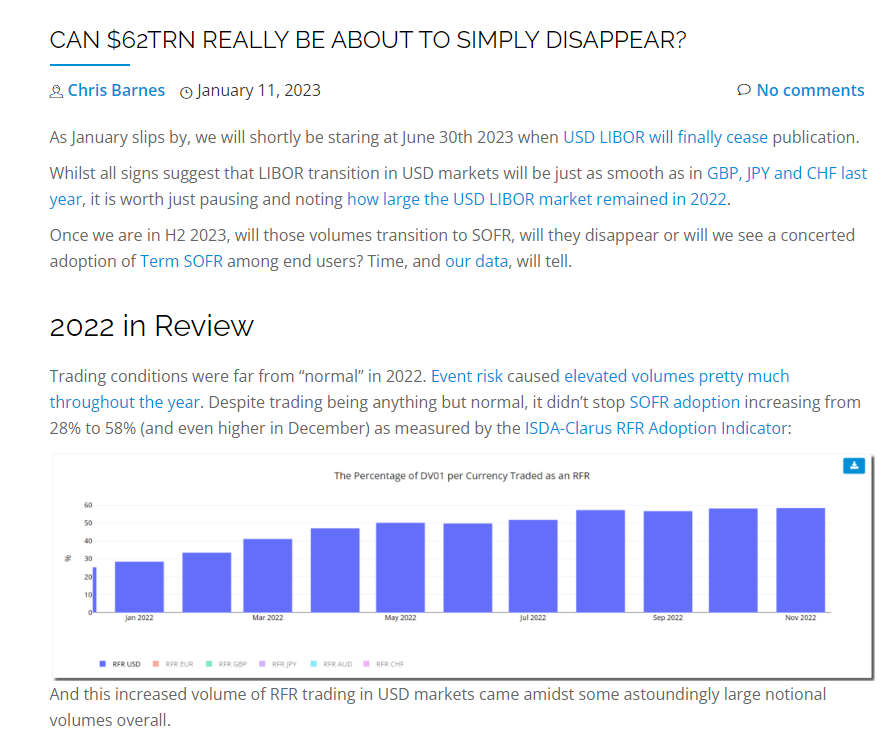

As recently as January I posed the question:

That blog was written in response to the fact that 2022 continued to see plenty of USD LIBOR risk sent to CCPs. Could all of that trading just stop in time for the final cessation of USD LIBOR in June 2023?

Following on from the recent CME conversion exercises for Eurodollars and Swaps, we have now seen the final LCH SwapClear conversion exercise. This converted USD LIBOR swaps cleared at SwapClear into USD SOFR swaps:

