- Clarus tools calculate margin under LCH, CME and ISDA SIMM™.

- It is a natural question to compare the three models.

- There are interesting differences across currencies and tenors.

- We find that SIMM is up to 37% higher than at a CCP.

At last….!

This blog has been sitting in my “to-do” box for long enough. It is such a natural question to ask, particularly when you have the tools to answer it. Our CHARM margin analytics allows us to answer exactly these types of questions. So let’s plug some numbers in for vanilla Interest Rate Swaps. We’ll look at other product types in the future.

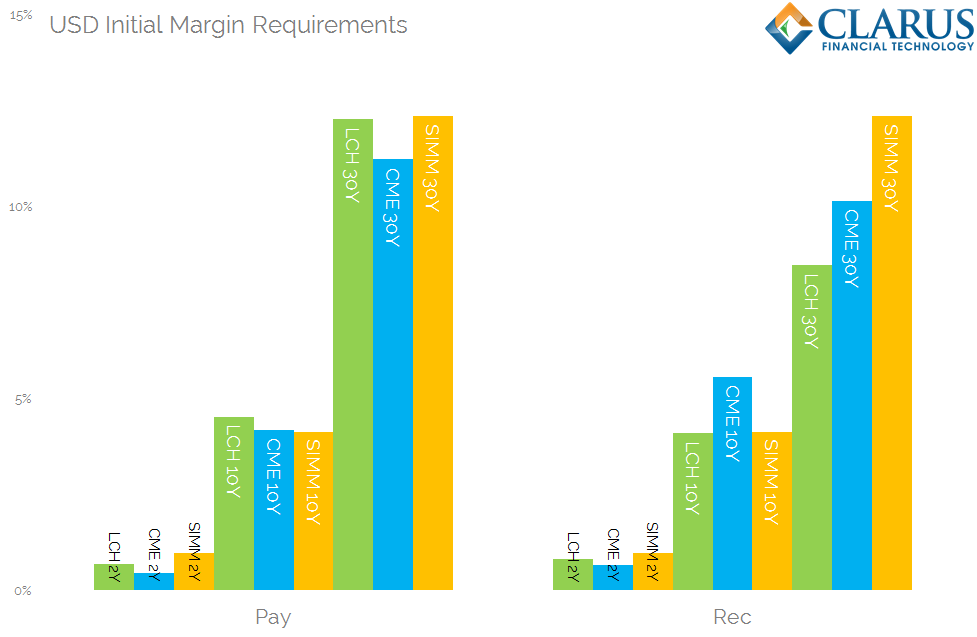

USD Interest Rate Swaps

First up, let’s look at the largest market – USD swaps.

Showing;

- The Initial Margin required to be posted for a standalone USD IRS as a percentage of notional

- Maturities of 2y, 10y and 30y are analysed under 3 different margin models – the LCH, CME and ISDA SIMM™.

- CCP models are not symmetrical – generally, a Pay Fixed USD IRS has a higher IM requirement than a Receive Fixed IRS. Although as Tod explored last week, times they are a-changin’.

- ISDA SIMM™ is symmetrical – the margin required for a Pay fixed position is the same as for a Receive fixed position.

- For Pay fixed positions, SIMM is very similar to the CCP models.

- SIMM is only noticeably higher than both CCPs for 30 year Receivers in USD swaps.

- For 10 year positions, SIMM is the lowest IM – whether it is a pay fixed or a receive fixed position. That might be a surprise to some people.

