A crucial step in the final transition to USD SOFR is the physical conversion of outstanding cleared OTC swaps from USD LIBOR to USD SOFR. Clearing Houses (CCPs) provide this as a service to clearing participants and it is a crucial “last step” in the move away from LIBOR. Remember that USD is the last of the LIBOR currencies. No more USD LIBOR, no more LIBOR full-stop.

The last paragraph of this blog includes worked examples at both CME and LCH for those who like the details!

Conversion?

First, a few of my own thoughts on conversion:

- Ever since we have known the date of USD LIBOR cessation, the risk on a USD interest rate swap stopped being versus LIBOR and moved to SOFR + spread for all fixings occurring after June 30th 2023.

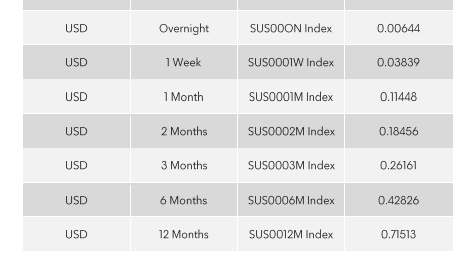

- The spread was calibrated via the ISDA Fallbacks and published way back on 5th March 2021:

- A CCP converting a swap shouldn’t change the thoughts of a market participant in terms of their primary risk factors.

- The cashflow of any USD LIBOR fixing after the end of June 2023 has been governed by compounded SOFR in-arrears plus a spread since March 2021.

- A conversion event makes this an explicit fact. Rather than continuing with LIBOR swaps, the CCP “re-books” a trade so that it explicitly references SOFR + the ISDA Fallback Spread.

Two things to note at this juncture:

- Why would a CCP bother to rebook all of those trades? Latest estimates are about 500,000 contracts will be converted. LCH cover this really well in their consultation so I won’t add anything:

- This is different to the “SOFR Auction” we covered in detail back in October 2020. That was when CCPs changed their discount curves from Fed Funds to SOFR. This created real “new risk” to the market that needed to be hedged – market participant’s discounting risk on their cashflows was now calculated at SOFR, and no longer at Fed Funds. Converting trades from LIBOR to SOFR representation does not carry any change in risk profile.

- A Fallenback trade does not share precisely the same characteristics as a market standard SOFR swap. For reasons long since lost in legalese and consultation responses, the payment dates of a LIBOR swap were deemed sacrosanct. But the daily SOFR fixing isn’t published in time to be able to make same day payments. So, on the whole, there is a two day payment gap for Fallenback trades versus standard SOFR OIS. But there are also edge cases (which may be quite common), whereby differences between standard SOFR OIS and Fallback trades may be greater – the most commonly cited one being a “short” IMM period of e.g. 84 days.

- So how could a CCP “convert” trades? There are a few different ways it could be achieved:

- The Fixed Rate from the old swap is always carried forward onto any new swaps.

- One option is to terminate the old swap after the last LIBOR cash-flow occurs, and re-book the rest of the swap from the first SOFR fixing date until the maturity date.

- Or, terminate the old LIBOR swap, and book an identical trade from start date to end date, but vs SOFR.

- Then, suppress all pre-dated cashflows so that they don’t happen again!

- And either a) book a cash-flow on the new swap for the known last LIBOR-linked cashflow.

- Or b) book a single period LIBOR vs SOFR swap for the final LIBOR cashflows (e.g. any fixings due to settle before June 30th and any new fixing to take place before June 30th).

- Etc etc. I am sure there are some other ways to engineer almost identical cash-flows so that the conversion is as risk free as possible.

- There are positives and negatives of different approaches.

- Considerations include scalability, accuracy, gross notional, line items. Even hedge accounting gets a look in, because ultimately accountants always have the final say!

- Probably due to the scale of positions, the two day difference in payment dates between Fallenback and Market Standard SOFR trades can even cause a (somewhat minor) NPV difference for portfolios. CCPs will make NPV transfers from winners to losers so that everyone is kept whole in the exercise.

- This is not the first time CCPs have converted trades. They did the same exercise for GBP, CHF and JPY LIBOR trades back in 2021. Blog here.