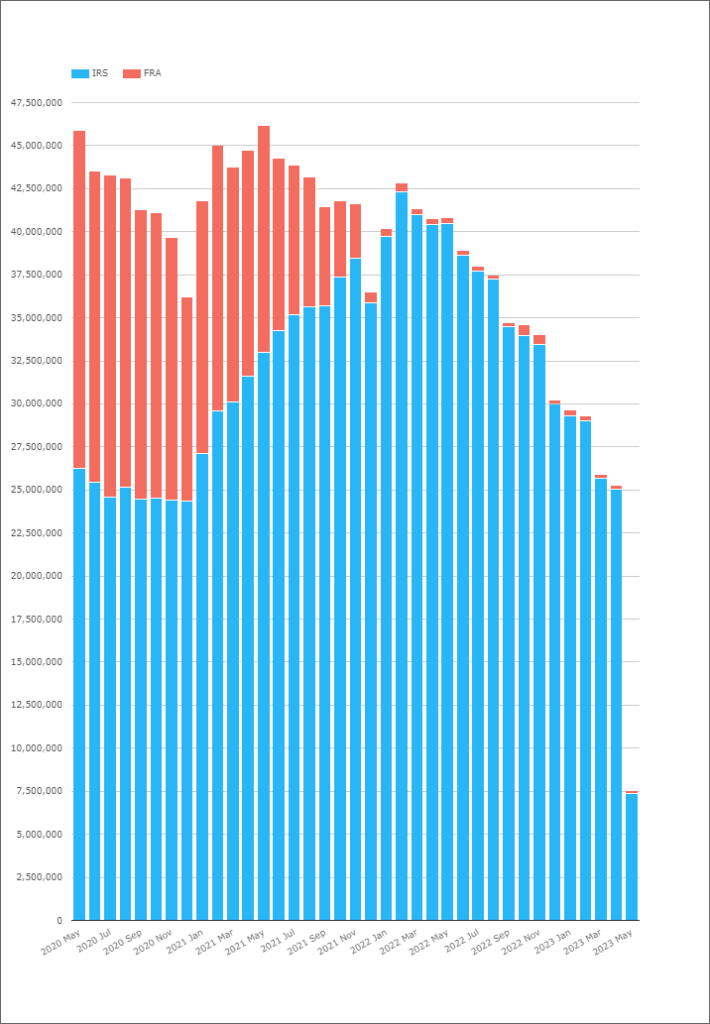

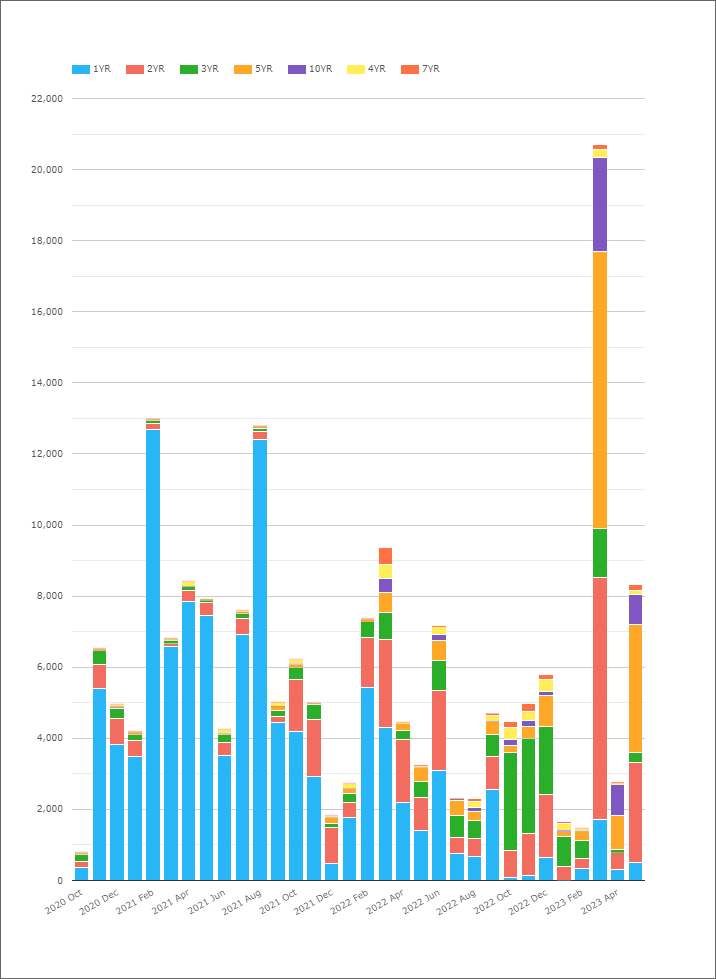

CCPView provides the data behind the conversion, a nice summary of which can be seen in the huge change in Open Interest in USD products:

Showing;

- In May 2020, there was $45.9Trn of outstanding USD LIBOR linked notional at LCH SwapClear across USD LIBOR IRS and USD LIBOR FRAs.

- In May 2021, there was $46.2Trn in outstanding USD LIBOR-linked notional. Amazing to think USD LIBOR exposures were still increasing two years ago.

- Open Interest started to steadily decline from February 2022.

- At the end of last year, there was still more than $30.2Trn of outstanding notional.

- $17.7Trn of outstanding notional was removed as a result of the conversion exercise at SwapClear.

- We now stand at an outstanding notional of “just” $7.5Trn, which will roll off as the final USD LIBOR-linked cashflows settle over the coming months.

Please note that these numbers are all “singled counted” – consistent with our Principles and Data Sources – and so will be different to those you read in the LCH press release.

