- Up to 89% of Rates risk is now trading versus CORRA in Canada.

- Dealer markets for OTC products show the most advanced transition.

- We look at the data and activity across CORRA and CDOR derivatives ahead of key dates for transition.

- After 30th June 2023, new activity in CDOR has to have a very good reason.

ISDA recently published a very informative webinar on the CDOR Transition:

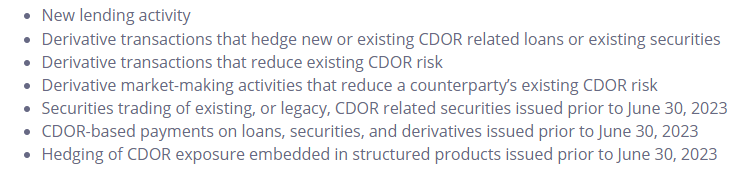

From this, I learned that 30th June 2023 (i.e. Friday!) is a big day for Canada Rates markets. Succinctly, no more new CDOR trading should take place after this date, other than for some well-defined exceptions. The CARR website is a great resource (from the Bank of Canada) and provides the list of allowed exceptions:

Whilst that list may look relatively long, it is also pretty clear that your day-to-day, BAU trading activity is now expected to transition to CORRA. Which gives us a great opportunity to check in on how that transition is going.

For some background, we have looked at RFR Transition in Canada a couple of times recently:

ISDA-Clarus RFR Adoption Indicator

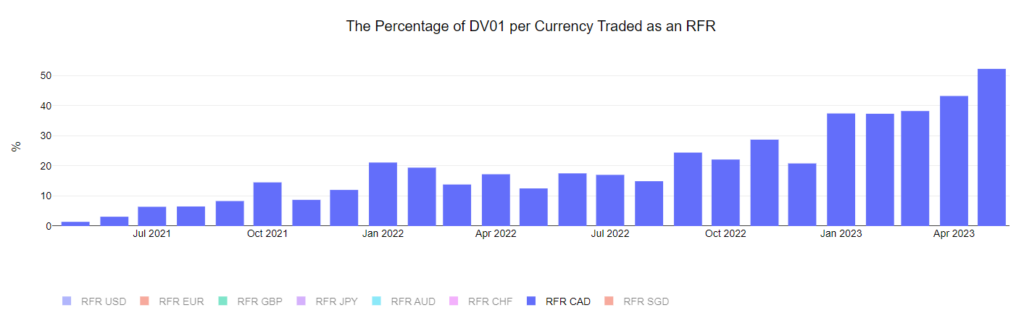

Seeing as I started with an ISDA Webinar, let’s check in on the progress CORRA adoption has made recently via the ISDA-Clarus RFR Adoption Indicator. Whilst much has been written about the on-going cessation of USD LIBOR (only three more fixings to go after today!), the data for CAD rates has also been moving in the right direction:

Showing;

- In case you are not already aware, the RFR Adoption Indicator tracks new trading activity in RFRs versus legacy rates in 8 currencies. It measures the risk traded, in DV01, of all cleared Rates products across both OTC and Exchange Traded (futures) derivatives markets.

- Recently, the percentage of risk traded as CORRA has increased to all-time highs.

- 52.2% of all CAD Rates risk was traded versus CORRA in May 2023.

- This is the first time that over half of new risk has been linked to CORRA derivatives.

- The rise in the index is certainly linked to the success of the “CORRA First” initiatives.

At 52%, CORRA is a little way behind SOFR adoption (which sits at 66%), but CDOR still has one year to run whilst USD LIBOR is in its final days!

Let’s see if we can learn more about the transition story in more detailed data.

SDRView

There are a few interesting charts here that are well worth considering.

