- CDOR will cease publication in June 2024.

- This requires Canadian Rates markets to transition to CORRA OIS.

- The first “CORRA First” initiative will take place on January 9th 2023.

- We look at current volumes and how CAD markets can successfully transition to RFR trading.

I first wrote about benchmark reform in Canada in 2019:

Since then, we have had the announcement that CDOR will cease in 2024:

As with all good benchmark stories, the announcement of cessation sets the ball-rolling on a number of fronts:

- When will trading transition from CDOR to CORRA in interdealer markets?

- Will clients follow?

- When will futures liquidity shift? Are there suitable RFR-linked futures contracts available?

- We should at least be able to forget about toxic FRAs – CAD has always traded fixing risk as an SPS.

- Have your clients signed the fallback protocol?

- Are your CAD CSAs already CORRA-linked or do they require repapering?

- I am sure I am forgetting some….

CORRA First

Luckily, we have a well-thumbed playbook to refer to now, and the first step is likely transitioning as much interbank liquidity as possible away from CDOR and onto CORRA. This has traditionally been achieved through regulatory guidance and the issuance of “RFR First” dates whereby market conventions move on a given day. We have covered these for SONIA First, SOFR First and RFR First in XCCY.

So let’s check-in with the CAD markets. The CARR (Canadian Alternative Reference Rate) working group issued the following announcement:

- January 9th 2023 is the big day! We should see interdealer CAD markets move to CORRA decisively on that day.

- XCCY swap markets will be close behind, expecting to shift from CDOR vs SOFR to CORRA vs SOFR on March 27th.

- Swaptions will move on the same day as XCCY.

Is This Necessary?

I noted in the original 2019 blog, about 50% of the CAD market was already trading vs OIS. Has this continued to be the case? Not really….

