that I ever traded without comment.

A huge part of the Clarus blog in recent times has been focused on the transition away from IBORs and into RFRs. What was once an inconceivable step has now finally taken place – the 3 month “Eurodollar” contract at CME (i.e. a contract for difference versus the 3m USD LIBOR fixing) is no more. The remaining Open Interest (after June 2023 expiries) was converted into SOFR equivalent contracts as of close of play Friday.

I will not be the only person in the market thinking about:

- My first ever real “trade” was in Eurodollar futures.

- You had to learn a whole new language to be able to trade them – this was before screens!

- It makes me feel very old for my career to have extended past the lifetime of what was once the largest traded contract in the world.

- It was the simplest product to be able to conceptualize when starting out. Is a futures contract that settles versus compounded rates and pretty much ceases to trade before it actually expires so simple for “newbies”?

- I will forever miss the anticipation/nervousness/adrenaline on IMM day of where LIBOR will actually fix. Having rolled so many FRA fixings into the IMM, the sheer size of positions always made it an event.

For those feeling really nostalgic, the front 3 contracts are still available to trade:

But in essence, Friday marked the final day of “real” liquidity I think. Let’s therefore take a look at the data behind the conversion:

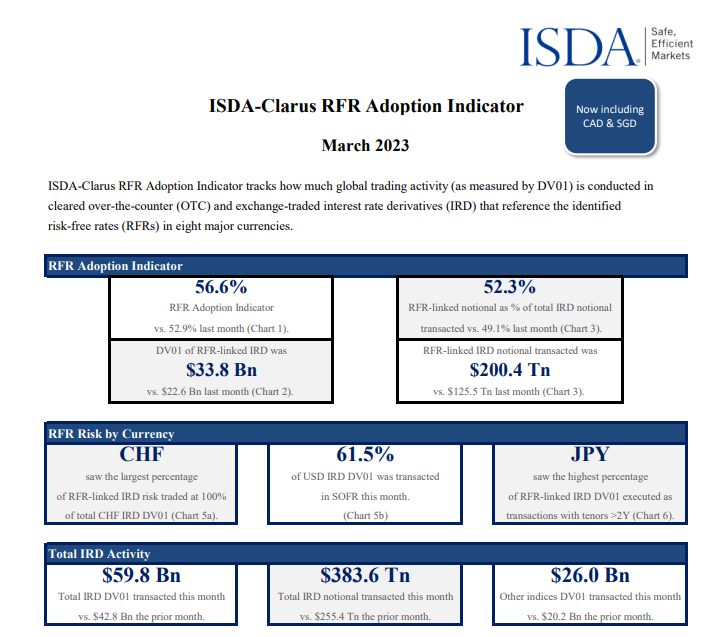

March 2023

The RFR Adoption Indicator for March is therefore the last mark we have before the Eurodollar contract disappeared. The report shows some very good news, and will likely be even higher next month (read on to estimate how much higher):

Showing;

- The index has increased to a new all-time high of 56.6%, 3.7% higher than last month.

- Over $200Trn of RFR-linked notional traded for the first time ever.

- SOFR adoption hit 61.5% (just shy of the all time record), increasing by 2.4% compared to last month.

- The trends for EUR, CAD and AUD adoption are all positive – I show the charts below.

It is an interesting exercise to see what happens to the RFR Adoption Indicator if all of the Eurodollar risk is converted into SOFR.

Hold on to your hats

With a bit of trickery behind the scenes, I can convert our volume data related to Eurodollar futures into SOFR futures.