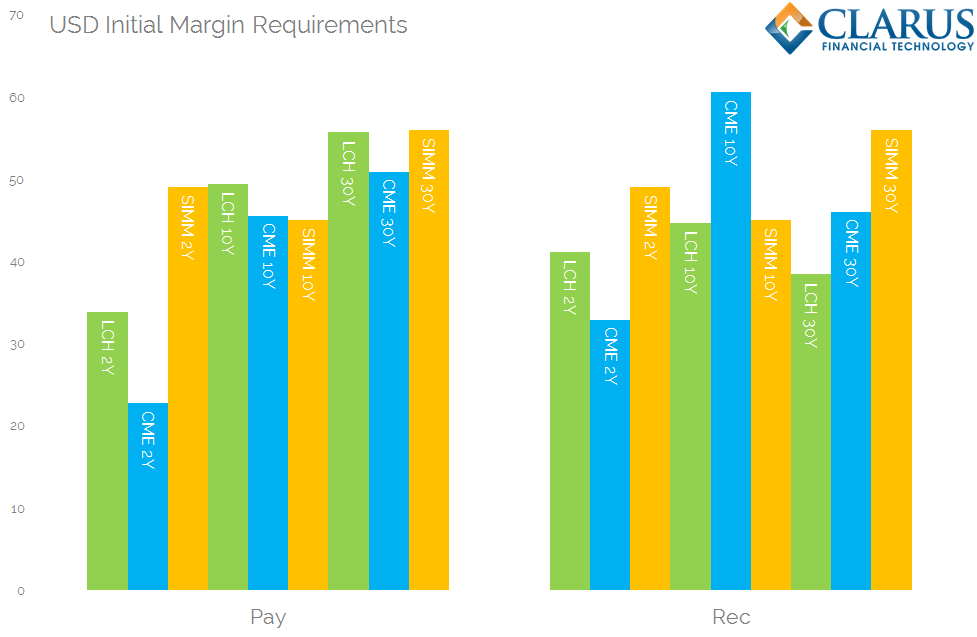

The chart above does not make any allowances for duration – we are looking at the percentage as face value of the swap. As with most analysis in the swaps market, we see a more accurate picture if we look at this on a DV01 basis. So let’s re-state the chart, but look at the Initial Margin required in basis points of risk – i.e. let’s divide by the DV01 of each swap.

Showing;

- For Payer swaps, CME and LCH margins increase as maturity increases. This is not always the case for SIMM.

- The highest IM of any swap in basis point terms is a 10 year Receiver at CME.

- The lowest IM of any swap is a 2 year Payer at CME.

- Out of the six combinations of Pay/Rec and tenor, SIMM is only meaningfully higher than both CCPs in 50% of cases – a 30 year Receiver swap, and all 2 year swaps.

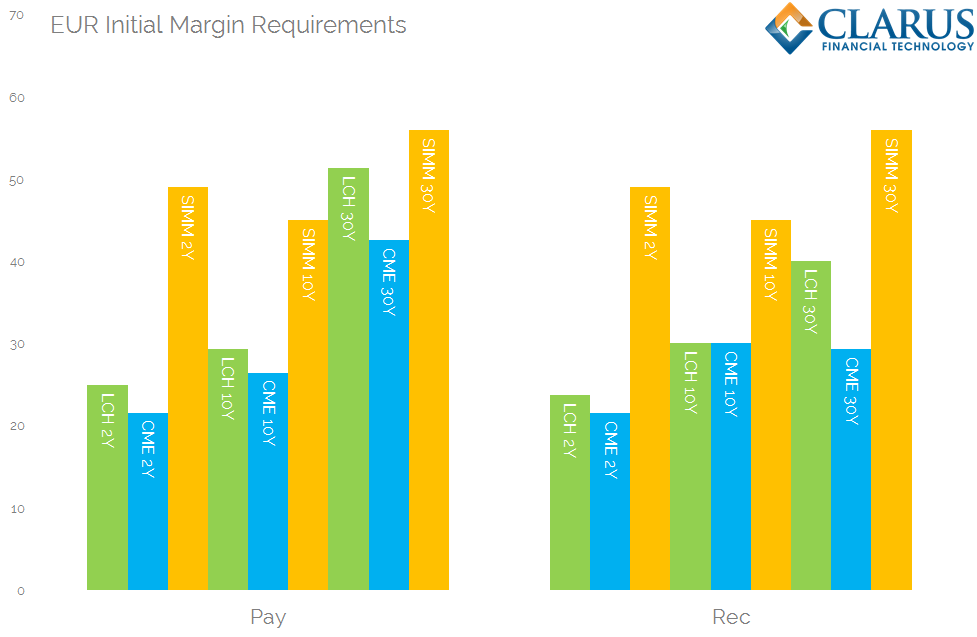

EUR Interest Rate Swaps

For all “normal” volatility currencies, such as USD and EUR, SIMM uses the same risk weightings. This means that the IM requirement under SIMM for a given size of DV01 is the same in both USD and EUR. So let’s compare this with the CCP models – again looking at it in basis points of risk:

Showing;

- For Payer swaps, SIMM is always the highest IM.

- For Receiver swaps, SIMM is also clearly higher across all maturities.

- At CME and LCH, IM tends to increase with maturity across both payers and receivers. As we already commented, this is not necessarily the case under SIMM – 10 year IM requirements see a dip.

