In my Dec 2015 blog, CCP Basis Spreads:What Next, I opined that we would see CCP Basis Spreads becoming significant in non-USD Interest Rate Swaps and I subsequently covered the LCH-JSCC Basis in JPY Swaps.

Today I will look at the LCH-EUREX Basis in EUR Swaps.

Broker Quotes

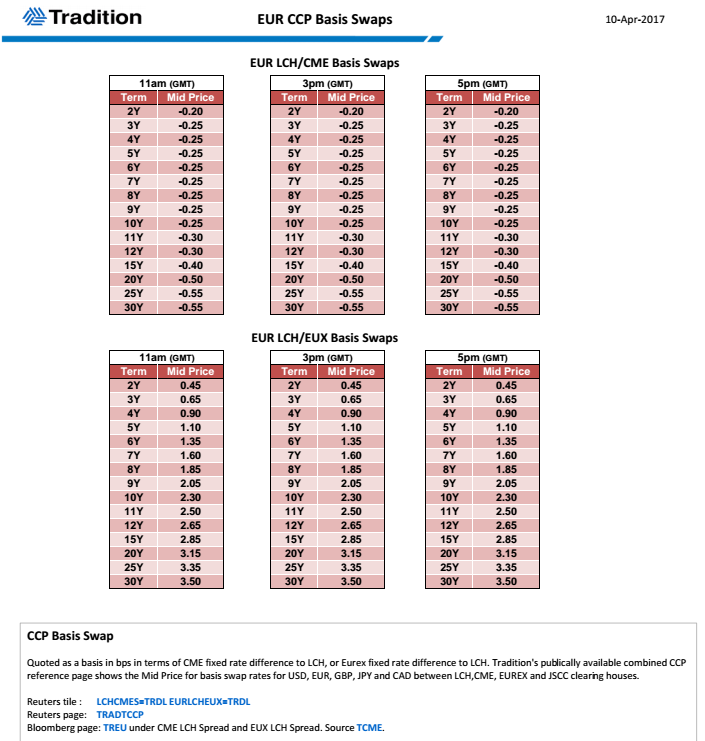

Lets start with Tradition’s EUR CCP Basis Swaps prices for April 10, 2017.

Showing:

- LCH/CME and LCH/EUX Basis Swaps

- LCH/CME are in the range -0.20bps to -0.55bps from 2Y to 30Y

- LCH/EUX are in the range +0.45bps to +3.50bps

- LCH/EUX 10Y is +2.30 bps

- Given that EUR IRS 10Y (LCH) mid is 0.711%, this is significant

- Meaning that 10Y (EUX) mid would be 0.734%

- While 5Y (LCH) mid is 0.13%, making 5Y (EUX) mid 0.141%

Very interesting and significant price differences indeed.

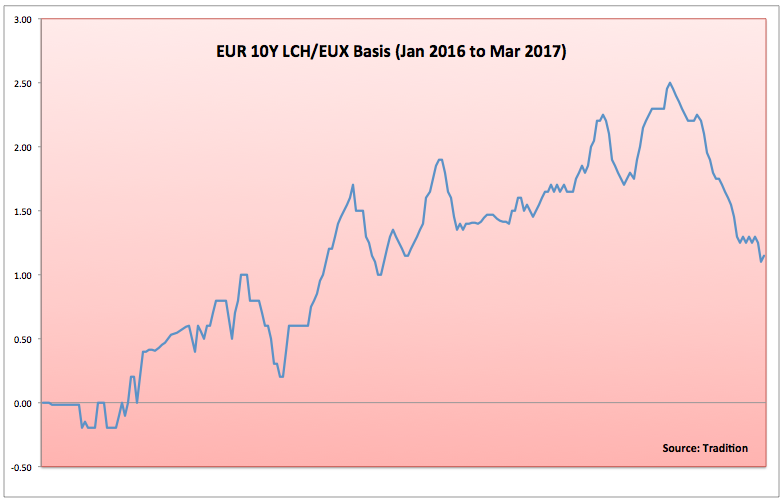

Lets look at how variable the basis has been.

Time Series History

Using Tradition data for the past 15 months, we can chart the EUR 10Y LCH/EUX Basis.

Showing that:

- Before 21 Apr 2016 the basis was flat or negative 0.2 bps

- Increasing to +1 bps by 20 Jul 2016

- Back down to +0.2bps by 26 Sep 2016

- Up again to +1.7 bps on 18 Nov 2016

- A classic roller coaster ride

- Reaching +2bps on 10 Feb 2017

- A high of +2.5 bps on 20 Feb 2017

- Back down to +1.1 bps on 22 Mar 2017

- (And not shown on the chart, up again to +2.3 bps on 10 Apr 2017

Volatile to say the least.

CCP Switch Data

At this point it would be interesting to see how much CCP Switch trading activity there is.