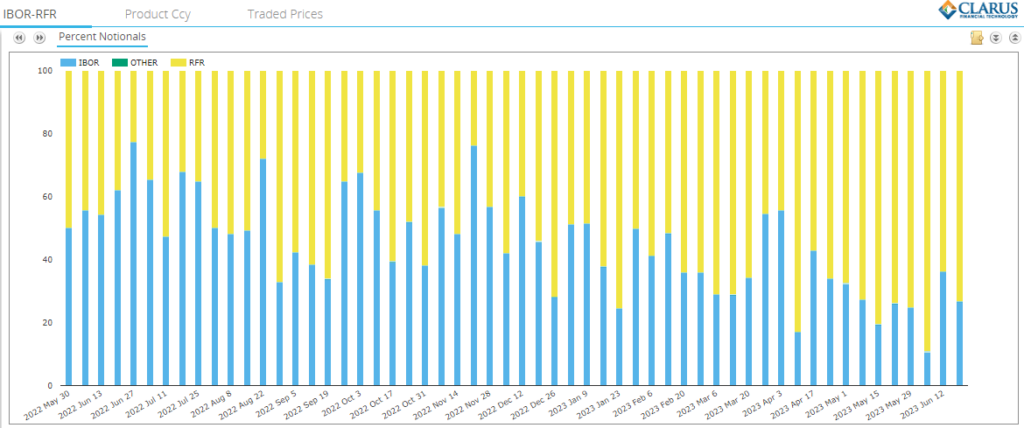

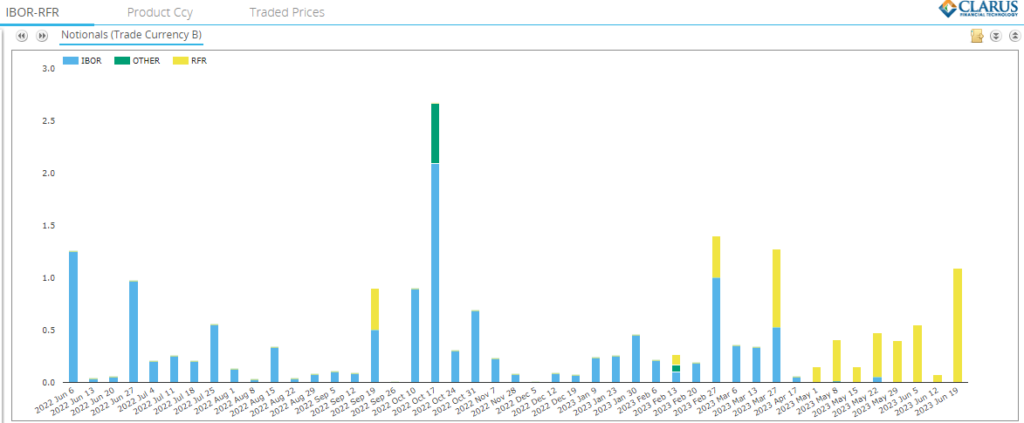

First up, just looking at notional amounts reported as CDOR or CORRA across all Rates products. From SDRView Researcher:

Showing;

- Percentage, as measured by notional, of Rates (and XCCY) products reported to US SDRs as either CDOR (“IBOR” on the chart) or CORRA (“RFR” on the chart).

- The most recent full week of activity saw 73% of notional traded vs CORRA.

- Whilst CORRA adoption is advancing, it varies quite a bit week-on-week by this measure.

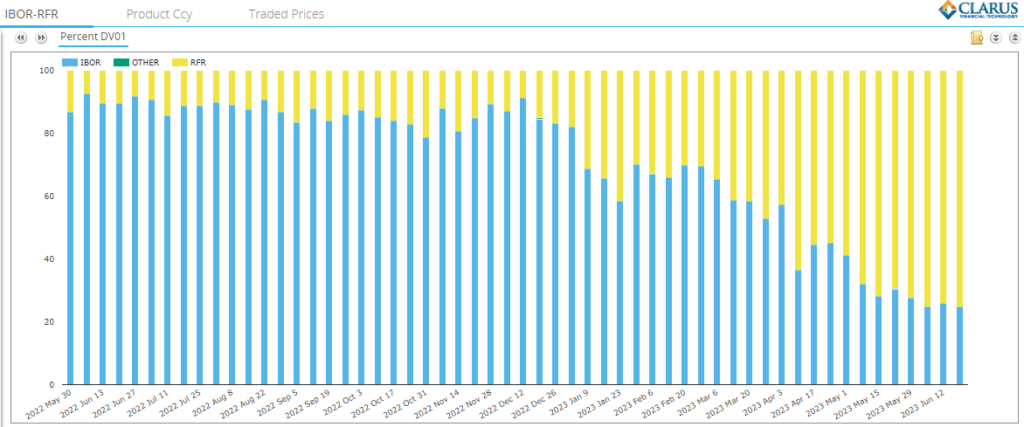

Running exactly the same time-series but on a DV01 basis shows a much more progressive march toward CORRA trading:

Showing;

- A gradual march toward CORRA trading, with 75% of total Risk transacted versus CORRA in the most recent weeks.