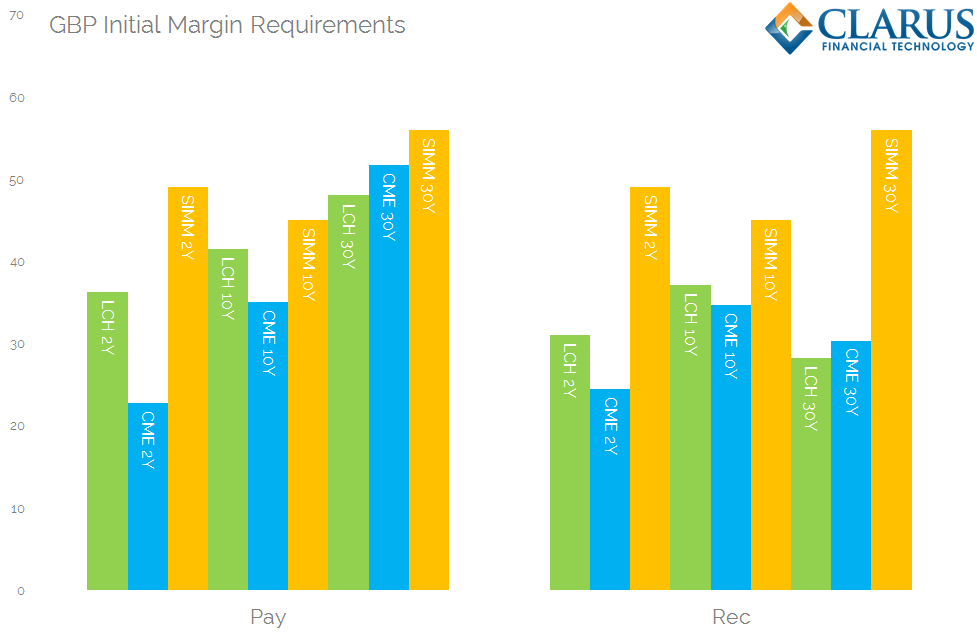

GBP Interest Rate Swaps

It is worth looking at a third “normal” volatility currency as well – GBP IRS:

Showing;

- SIMM is again the highest Initial Margin requirement across every scenario.

- A very large variation for 30 year Receivers, where SIMM is double the margin requirement at LCH.

As we can see, even excluding portfolio effects (i.e. the relative mix of currencies), standalone swaps exhibit considerable differences to SIMM. And these differences are intrinsically linked to the currency of the underlying.

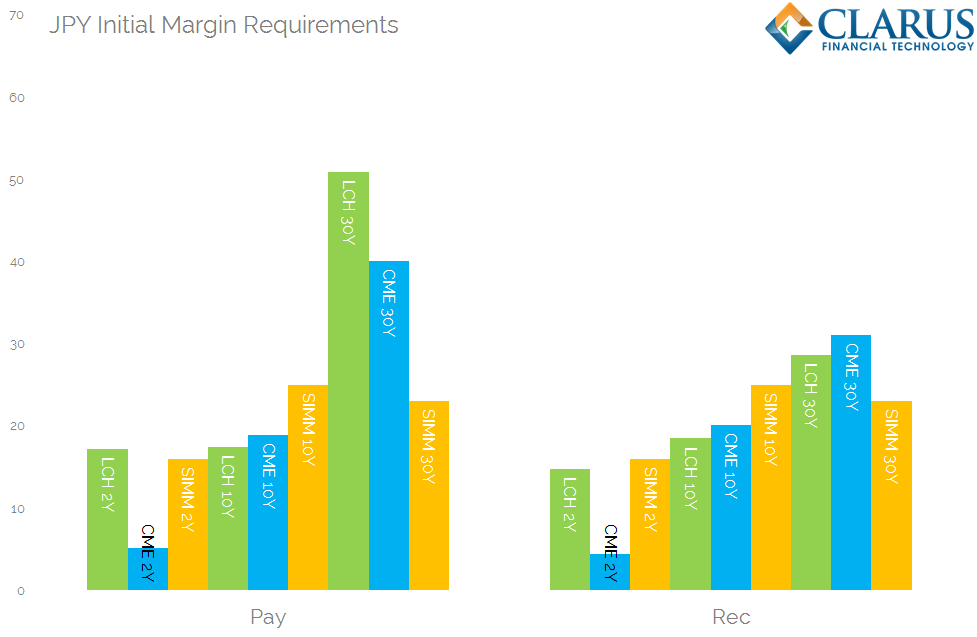

JPY Interest Rate Swaps

Let’s shift attention to the only low volatility currency in SIMM – JPY IRS:

- 30 year payer swaps aside, I guess it is unsurprising that we do not see a large spread in results.