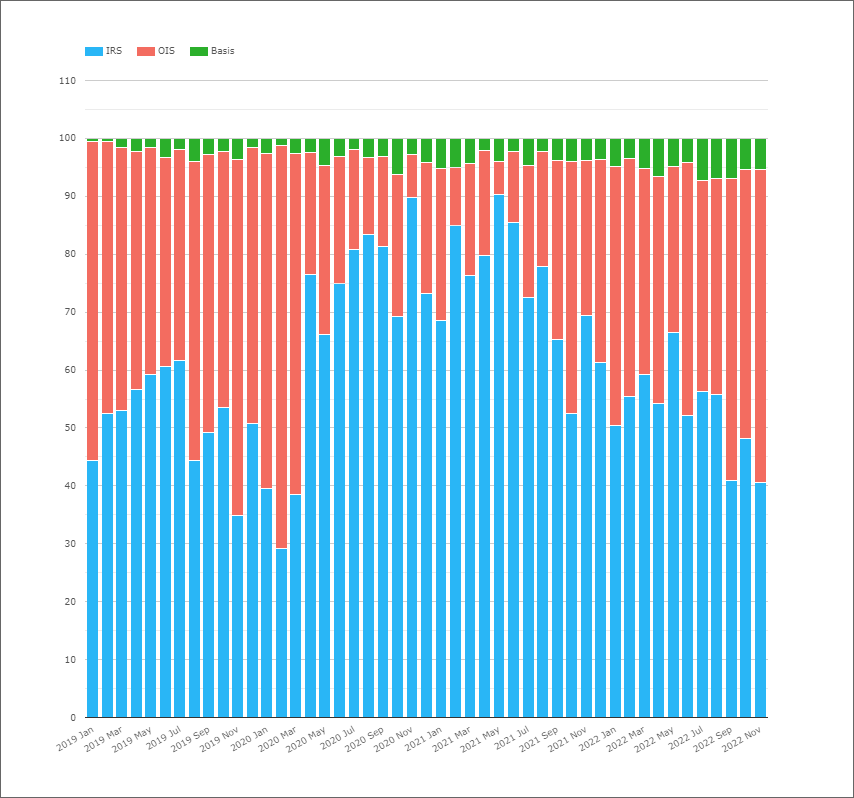

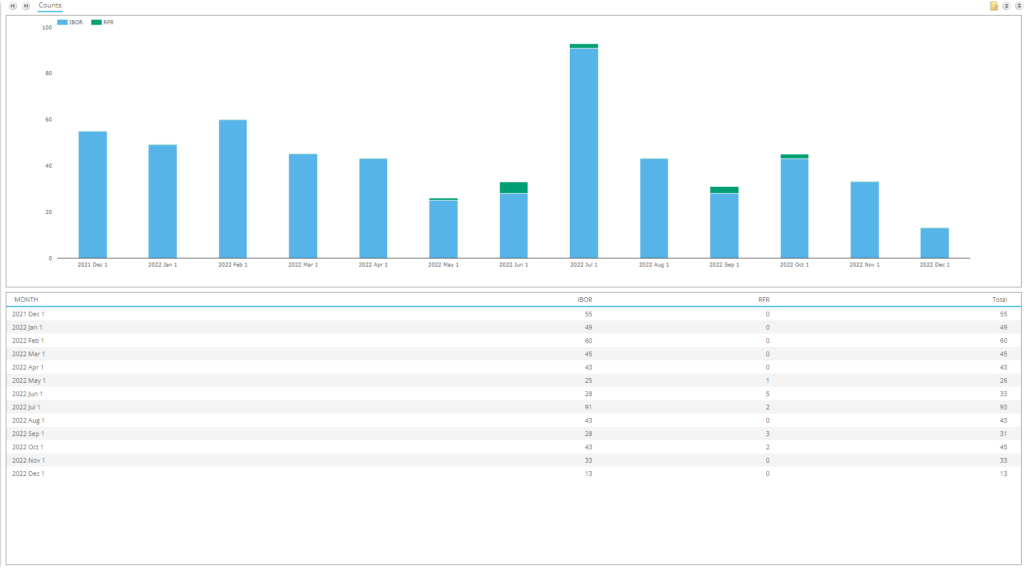

Showing;

- The split of Cleared CAD Interest Rate Derivatives by product type – including FRAs, IRS, OIS and Basis swaps.

- Volumes are measured by notional amount traded.

- FRAs do not trade in CAD markets. As I remarked way back in 2016 (!), same day currencies such as AUD and CAD have always traded FRAs as Single Period Swaps – this gives international banks time to make the settlements, given that the fixings are known too late in the day to make same day settlement achievable.

- It was true that CAD CORRA OIS accounted for about 50% of the market by notional volume in 2019.

- However, this was patently NOT the case in 2020 and 2021.

- Since May this year we have seen more and more OIS trading. Is this a result of more active central bank policy from the Bank of Canada or market participants taking heed of the cessation announcement?

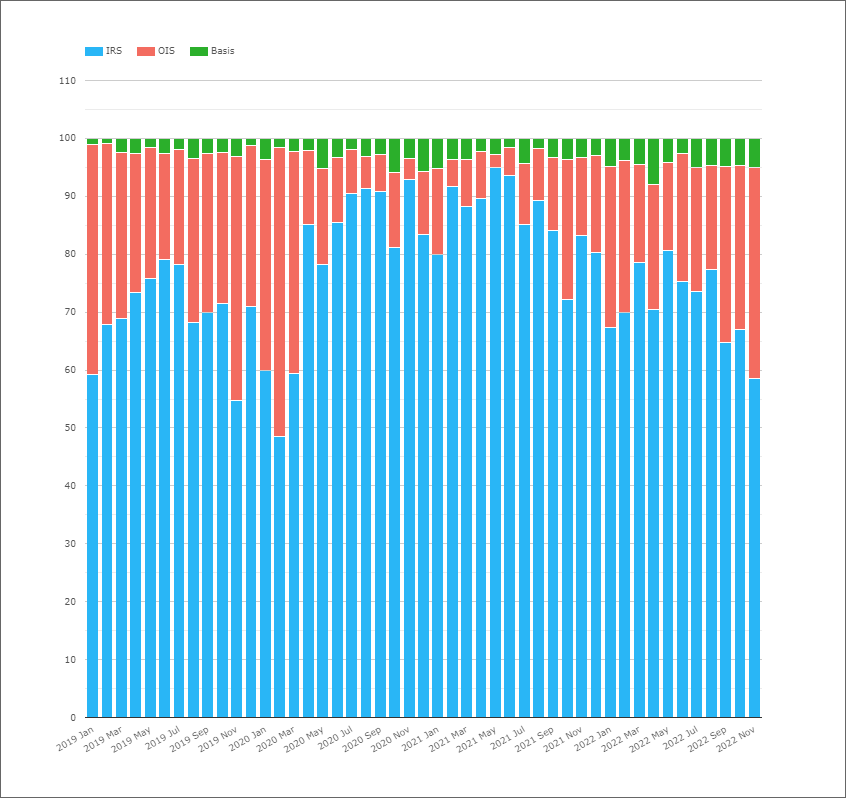

To answer that question, we need to look at the same data, but on a DV01 basis. This is very similar to how we run the ISDA-Clarus RFR Adoption Indicator – albeit CAD is not one of the six currencies that we currently monitor.

