CORRA First was put in place on January 9th 2023 to help CAD interest rate derivatives transition from CDOR to CORRA. For all of the juicy details, please see my blog from last year:

Transparency is Better Than Ever

RFR transition in Canadian markets may seem a little niche for some of our readers. However, it also serves as a fantastic opportunity to highlight the improvements in transparency that the US have introduced since December last year.

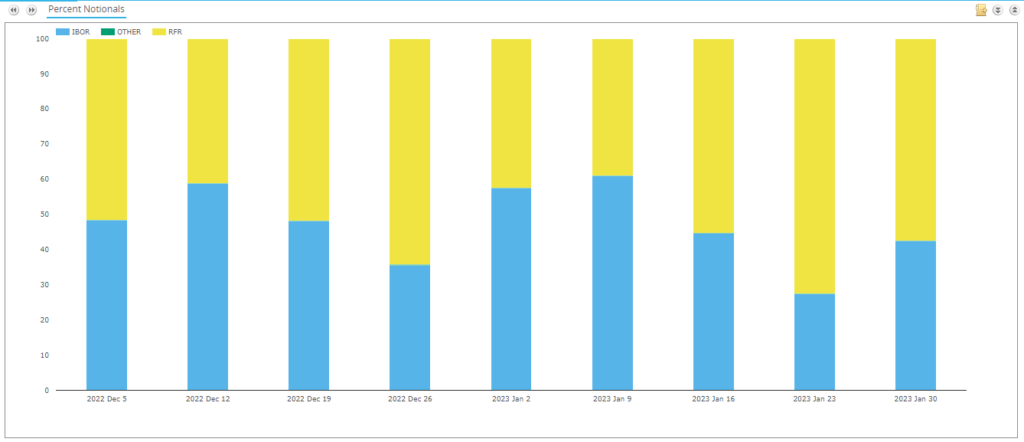

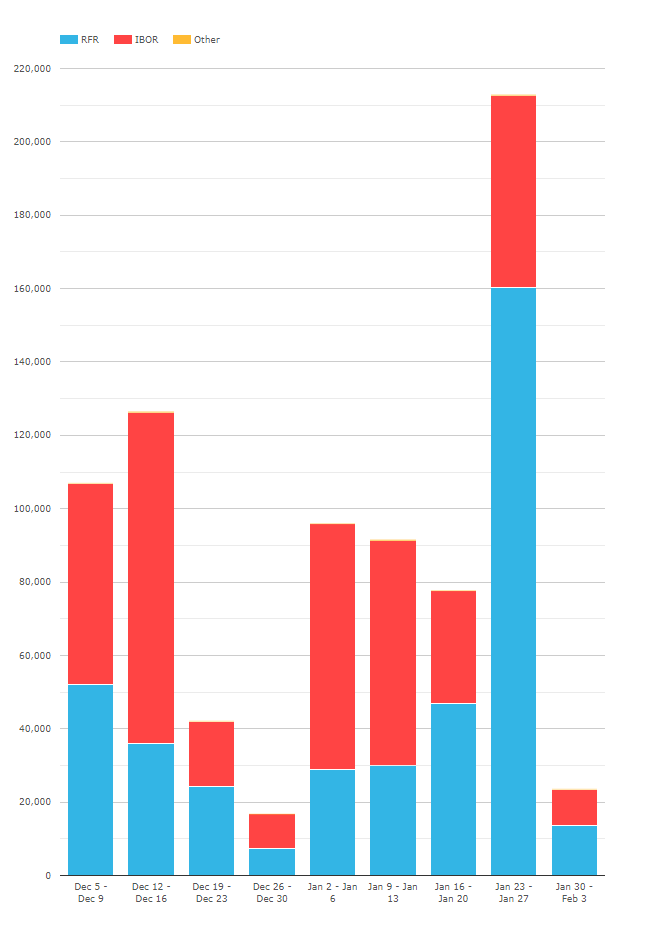

SDR data shows the proportion of trades transacted as RFR or IBOR (CORRA or CDOR in this case), and shows no great change so far:

Showing;

- The percentage of notional for CAD swaps (both vanilla IRS and OIS) that is transacted versus RFR (CORRA) or IBOR (CDOR) each week since the beginning of December 2022.

- It is a volatile measure, ranging from 39% (week of Jan 9th ) to 72% (week of Jan 23rd).

- So far this week, we are back to a 57/42% split.

- Even back in December, CORRA accounted for up to 61% of trading.

Presented as such, it suggests that CORRA First has not really impacted trading activity yet.

However, that is not true.