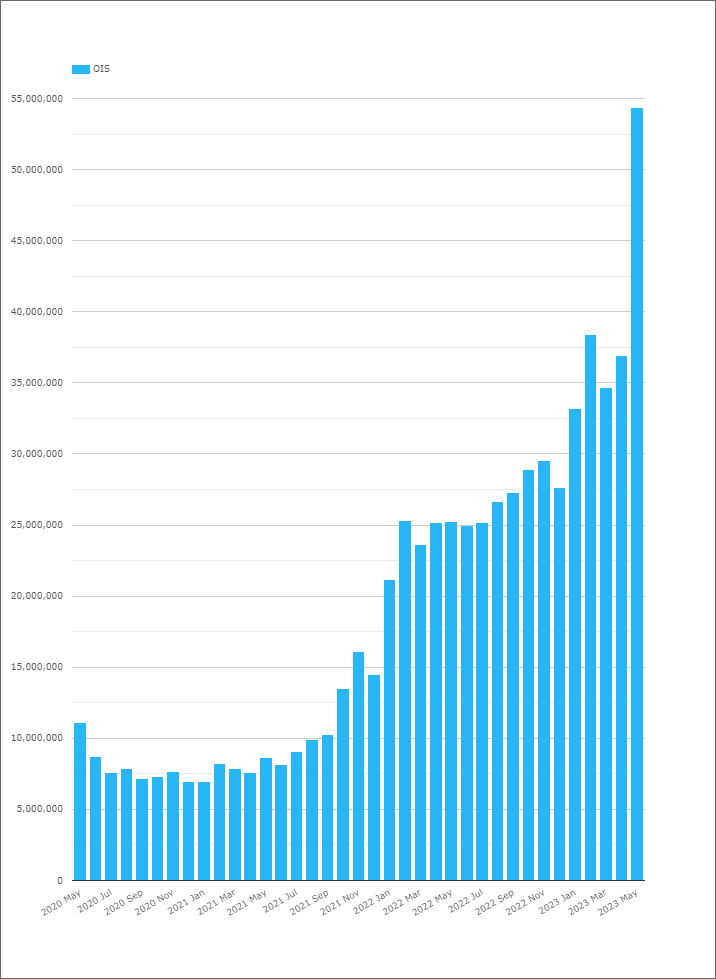

SOFR

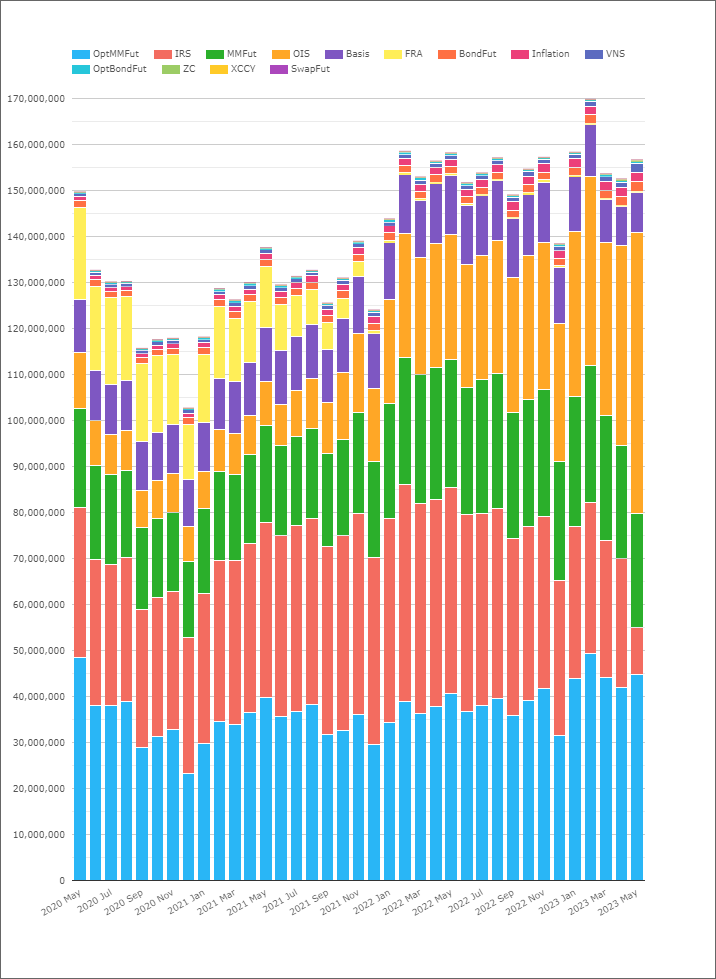

Completing the picture should be the inverse in SOFR OIS. We are all expecting the Open Interest at LCH SwapClear to increase by about $17Trn, right? It’s an impressive chart:

For once, we would be about right in our assumptions! The chart shows:

- April 2023 saw an Open Interest in USD OIS (across both SOFR and Fed Funds) of $36.9Trn

- May 2023 now sees an Open Interest in USD OIS of $54.36Trn

- An increase of $17.45Trn.