Showing;

- The split of Cleared CAD Interest Rate Derivatives by product type – including IRS, OIS and Basis swaps, but this time split by DV01 traded.

- The proportion of risk traded in IRS vs CDOR is consistently the most significant and largest part of the market.

- November 2022 was close to a record month for the proportion of risk moving through OIS products.

- Even then, it was only 36% of the overall market. IRS vs CDOR accounted for 59% of the risk.

- And we can see that in 2019, whilst there was a lot of notional traded as CORRA OIS, the amount of risk traded was much smaller.

- In 2019, a typical month would see anywhere between 20-40% of risk traded as an OIS.

- That has been remarkably similar in 2022, but the past 3 months have seen a shift toward OIS trading.

The DV01 chart highlights why it is necessary for regulators to step in with “CORRA First” as an initiative. The move is just too slow, or precarious even, without added regulatory impetus.

And Cross Currency?

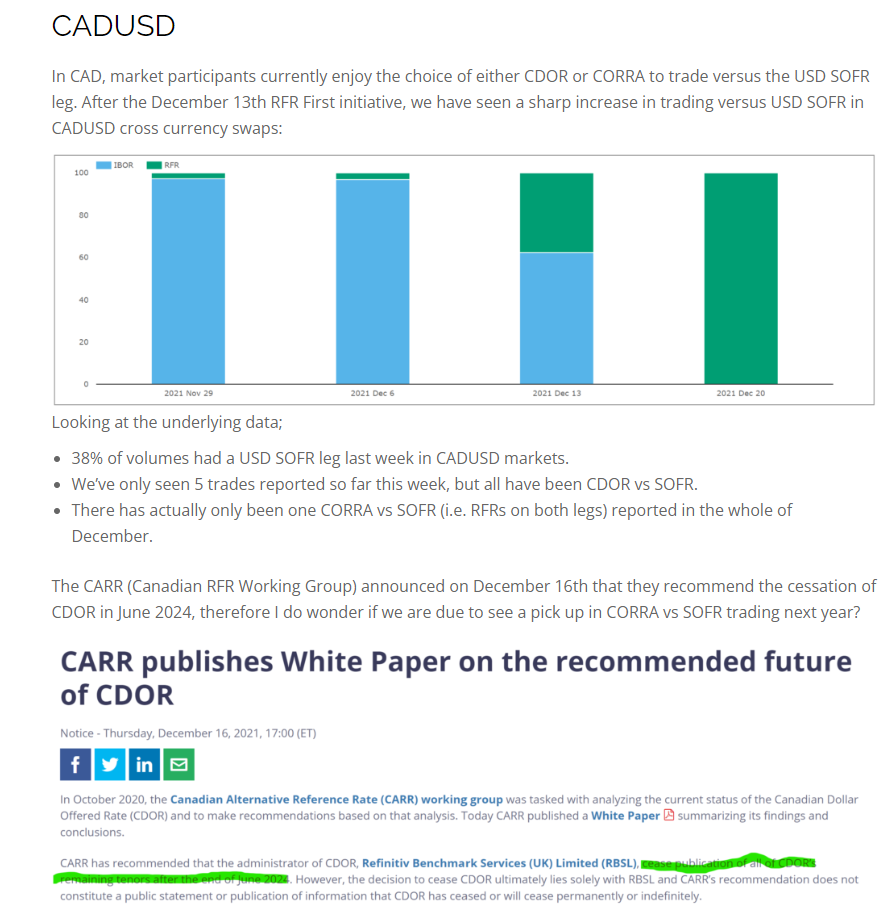

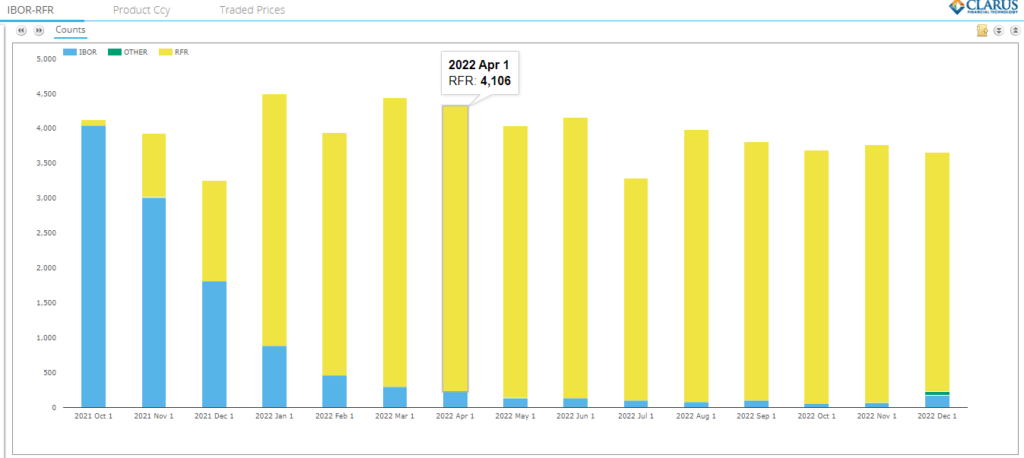

I reported at the end of 2021 on the success of RFR First in XCCY markets, and I provided the following colour on CADUSD in particular:

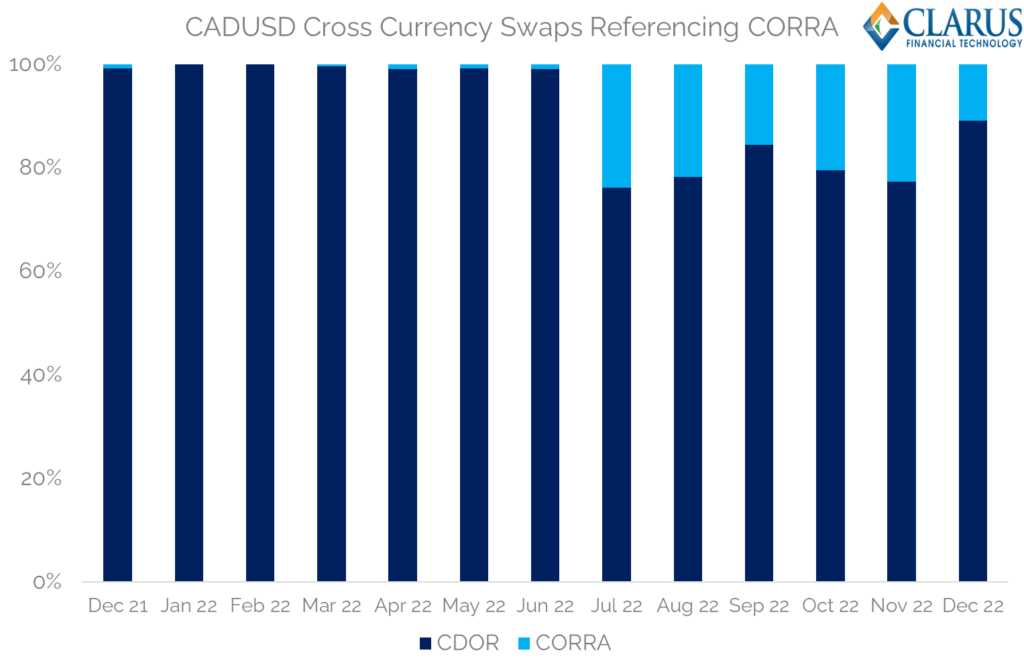

Only ONE CORRA vs SOFR swap?! Let’s refresh that number:

Showing;

- XCCY markets have come a long way but they still have a long way to go.

- CORRA vs SOFR did not really start trading until July 2022.

- Currently 20% of trades (by number) are conducted as CORRA vs SOFR.

- We’ve got 80% of the market still to change!

CAD Swaptions?

In the US DTCC SDR, only a handful of CAD Swaptions are reported each month. The Canadian DTCC SDR has a lot more swaptions reported, but still only about 10 have been versus CORRA all year:

Looking at the experience with SOFR First in USD markets, the switch to SOFR Swaptions happened very quickly in the US – we covered it here:

In Summary

- CAD interbank markets will see the first “CORRA First” initiative launched on 9th January 2023.

- CDOR will not cease until June 2024.

- Only 20-40% of CAD risk is currently traded versus CORRA in vanilla Rates markets.

- This is even lower for XCCY markets, and only a handful of CAD CORRA swaptions have been traded.

- 2023 will see large changes in Canadian markets.