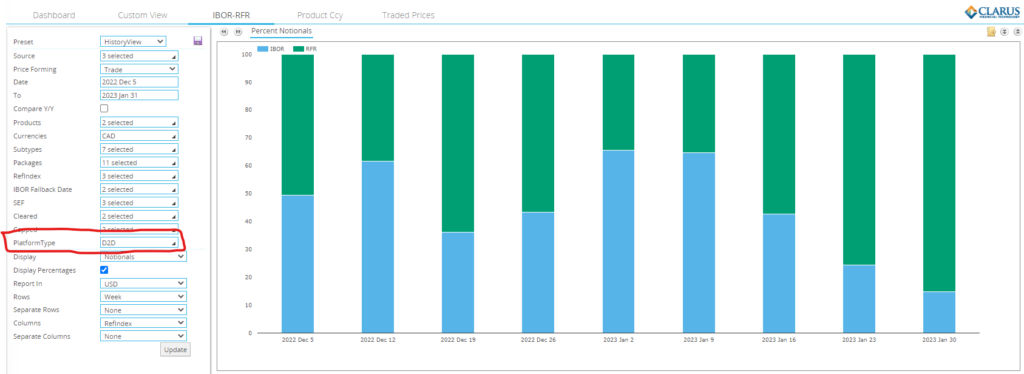

D2D CAD Markets

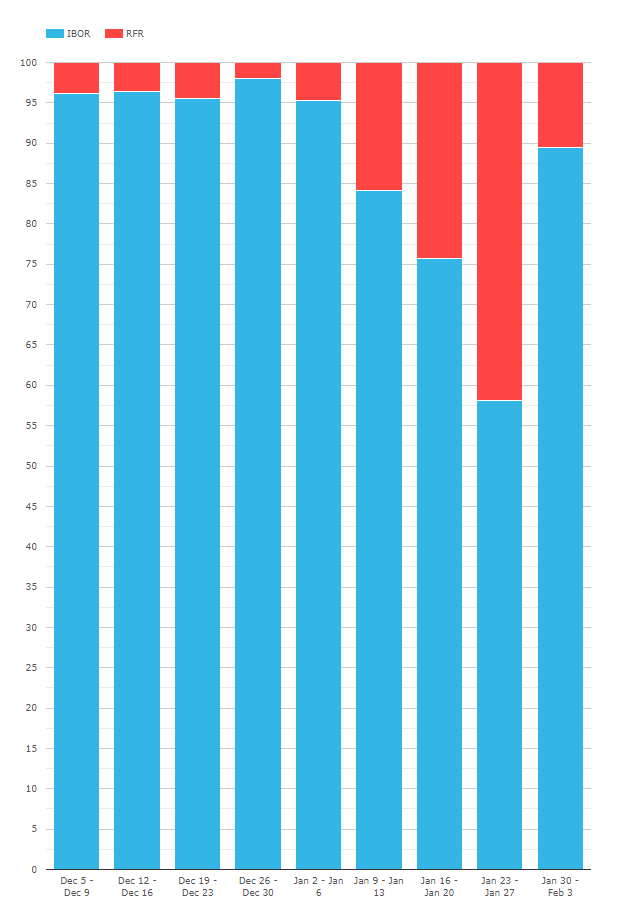

Since December, SDR data has included a platform identifier for each trade. This means that we now know, at a transaction level, whether the trade was executed on a Dealer to Dealer or Dealer to Client platform.

In SDRView we have now added this filter. For CAD markets, the behaviour on D2D platforms has certainly changed as a result of the CORRA First initiative:

Selecting D2D platforms changes the data significantly!

- CORRA First started on Monday Jan 9th 2023.

- We can see that every week since, the proportion of activity traded versus CORRA has gradually increased in D2D markets.

- The week of Jan 9th saw 35% of notional traded versus CORRA.

- This has increased every single week since – 57%, 75% and now 85% so far at the end of January.

- That is a pretty compelling uptake of RFRs by Canadian dealers!

Oh, Canadian Clients

Oh, Clients. Why are you so slow to change? Do you not read our blogs? I think that must be it – Clarus has to do more to improve our readership amongst the buyside. Dealers are clearly aware of CORRA First. And whilst, yes, it is focused on dealer markets, Clients would be well-served to sit-up and take note as well. Afterall, liquidity continues to be the primary consideration, right?