So Who Will be Impacted by Conversion?

If you clear swaps, it is very likely that you will be impacted by these conversion events. CCPs must ensure dealers and clients are able to process the huge amounts of trade amendments & terminations. So whilst the event doesn’t change market risk – it is not something we will see turning up in SDR data! – it does carry a large amount of operational risk across the industry.

Interestingly, CCPs and market participants have chosen to convert all trades at the same time – a “big bang”, rather than programmatically amend swaps after their final LIBOR payment dates. This must be due to risk considerations, otherwise people could have thousands of swaps being amended daily for the next 6-12 months (until the final 12 month LIBOR payment occurs on June 30th 2024 anyway). And what would you do with zero coupons? (Both CME and LCH materials deal with the specific case of zero coupons for any interested readers).

Because all of the conversions will happen when markets are “closed”, they also consume a lot of people’s weekends across the industry. That alone makes “LIBOR” a dirty word in most circles these days!

How Big Is the Conversion?

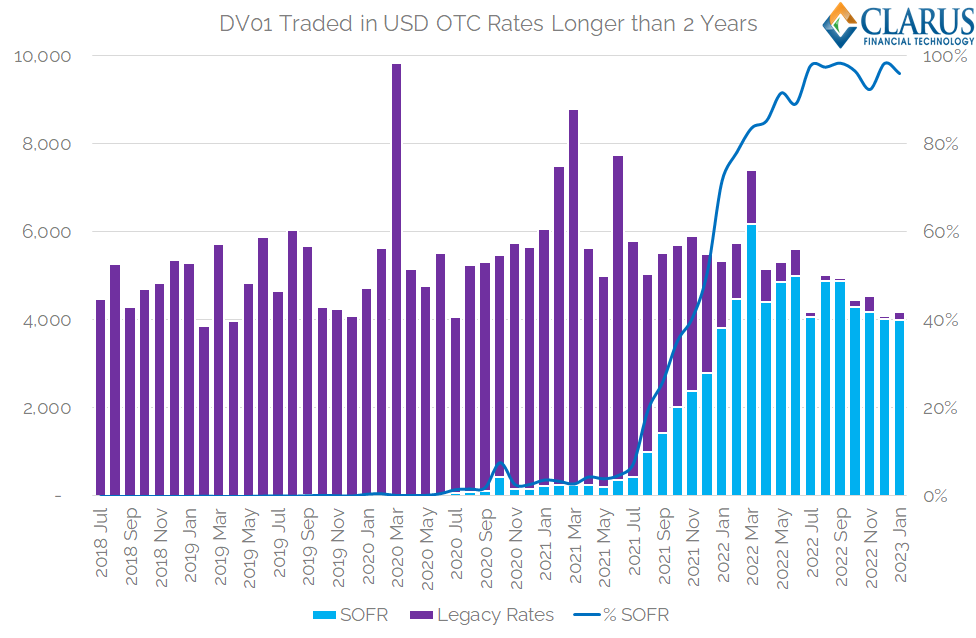

Recall from last week’s blog that we now see almost all new long-dated OTC risk traded versus SOFR:

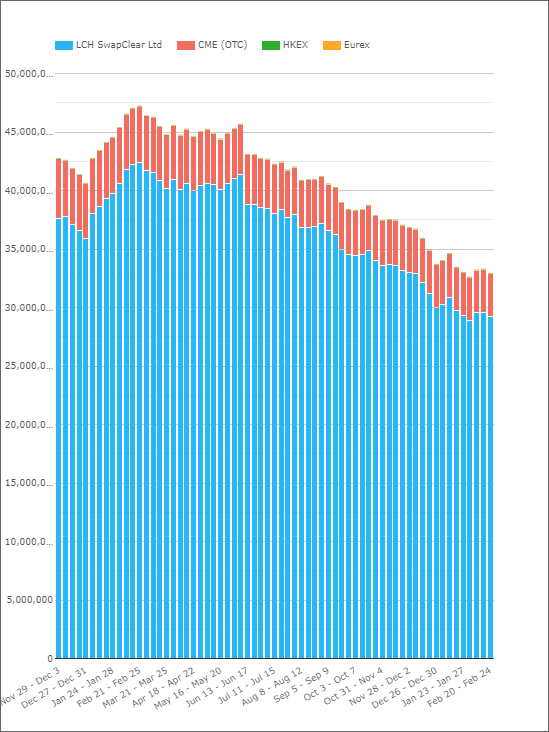

However, this does not look at the outstanding stock of trades still out there. The Open Interest in USD-linked IRS is still highly significant at CCPs:

Showing;

- There was over $47.2Trn of USD-LIBOR linked cleared positions outstanding as recently as February 2022.