- Nice to be able to reconcile the figures so readily.

Open Interest

We don’t look at Open Interest figures too often, but these conversion exercises reveal why it continues to be valuable data – despite the sheer size of the figures being a constant surprise!

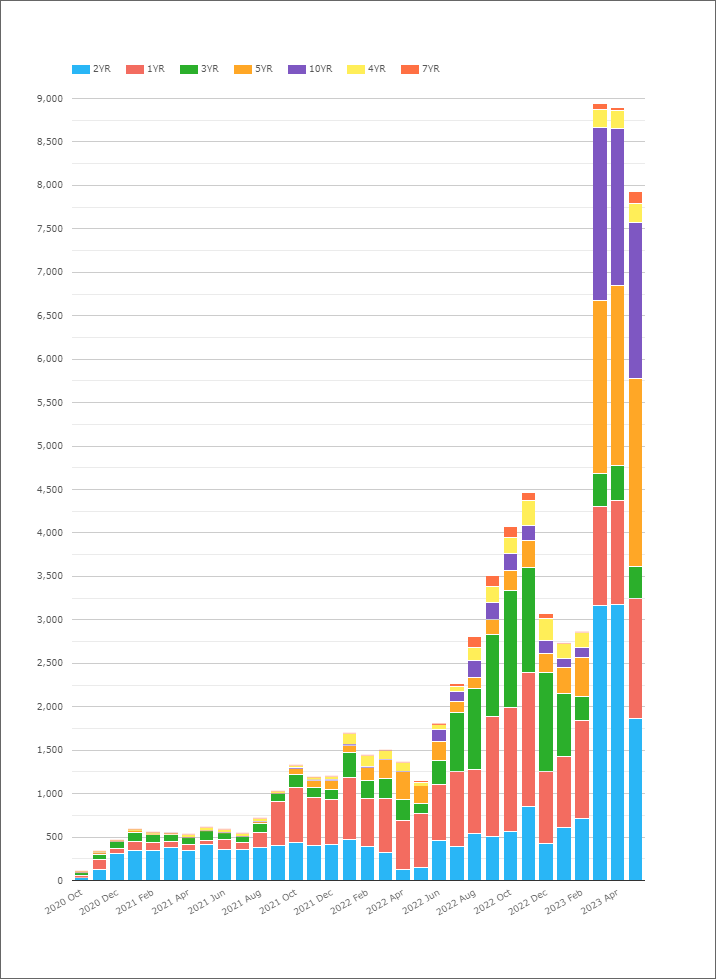

Comparing the impact on Open Interest in the Swaps world (with customisable OTC contracts and “on the run” details changing daily) to the almost zero change in SOFR Futures (with standardised contracts resulting in lots of netting opportunities) is a really stark reminder of where we could have been if MAC swaps had taken off (anyone remember them? We have a few blogs on them!). Will it reignite interest in MAC, or will ERIS SOFR futures see even more interest now? Remember we have data on ERIS SOFR activity as well in CCPView:

The Open Interest in these ERIS SOFR futures paints a little bit of a different story to the monthly volumes (see below, they are very variable month on month) so it will be an interesting one to monitor over the coming months:

Scores on the Doors

Ultimately, what do we care about? We wanted a smooth, riskless transition from USD LIBOR to USD SOFR. If overall Open Interest across both Swaps and Futures, LIBOR and SOFR, stays pretty constant as a result of transition, that would argue that transition had been smooth (for most market participants).

If we take an arbitrary starting point of May 2020:

- Total USD Open Interest across all Rates products stood at almost exactly $150Trn.

- As of May 2023 it has now increased to $156.7Trn.

- You can subtract the $7.5Trn in OI of USD IRS (see today’s first chart above) from that figure as that will very shortly roll off.

- Meaning, after a lot of hard work, we are pretty much exactly where we started in May 2020.

This argues that the depth of liquidity pools, number of active market participants and trading as a whole have remained fairly consistent throughout transition.

That is surely an achievement worth celebrating?