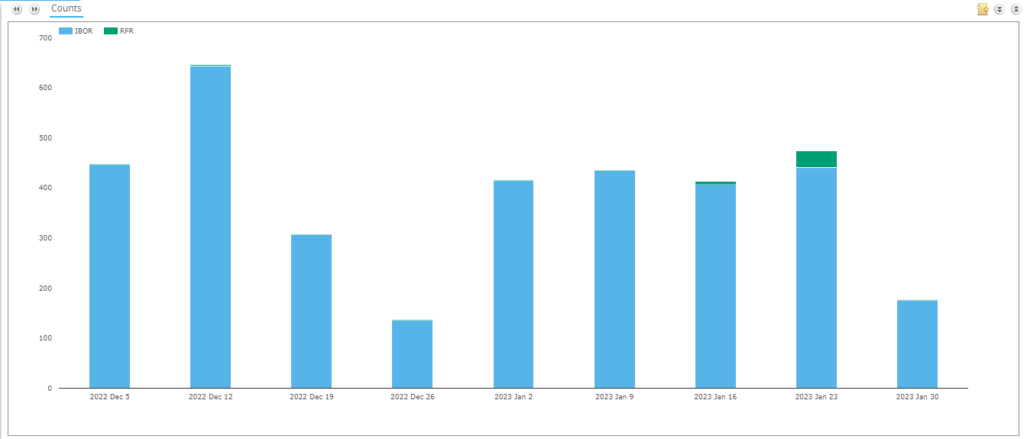

The same chart for D2C SEFs (i.e. Tradeweb and Bloomberg) looks VERY different:

Showing;

- The number of trades transacted on D2C SEFs in CAD markets each week, split by IBOR (CDOR) and RFR (CORRA).

- The chart looks a bit silly on a percentage basis because the RFR basically never trades on D2C platforms.

- We did see 35 client trades (big whoop!) last week versus CORRA.

- But we haven’t had a single one yet this week. Doh.

Global View

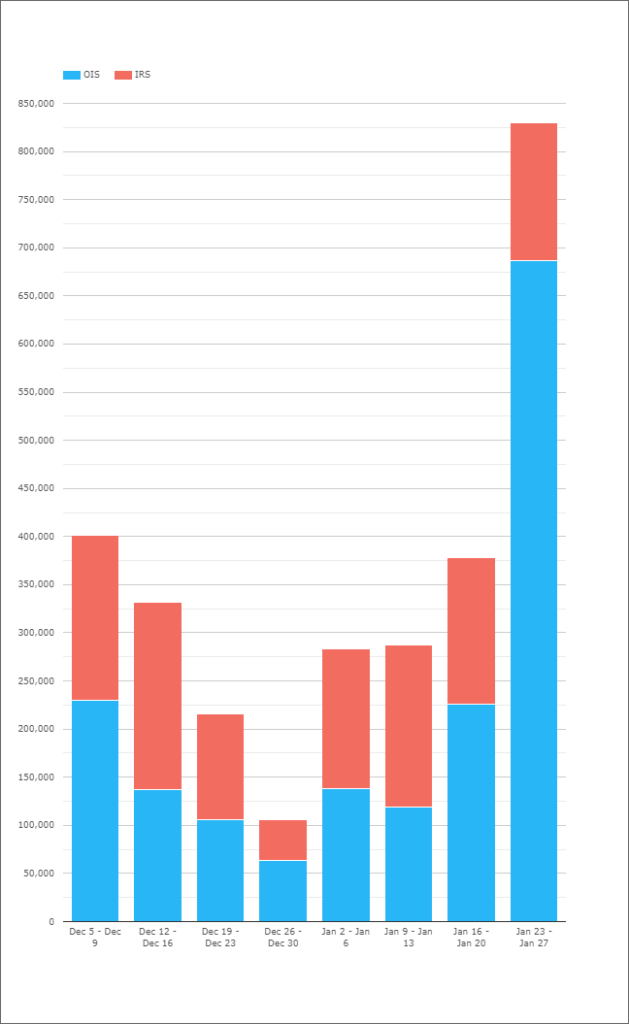

SDR data provides a good insight into the CAD market due to the large footprint of “US Persons” in the market. It is also worth cross-checking the results versus the global cleared market in CCPView.

Here, we see a huge amount of notional traded in OIS vs CORRA last week – a very positive sign for CORRA First!

But a cross-check versus the tenors traded shows that most of this OIS volume was in 2Y tenors (and shorter):

SEFView

SEFView shows the activity in CAD markets executed on-SEF. We can see a huge amount of notional CORRA was traded last week:

This also translates into a record week when measured by DV01:

We already know from the SDR data that this increase in RFR activity is mainly coming from D2D activity. It is a start.

In Summary

- CORRA First has started in CAD markets.

- There is strong evidence in the data that the initiative has changed trading behaviour.

- Recent changes in the transparency regime result in a much better understanding of changes such as CORRA First.

- D2D markets are leading the way in CORRA adoption.

- The data can be complex. Markets benefit from standardised measures to track these changes.