- This is one of the more compelling charts that I have seen, showing the success of CORRA-first.

Another helpful chart is the complete switch of non-linear products to CORRA. Almost no CDOR Swaptions or Caps/Floors have been reported to SDRs since the beginning of May 2023:

Clients and Dealers

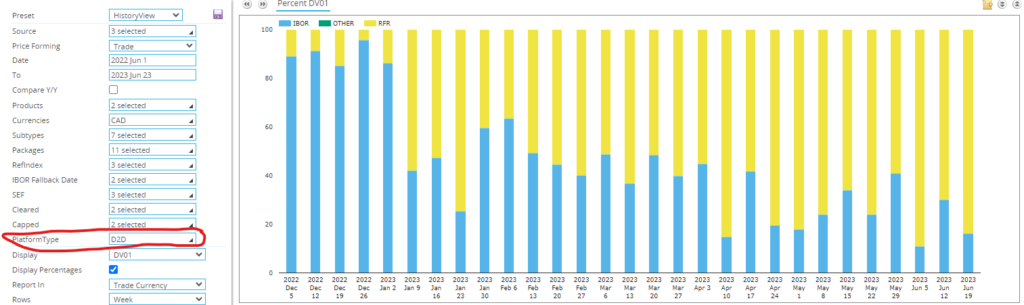

Staying with SDR data again, we looked previously at the difference in CORRA uptake between Dealer and Client trading. Replicating that same analysis:

On Dealer to Dealer platforms (highlighted above);

- Up to 89% of risk in any given week is now transacted versus CORRA.

- The increase in CORRA trading has been gradual week-on-week.

- The Dealer community will naturally have some new CDOR risk originating from the list of exceptions (see above), therefore we don’t necessarily expect this metric to head to exactly 100%.

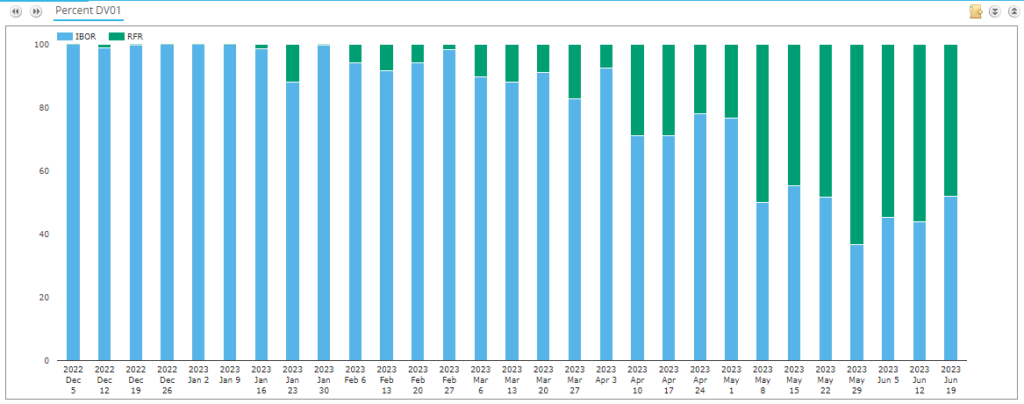

Looking at Clients on the other hand;

(Apologies for the switch in colours on this chart, the google auto-generated charts are not 100% foolproof!).

With RFR risk in green this time:

- Over 50% of risk transacted on D2C SEFs (i.e. Tradeweb and Bloomberg) were still versus CDOR in recent weeks.

- Now, we don’t know for sure whether this was because clients were in a mad rush to reduce their CDOR exposures whilst there is still liquidity available…

- That would be a charitable read on the data….

