ISDA and Clarus have now added CAD and SGD RFRs to the currencies we track in the RFR Adoption Indicator. This brings the total number of currencies up to 8:

- AUD

- CAD

- CHF

- EUR

- GBP

- JPY

- SGD

- USD

As we approach the end of USD LIBOR it will be interesting to see how other IBOR rates fare. CAD is in the middle of a “CORRA First” push, whilst SGD has done almost all of the heavy lifting already.

It has been a helpful exercise adding in the new currencies, both to put context on where different currencies are in terms of RFR reform, and to see how it moves the overall indicator.

We have included all of the history for CAD and SGD, going back to the beginning of the RFR Adoption Indicator in July 2018. This highlights the strength and breadth of Clarus data and will prove helpful to market participants through continued RFR transition exercises.

CAD

For those new to RFR transition in the Canadian market:

- CDOR will cease publication in June 2024.

- This requires Canadian Rates markets to transition to CORRA OIS.

- The first “CORRA First” initiative started on January 9th 2023.

I covered the transition in the following:

To add CAD “into the mix”, we identified the following volumes:

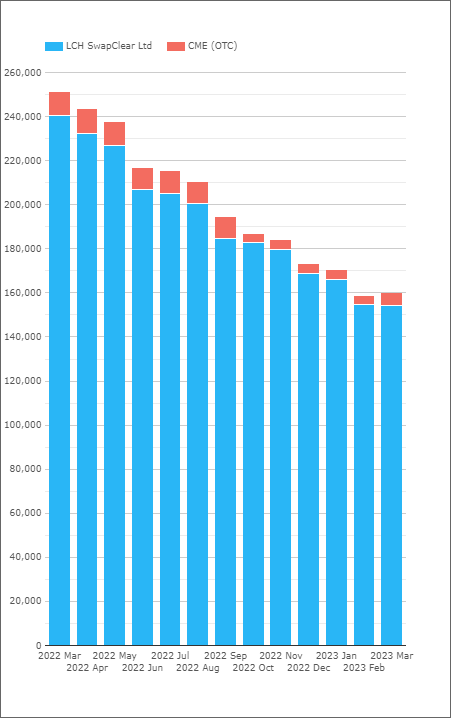

- LCH SwapClear – almost all CAD IRS are cleared here.

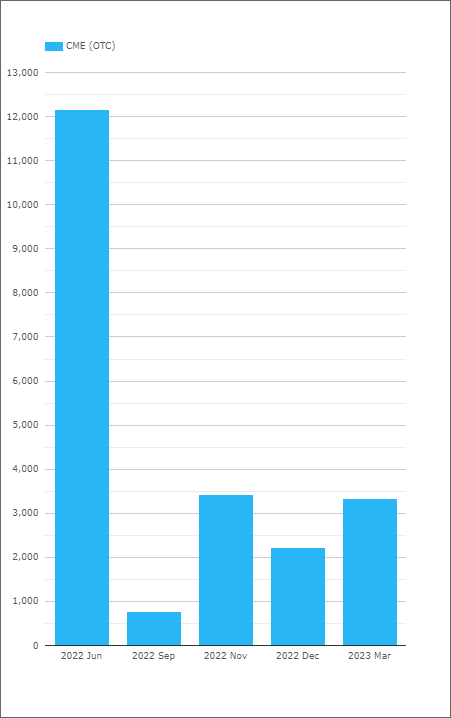

- CME – the volumes are somewhat periodic, but they are there:

- LCH and CME are the only two CCPs offering clearing of CAD OIS. For example, Eurex has not yet extended product support to include CAD:

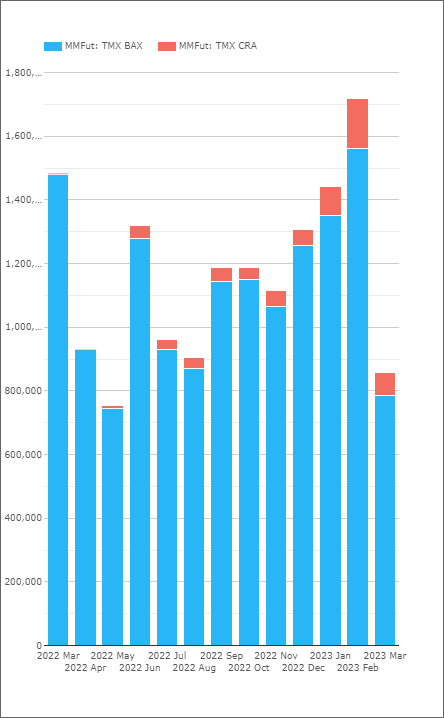

- CAD CORRA and CDOR (“BAX”) futures both trade at “TMX”, the Canadian-based exchange group. It looks like STIRs actually trade out of Montreal (I did not know that!):