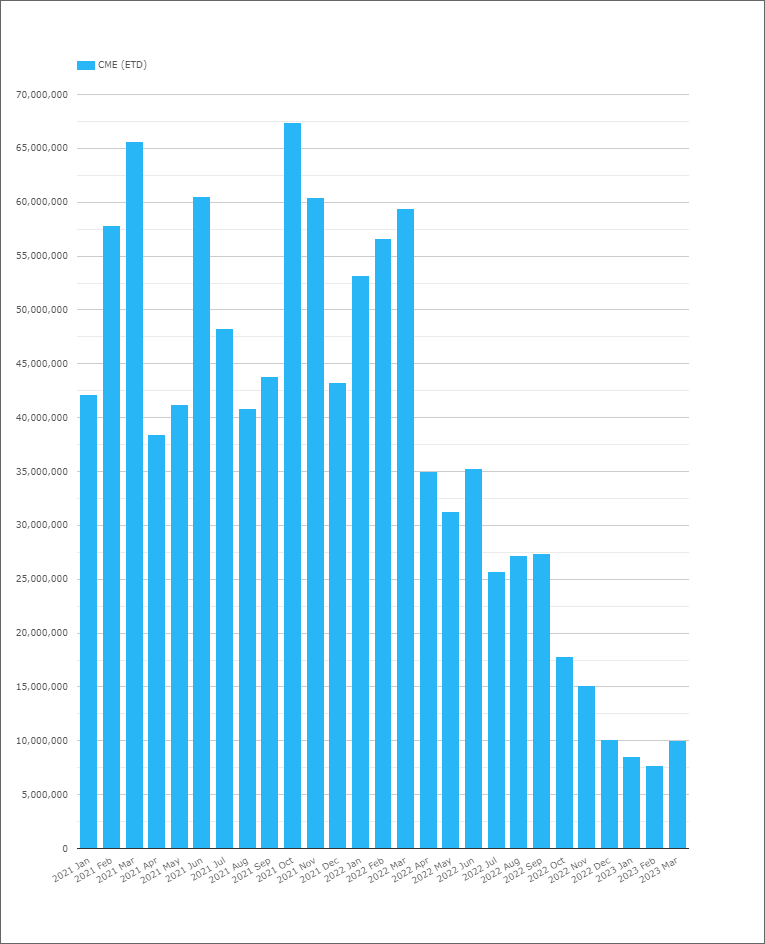

In March 2023, we saw $10Trn of notional-equivalent traded in Eurodollar futures (as shown in CCPView):

What is the approximate impact of moving $10Trn of notional activity from LIBOR-based products to SOFR-based? There are a few moving parts here:

- The RFR Adoption Indicator is based on DV01, therefore it depends on the maturity of that notional. Almost all Eurodollar activity is below 1 year.

- How much of this Eurodollar notional is spread related, and actually already trading as a spread to SOFR? We do not know.

- March is an IMM month, therefore may well have seen some activity related to the roll.

- June 2023 contracts have not been converted into SOFR equivalents because there will still be a USD LIBOR fixing published in June. Same applies for the April and May contracts. Therefore, there will still be a little bit of Open Interest left in Eurodollars after the conversion – but it is unlikely to see a lot of trading and therefore will have very little effect on the RFR Adoption Indicator from this point forward.

Because of those factors, we can only estimate the maximum possible impact of moving all Eurodollar activity into the SOFR contract. If we do so, we find the following impact on SOFR adoption:

Surprising?

- Our calculations suggest that SOFR would increase to 64.3% of the USD market, from 61.5%. This assumes that 100% of Eurodollar activity moves into SOFR contracts.

- The impact to the overall RFR Adoption Indicator is about half the size – moving it up to 58.2% from 56.6%.

The elephant in the room continues to be Fed Funds. Do you know what notional equivalent of Fed Funds futures traded in March 2023?

Answer: Nearly $100 Trillion!

Whilst the Fed are in play, this elevated activity in Fed Funds futures is likely to persist. Suggesting that SOFR adoption may top out at 65-70% for now.

Elsewhere

Whilst all eyes are on SOFR for good reason (Eurodollar conversion followed by final USD LIBOR cessation in around 12 weeks), there are some really interesting things happening in other currencies.

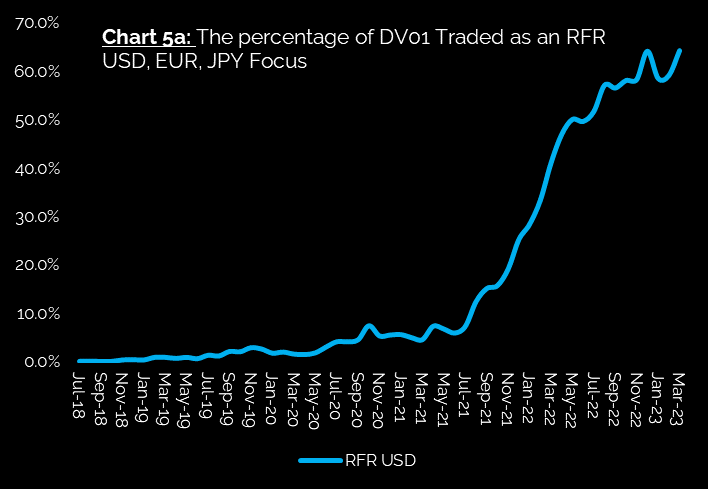

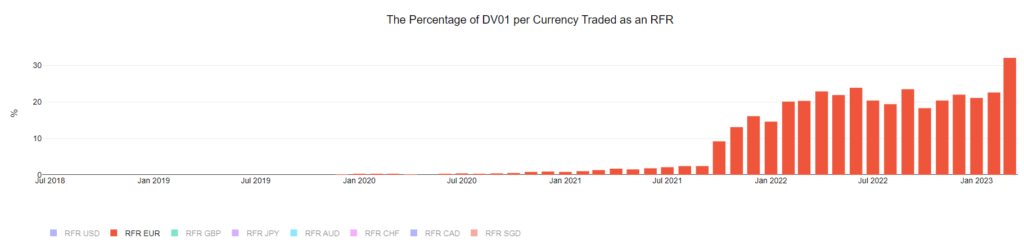

For example, take a look at the march of €STR adoption in EUR Rates markets:

Showing;

- March 2023 marked the first time that over 30% (32.1% actually!) of EUR risk was traded versus the RFR.

- That is a remarkable difference and one of the biggest jumps we have seen in any currency, absent any regulatory announcements.

- Will EUR be the first market to voluntarily transition to RFRs?

All eyes on the April figures to see if this momentum can be maintained.

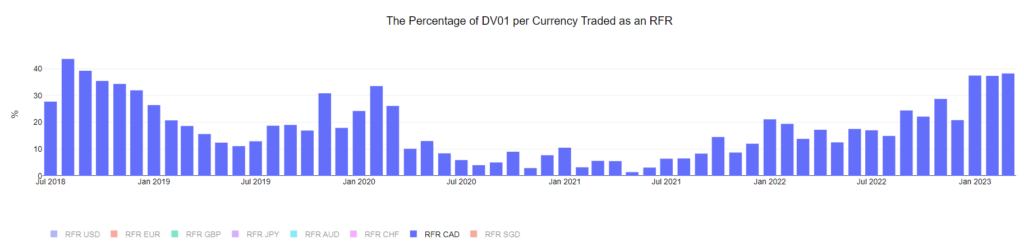

An RFR market with real momentum is CAD. The CORRA First initiatives are working:

Showing;

- CAD has now seen 3 consecutive months where CORRA has accounted for over 37% of trading activity.

- I included the full time history as way back in July 2018 CORRA was a popular index as well, but it quickly petered out.

- There was a further CORRA first initiative in Cross Currency Swaps from March 27th, which also covered the CAD Swaptions market.

