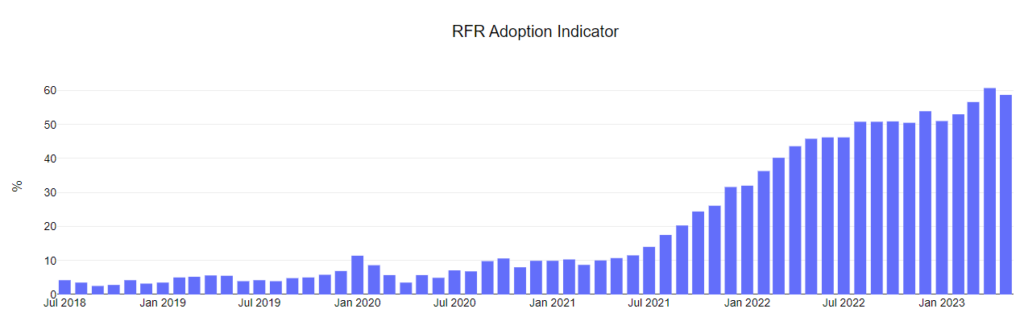

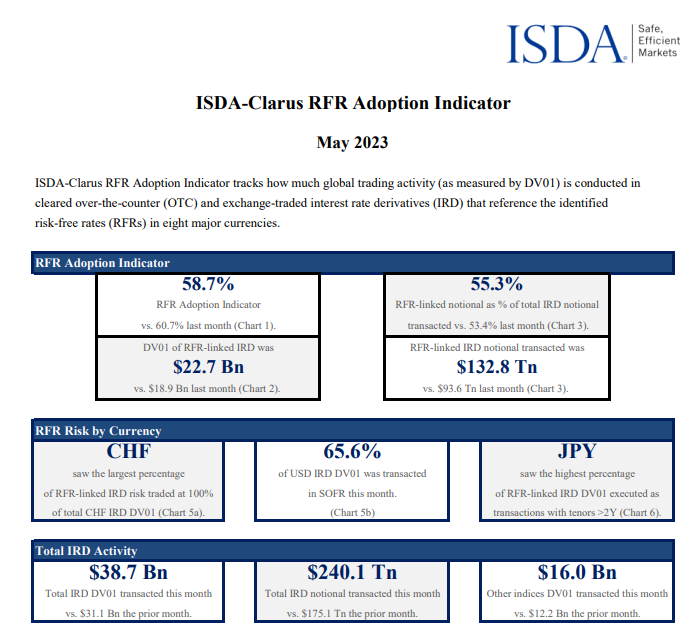

- RFR Adoption was at 58.7% in May 2023.

- USD SOFR Adoption was at 65.6%.

- Find out why both of these figures were lower than expected…

- …and what that could mean for trading trends in the future.

The latest ISDA-Clarus RFR Adoption Indicator has been published for May 2023 so I asked ChatGPT about the next report:

I love how it states that because it is a language model it doesn’t predict the future. Rather than simply stating “you cannot predict the future smart @rse”. From my experience with ChatGPT, I found that it primarily serves as a different (new?) way of serving up existing information/content in a very human-like way. But it doesn’t create new stuff – be that blog content or using data to predict/analyse. At least, in this instance, it gives everyone some excellent advice, which is to subscribe to our newsletter.

Irrespective of whether a prediction is created by me or by an AI model, May’s RFR Adoption Indicator serves as a great example of how wrong any prediction can be. I am sure I was not alone in expecting another decent jump higher for both overall RFR trading and SOFR adoption – mainly as a result of the LCH SwapClear SOFR conversion exercise.

SOFR Conversion

I doubt anyone will appreciate me reminding them, but many weekends this year have been devoted to physically converting outstanding USD LIBOR swaps at CCPs to vanilla SOFR swaps. The CCPs have not used the ISDA Fallbacks, but have rather converted old LIBOR stock into “vanilla” SOFR swaps. LCH SwapClear completed this process in May:

This followed on from CME converting both Eurodollar Futures and SOFR Swaps in April:

- CME converted your Eurodollars. This is what happened next.

- Do you know how much now trades in RFRs after the CME conversion exercises?

For background to how these processes worked, please refer to our primer on CCP Conversion exercises themselves:

In April 2023, seemingly as a result of the SOFR conversion exercises at CME, the ISDA-Clarus RFR Adoption Indicator saw a significant jump higher, to a new all time high over 60%.

It was a fair assumption that the LCH SwapClear conversion exercise, in May 2023, should have had a similar effect.