- CORRA futures are in their infancy. It remains to be seen how quickly “CORRA First” initiatives can transition what has traditionally been patchy liquidity in the BAX into these “new” CORRA futures.

SGD

For those new to RFR transition in the Singaporean market:

- SOR will cease publication in June 2023 along with USD LIBOR.

- This has required Singaporean Rates markets to transition to SORA, the new RFR.

- LCH first offered SORA OIS for clearing back in May 2020.

- Most trading is already versus SORA. A “job well done” by the industry for once!

I covered the transition in the following:

To add SGD “into the mix”, we identified the following volumes:

- LCH SwapClear – almost all SGD IRS are cleared here.

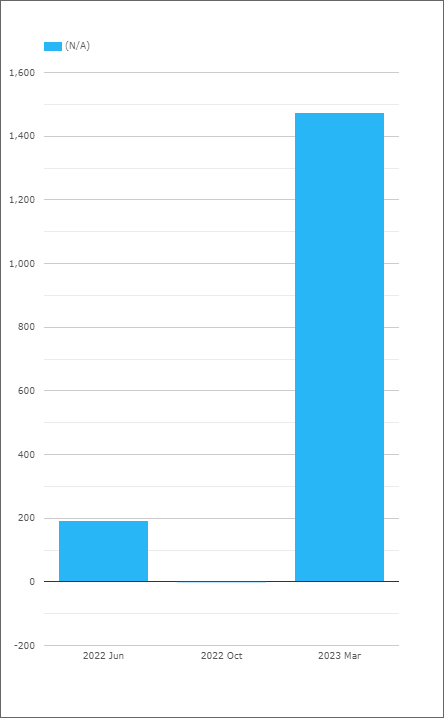

- CME – the volumes are very rare but we ensure coverage:

- SGX of course closed down OTC clearing some time ago, so this just leaves us with Futures markets to investigate…

- …which is another short section on this blog as there aren’t any money market futures for SGD rates either! There is a gap in the market if I ever saw one…..

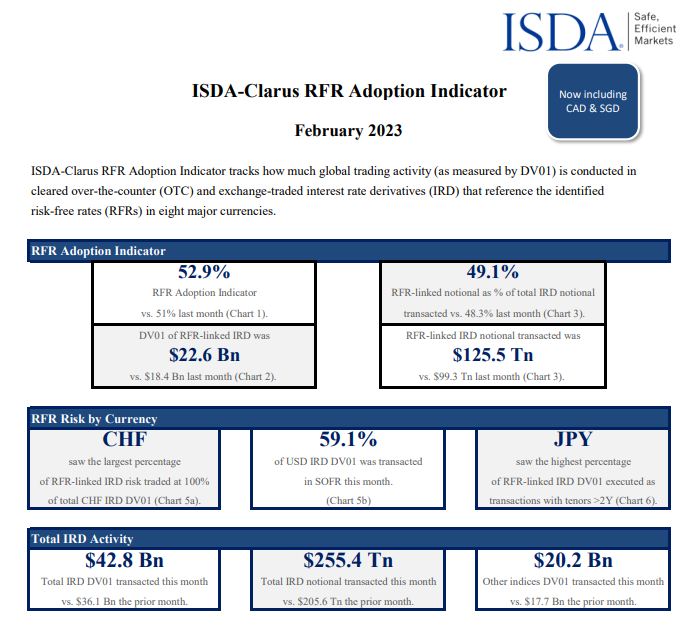

February 2023 RFR Adoption Indicator

All of this leads us to the latest publication of the ISDA-Clarus RFR Adoption Indicator:

Showing;

- The index has increased from 51.0% to to 52.9% – this includes the addition of CAD and SGD rates.

- SOFR adoption increased to 59.1%.

- 49% of total activity by notional was vs RFRs, still hovering around that 50% mark.