- This has reduced in the past 12 months, to currently stand at over $33Trn. (This is a smaller number than you will see quoted by CCPs/Risk.net etc due to our data methodology at Clarus).

- The reduction is likely a result of the natural run-off as trades mature, with some aspect of risk reduction/terminations thrown-in.

- Interestingly there is no evidence that uncleared positions have been backloaded into Clearing. This would tend to increase Open Interest.

- Therefore it is likely that market participants will be looking at the CCP conversion process to convert outstanding USD LIBOR into SOFR for cleared positions…

- ….and relying on ISDA fallbacks for their uncleared portfolios.

Whilst the CCP conversions will occur on specified dates, and USD LIBOR will cease publication as of June 2023, this does not rule out future conversion of uncleared trades. “Fallenback” portfolios will still have to be risk managed until maturity.

What Are The Conversion Processes?

The details of what will happen have been known for quite some time. For example, the CME document is dated August 2022:

LCH’s most recent guide is here:

In a nutshell:

- LCH will convert some trades on 21st April but most will be converted 19th May.

- CME will also convert on 21st April, with the second run occurring 3rd July.

- LCH estimate 500,000 contracts will be converted. This compares to around 300,000 last time round for GBP, CHF and JPY.

- Risk.net and Financial News cover the details here and here.

- CME will convert to a new forward-starting SOFR swap (i.e. same fixed rate as original contract versus SOFR + fallback spread), with any remaining LIBOR-linked cashflows booked as a short-dated Swap.

- Imagine a CME 3m USD LIBOR Swap for 5 Years at 1.5%, starting 9th March 2023.

- The representative (i.e. “valid”) USD LIBOR fixings occur 7th March 2023 and 7th June 2023, creating valid LIBOR-linked cashflows on 9th June 2023 and 9th September 2023.

- This will be converted into a new forward-starting SOFR swap starting 9th September 2023, running until 9th March 2028 at a 1.5% fixed rate versus SOFR + 26.161bp.

- And there will be a remaining USD LIBOR Flat vs 1.5% Fixed Rate swap running from 9th March 2023 until 9th September 2023.

- The original LIBOR swap is terminated.

- LCH will convert each LIBOR swap into a SOFR swap (+ fallback spread) with the exact same dates (and fixed rate) as the old swap. A basis swap “overlay” trade will then be booked for the final LIBOR payments.

- Imagine an LCH 3m USD LIBOR Swap for 5 Years at 1.6%, starting 9th March 2023.

- The representative USD LIBOR fixings occur 7th March 2023 and 7th June 2023, creating valid LIBOR-linked cashflows on 9th June 2023 and 9th September 2023.

- In May, this will be converted into a new backward-starting SOFR swap starting 9th March 2023, running until 9th March 2028 at a 1.6% fixed rate versus SOFR + 26.161bp.

- And there will be a new “overlay” basis trade to replicate the representative LIBOR fixings – starting 9th March 2023, maturing 9th September 2023 at LIBOR flat versus SOFR + 26.161bp.

For CME, they will also be converting all outstanding Eurodollar contracts to SOFR on 14th April. Wow!

In Summary

- CCPs will shortly begin converting the last outstanding LIBOR OTC contracts into SOFR contracts.

- This conversion will happen so that the remaining trades will be equal to SOFR + the ISDA Fallback spreads.

- If you have one take-away from this blog it should be that this does not change the risk in the market.

- These events will take place across the weekends of April 21st, May 19th and July 3rd.

- Some LIBOR-linked cashflows will occur, but there will be no LIBOR linked “risk” in clearing any more.