However, the latest data shows that this was not the case. Read on to see what happened!

RFR Trading Did Not Increase in May. Which is Weird.

The report summary shows;

- The index decreased (from its all-time high last month) to 58.7%, 2% lower.

- SOFR adoption reduced to 65.6%, from 70.9% last month.

- RFR trading also reduced in EUR, down 2% to 27.1% for €STR.

- With the two largest markets reducing their RFR adoption, it clearly pulled the overall index lower.

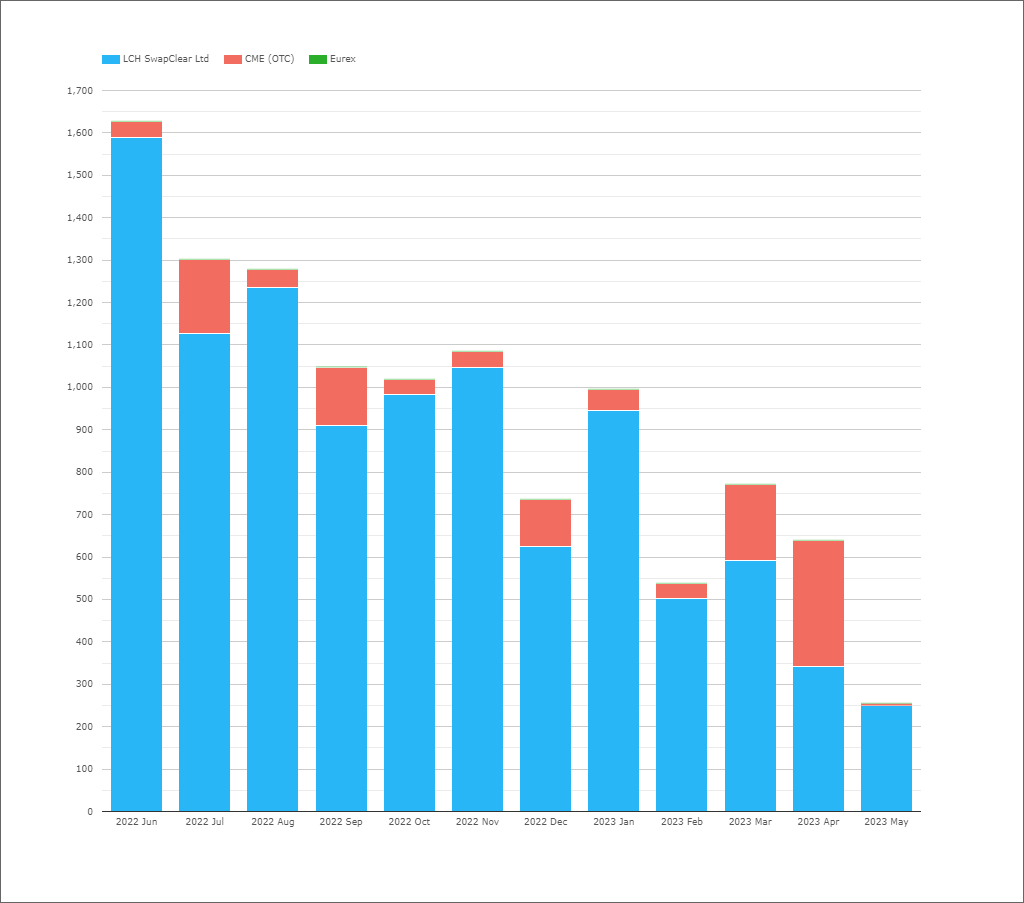

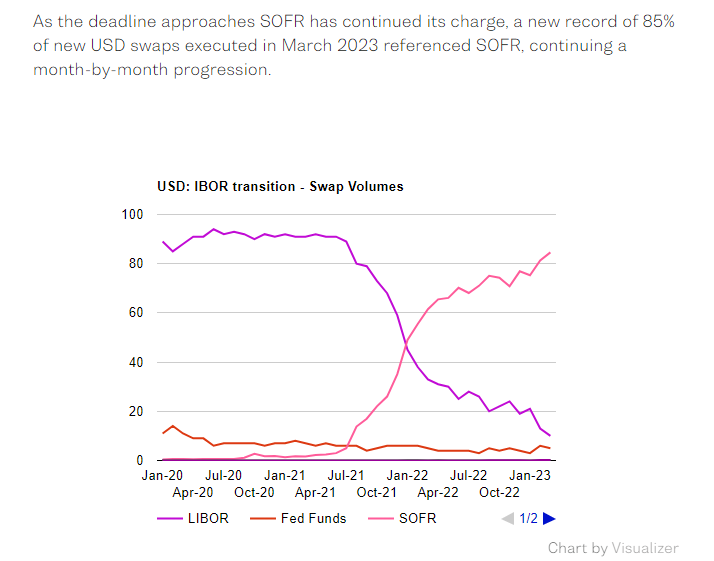

Let’s dwell on that SOFR number for a bit. The portion of the market that traded vs SOFR decreased in the penultimate trading month ahead of USD LIBOR cessation. What gives?