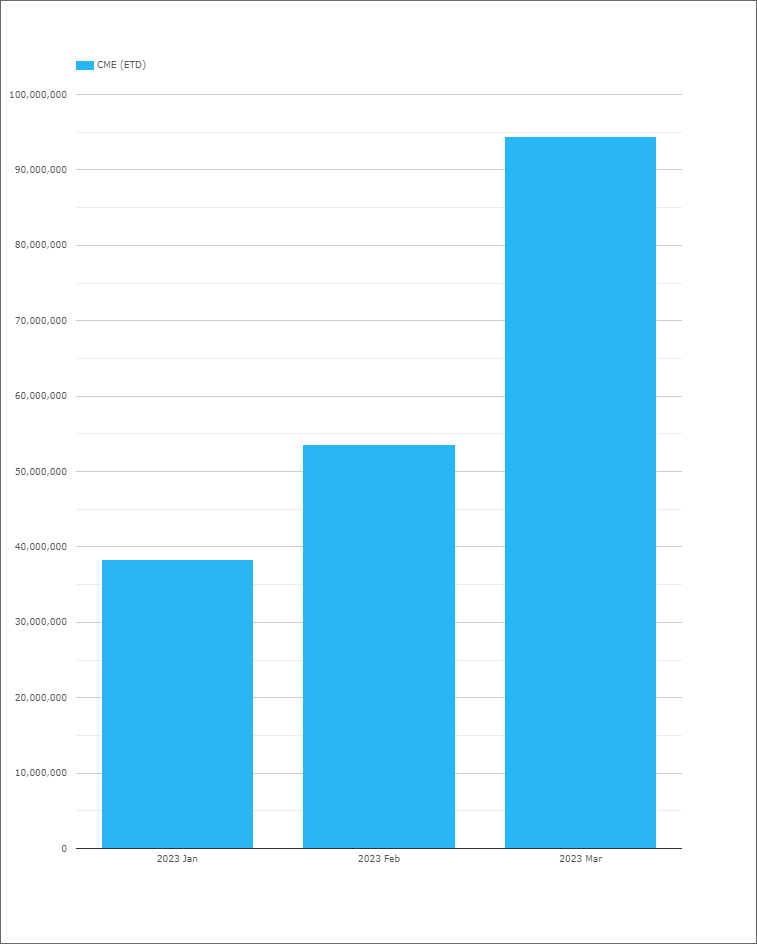

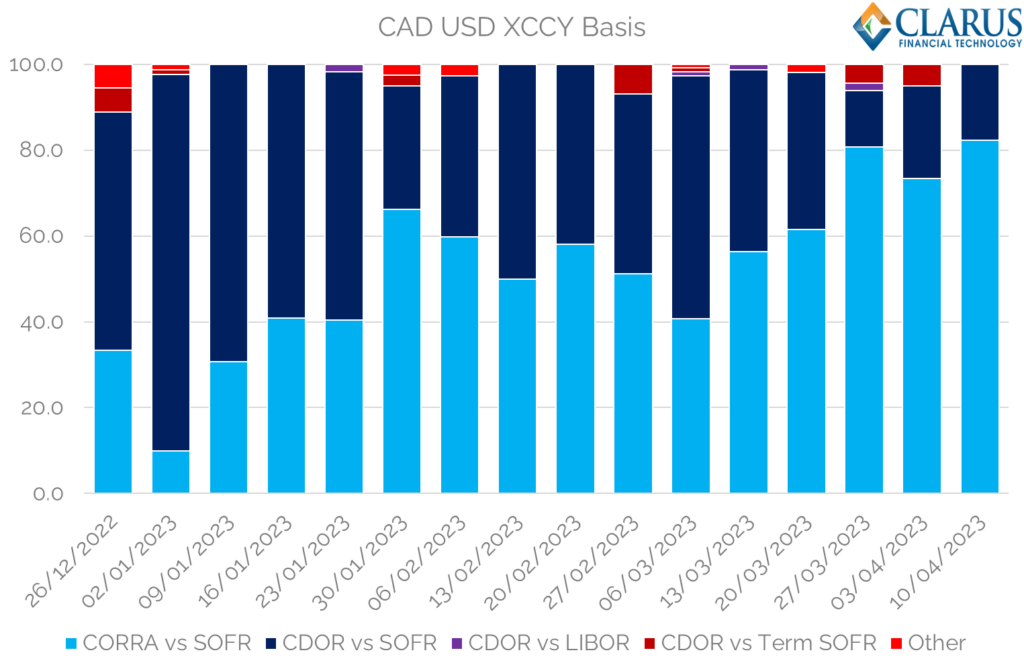

Looking at CAD XCCY swaps reported to SDRs, it looks like CORRA First in XCCY has had the intended effect, raising the proportion of CORRA vs SOFR trades (from an already high level):

Showing;

- In the most recent full week, over 82% of trades (by trade count) were reported as CORRA vs SOFR.

- This is a new high since the beginning of 2023.

- There have been a few trades referencing Term SOFR, but it is fair to say most of the liquidity is now in “pure” RFR vs RFR.

- This is a far cry from previous years, when term CDOR vs compounded SOFR was the norm in CADUSD.

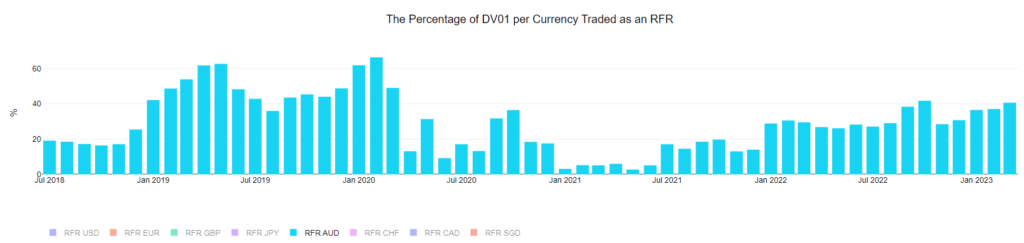

And finally, we should highlight the uptick in AONIA trading in AUD markets:

As we’ve said before with AUD markets, it is really hard to disassociate the increase in AONIA trading versus the fact that the RBA is “in play” with lots of repositioning regarding when/if they may hike again. Similar can be said for CAD and EUR as well, so it remains to be seen whether these trends can stay in place once Central Banks are less active.

The data will tell….

In Summary

- The March 2023 ISDA-Clarus RFR Adoption Indicator hit a new all time high of 56.6%.

- This increase came before the CME Eurodollar contracts were converted into SOFR.

- Whilst the Eurodollar conversion is a momentous (and nostalgic!) occasion for market participants, the impact on overall RFR and SOFR adoption will be quite small.

- There are positive trends in RFR adoption in EUR, CAD and AUD right now.

- Stay tuned to see how these trends progress in the Clarus data.