Unfortunately, unlike the US, where this data is made public by SEFs, there is no such public data in Europe, but chatting to IDBs we do hear that trades are happening and hence the volatility in the basis.

So let’s turn our attention to whether volumes are picking up at Eurex.

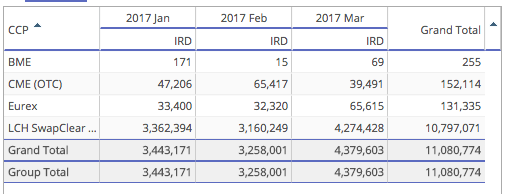

EUR Cleared Swaps Volume

First monthly volume for all CCPs with EUR IRS (so excluding Eonia, Fra, Basis).

Showing:

- Eurex increasing from €32 billion to €66 billion in March

- Eurex higher in March than CME

- BME with €69 million

- LCH SwapClear massively higher than all at €4.27 trillion in March.

So not much in the way of significantly higher volumes at Eurex.

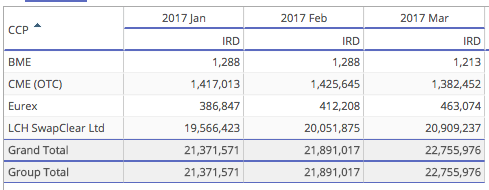

Next Outstanding notional.

Showing:

- Eurex at €463 billion end March

- Less than the €1.4 trillion at CME

- LCH SwapClear with €21 trillion

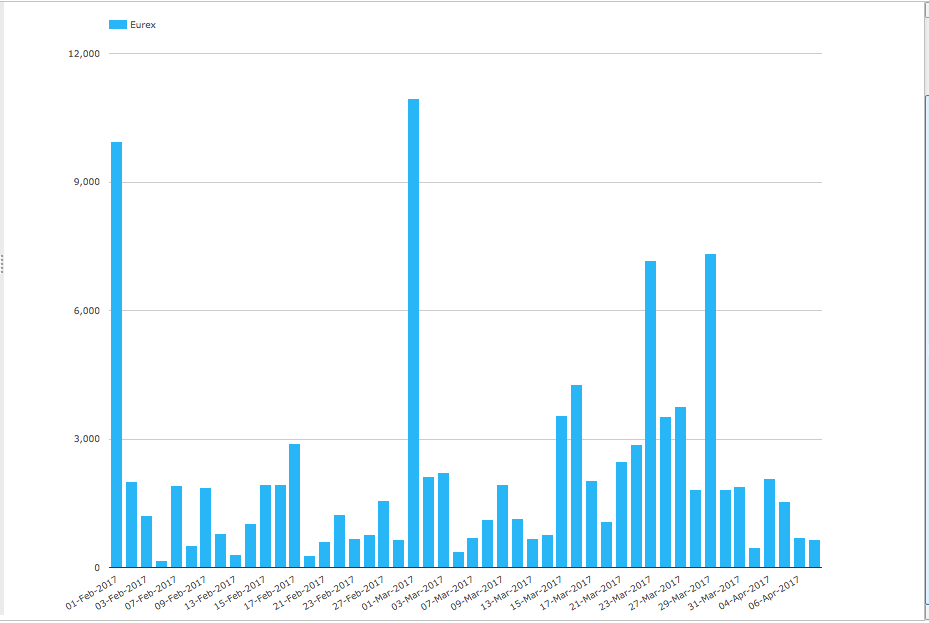

And next daily volumes at Eurex from 1 Feb to 7 Apr 2017.

Showing:

- Two days with €10 billion (1-Feb and 1-Mar)

- Two days with > €7 billion (23-Feb and 29-Mar)

- Possibly these are back-loading volume

- Four days with > € 3 billion

- All other days below this, many < € 2 billion

- Some evidence of more days in March with higher volume than days in Feb

It will be interesting to see whether this higher trend at Eurex continues in April.

By contrast the LCH SwapClear Daily Average over this period is €167 billion, so a massive difference.

Final Thoughts

While daily volume at Eurex remains low, the outstanding notional is increasing (€463 billion end March) and one can imagine that as Clearing members have been actively managing their USD IRS CME/LCH Basis, they are now doing the same with LCH/EUX Basis in EUR.

Further the data suggests we might be poised for an uptick at Eurex and more volatility in the basis.

For lots of reasons: the Deutsche Bourse and LSE merger is dead, recent press on KfW choosing to clear on Eurex, the Brexit clock ticking, European politicians advocating EUR Clearing should be in the Euro Zone, Mandatory clearing for Clients, Uncleared Margin rules impact on Clearing, I could go on ….

A plethora of reasons.

A case of now or never?

Perhaps, but liquidity is notoriously hard to move.

I know Eurex did it in the 90’s with the EUR Bond Future from Liffe, so there is a precedent.

But the diversification benefit of all currencies together at LCH is a strong incentive.

Only time will tell what happens this time.

We will be keeping an eye on the data.

Both volumes and the basis.