To immediately put some minds at ease, we can see that it wasn’t due to a final rush to trade USD LIBOR!

This is the closest I can give to a warm hug to you LIBOR Transition managers out there. It’s OKAY! USD LIBOR isn’t making a comeback, it really is going to disappear at the end of this month. The chart above shows that in May 2023;

- The lowest amount of USD DV01 ever traded versus USD LIBOR since records began.

- There was basically no USD LIBOR risk traded at CME – all the trading at CME is now in SOFR products across both Futures and Swaps.

- May was the first time that less than $750bn in new USD-LIBOR linked notional was cleared in a month (okay, that is still quite a big number 😛 ).

I was relieved to see this chart because it would have been really embarrassing over here on the Clarus Blog if we had somehow missed a reprieve for USD LIBOR!

OSTTRA have also recently pointed out that, by trade count, May 2023 was a record month for SOFR activity across their swaps affirmation platform, MarkitWire:

And this is replicated in SDR data, which shows an even higher percentage of USD Rates trades – 92% – referenced SOFR. That suggests that USD LIBOR trading is a little bit more prevalent in Europe and Asia than the US, but not by much:

Showing;

- US Persons data from SDRView Researcher.

- 92% of USD Rates trades, by trade count, reported to SDRs in May 2023 referenced the “RFR” (SOFR in this case).

- This was a new all-time high.

- Interestingly, 4.7% of trades referenced LIBOR, whilst 3.7% (i.e. almost the same number) referenced other indices.

- Other indices include BSBY and Term SOFR, but also Fed Funds.

So let’s talk about Fed Funds trading.