- …rather than just stating Clients are slower to transition than the dealer community.

- Either way, with more and more liquidity transferring to CORRA products, we expect the D2C metrics to catch-up with the overall market relatively quickly.

Futures

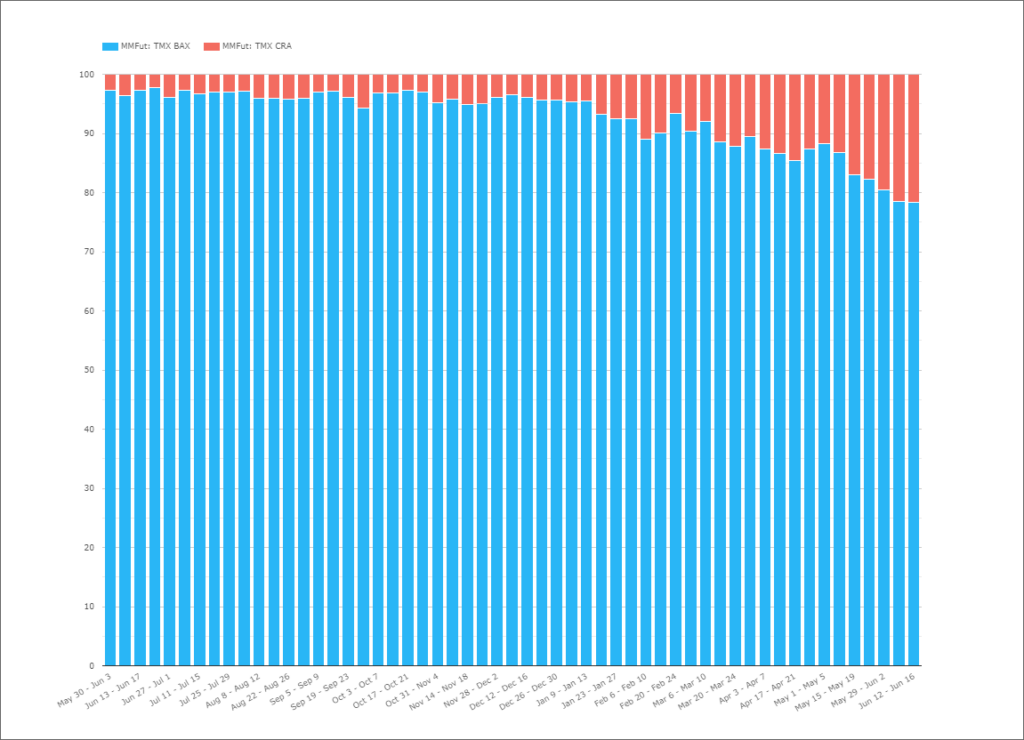

What is interesting with this transition to CORRA is that Exchange Traded Derivatives are subject to the same timelines as OTC markets. But we know from IBOR transition in other markets that Futures markets are much slower to transition than in OTC. We see this same scenario playing out in Canadian Rates as well. From our CCPView data:

Showing;

- Percentage of risk traded as either CAD BAX (CDOR) contracts in Blue versus risk traded in CAD CRA (CORRA) contracts in Red.

- These are both traded at TMX – you can find contract details and the transition website here.

- There is more and more risk being transacted vs CORRA.

- But at 21% it is much lower than in OTC markets.

- Much as happened with Eurodollars, there is also a plan to convert BAX contracts to CORRA. The plan can be found here.

Some on-going BAX activity is expected as people hedge fixing risk on existing swaps. That will continue until Fallbacks kick-in and the fixings become CORRA-linked instead. However, there is clearly activity outside of fixing-related risk that still needs to transition.

In Summary

- Up to 89% of CAD derivatives risk is now trading versus CORRA.

- 30th June 2023 is an important date in the transition of CAD rates to an RFR world as new trading of CDOR risk is expected to largely cease from this date.

- The uptake of CORRA trading varies across dealers and clients and between Futures and Swaps/OTC markets.

- There will be a number of other markets going through RFR transition over the coming years even after USD LIBOR disappears at the end of this month.