- Something unusual for SIMM is that 10y IM is higher than 2y or 30y – which is the opposite to what we see in normal volatility currencies and not something replicated in the CCP models.

- SIMM is just 45% of the IM requirement of a Pay Fixed LCH 30 year JPY IRS. This difference could get even larger when liquidity add-ons or client multipliers are taken into account. These add-ons are not (yet) accounted for under SIMM.

- I find it surprising that SIMM can be lower for both Payers and Receivers in 30 year swaps. Particularly as only JPY is deemed a low volatility currency at the moment.

And Finally

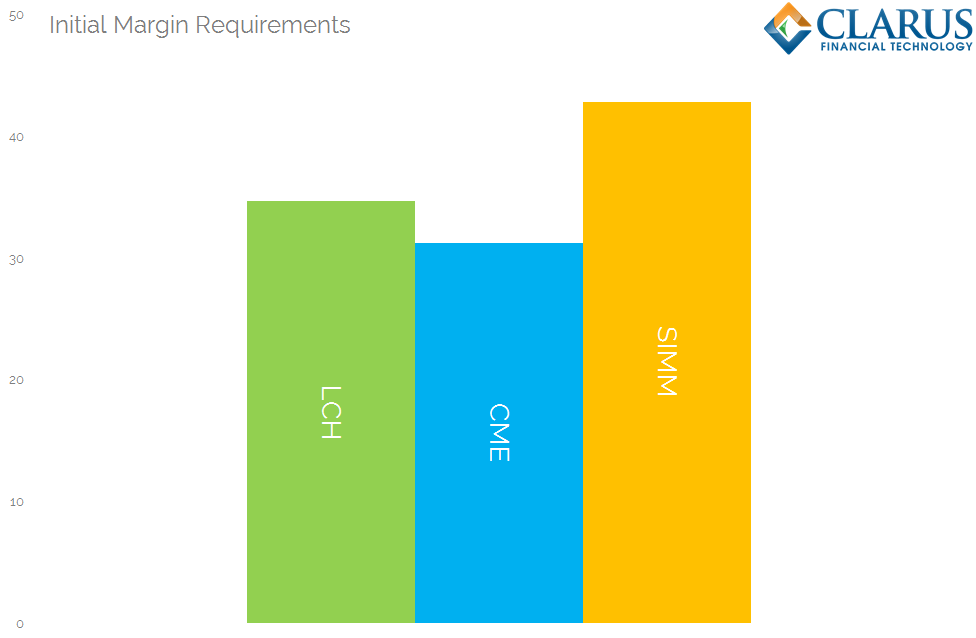

Here is a a simple take-away from this week’s blog: SIMM is similar to a parametric VaR model, designed to be a one-size fits all for a range of end-users and dealers. So it has to make sense on a consolidated basis. This blog allows us to measure IM on a consolidated basis because we have used a maturity-agnostic measure and expressed IM as basis points of risk. This means that we can take a simple average across 2y, 10y, 30y Payer and Receiver swaps across all four currencies. The analysis is below:

Showing;

- On average across our sample, CME demands the lowest amount of IM at 31 basis points.

- LCH demands 35 basis points.

- SIMM demands the largest IM overall, at 43bp.

- SIMM is therefore 37% higher than CME IM and 24% higher than LCH IM.

- These measures are for a House account across USD, EUR, GBP and JPY.

- They exclude any charges that clients may face from IM multipliers.

Please remember that CCPs employ multi-lateral netting, where-as SIMM must be applied per counterparty. This lack of multi-lateral netting in the bilateral space typically means that a real portfolio will have much larger IM in bilateral space than when it is cleared.

These consolidated differences between the 3 models will vary depending on the currency composition and maturity of a portfolio, therefore please take them as a broad illustration only. It will be an interesting blog in the future to estimate these consolidated amounts more accurately, based upon trading volumes in Cleared and Uncleared markets.

In Summary

- We compare IM requirements across LCH, CME and bilaterally under ISDA SIMM™.

- The variations between the models (for a standalone swap) can be significant.

- These variations vary from currency to currency and from maturity to maturity.

- Overall, we can say that ISDA SIMM demands a larger amount of IM than either CCP.

- Given portfolio effects and differing amounts of netting, it would be unwise to take this as gospel.

- It is prudent to perform this analysis per counterparty (pre-trade) using a sophisticated margin analysis tool such as CHARM.

- Contact us if you need more details.