Fed Funds Trading Took Off

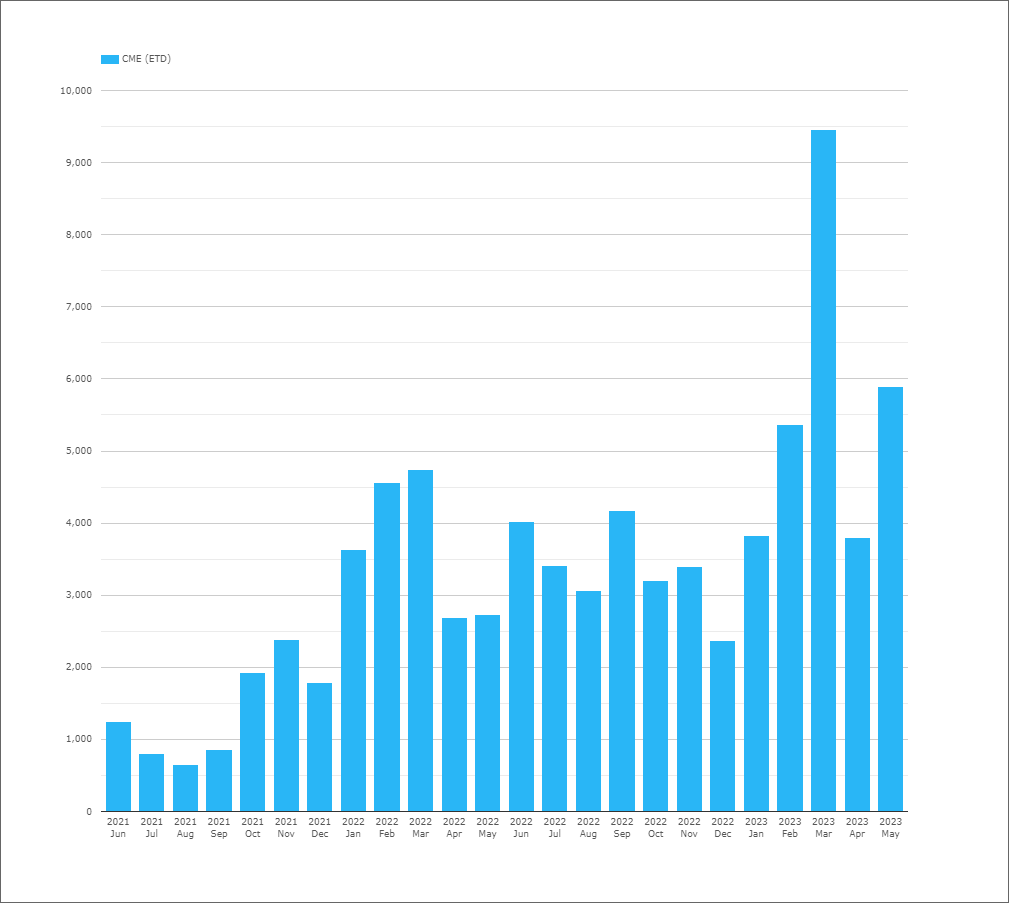

In CME Futures markets, we saw the largest amount of Fed Funds risk traded outside of an IMM roll month, since the Fed started hiking rates:

The chart shows that nearly $6Bn of DV01 risk traded in Fed Funds futures last month – a huge amount by anyone’s book! If this had been down around the more “typical” (but still elevated) $4bn, we would have seen a similar level of SOFR adoption.

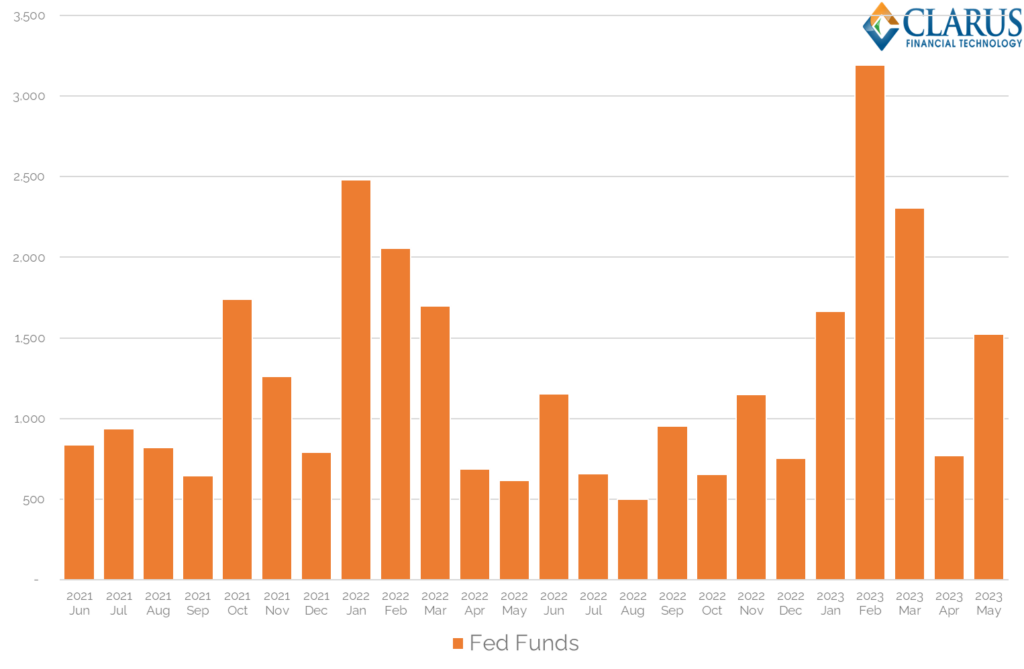

The large amount of Fed Funds activity was also replicated in Swaps trading:

Showing;

- DV01 traded in Fed Funds OIS each month.

- We can see that May 2023 saw more risk traded than in April, although it was lower than in both January and February.

- It was a relatively large amount of risk at $1.5bn DV01, but not unusually high.

Overall, both Futures and Swaps markets saw more activity in Fed Funds than previous months. With the Fed again “in play” this month, this trend could well continue. Recall, I wrote a blog about this potential dynamic at the beginning of this year:

In Summary

- The RFR Adoption Indicator decreased this month to below 60%.

- This was a huge surprise given that a large chunk of USD LIBOR risk was converted to USD SOFR at LCH SwapClear during the month.

- In terms of new trading activity, we saw a lot of risk transacted versus Fed Funds in the USD market.

- Therefore, whilst USD LIBOR linked activity hit new all time lows, there was risk transfer activity outside of SOFR.

- The balance between Fed Funds and SOFR risk will be an interesting one to continue to monitor even after LIBOR cessation.