- Total trading activity was quite a bit higher than last month at $42.8Bn of DV01. What is all of this month’s volatility going to bring?!

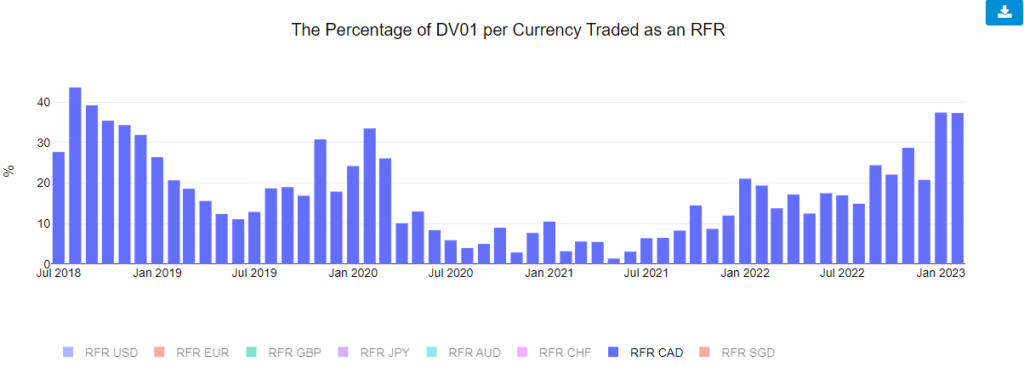

And of course, we need to introduce the new CAD and SGD data. Starting with CAD, which is a more nuanced story:

- The amount of risk traded vs CORRA in any month in CAD markets is very volatile.

- Like AUD, it is far more likely to be influenced by changing expectations in the market of central bank action rather than structural changes.

- In 2023 we now have both of these factors driving CORRA adoption.

- CORRA first in IRS markets (soon to be followed by XCCY), coupled with a massive global rally in Fixed Income.

- Expectations for where CORRA adoption will land for March 2023 must be pretty lofty!

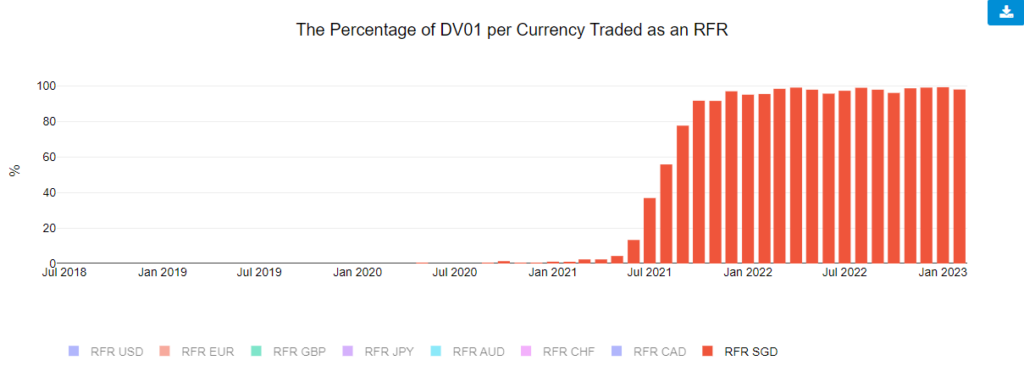

In SGD, it is not so much an adoption “story” as a fait-accompli:

- Since July 2021, SORA started an aggressive path to becoming the dominant index in SGD Rates trading.

- Ever since December 2021, almost 100% of Rates trading has been versus SORA.

- I guess the benefits of having a single index, a concentration of market players and no futures markets has made transition in SGD rates very rapid.

- An impressive success story for the industry I would suggest.

- The residual volumes (vs “Legacy Rates“) continue to be versus SGD IRS – the old “SOR” rate.

- The Open Interest in these old IRS tends to reduce at both LCH and CME each month, suggesting any new volumes are risk reducing in the main (along with maturities & terminations of the old stock):

In Summary

- RFR transition is happening across a number of currencies.

- We have added CAD and SGD to the ISDA-Clarus RFR Adoption Indicator, increasing the number of currencies being monitored to 8.

- RFR Adoption across these 8 currencies now stands at 52.9%.

- Check out all of the data at rfr.clarusft.com.