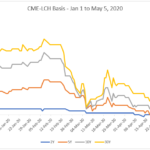

CME-LCH Basis Spreads Turn Negative

We last looked at CME-LCH Basis in August 2019 in CME-LCH Basis Narrows to Four Year Low and as there has been significant volatility in the last few months, high time we looked at this again. Background For Swaps that are economically the same, it is non-intuitive that the fixed rate should be different depending […]

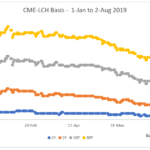

CME-LCH Basis narrows to four year low

Our recent blog, CCP Basis – The Cost of Clearing Fragmentation, proved very popular and while this was published on July 30, 2019, it was actually written a few weeks earlier. As is often the case with these things, there have been major new market developments in the CME-LCH Basis, meaning we need to do […]

CCP Basis – The Cost of Clearing Fragmentation

Staff Working Paper No. 800 from the Bank of England was published in May 2019. Titled “The Cost of Clearing Fragmentation”, the paper lays out a quantitative process to model the level of CCP basis. We’ll give you a layman’s guide to the paper here and show how our own data from CCPView can be […]

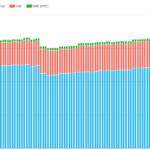

CCP Basis and Volume in Major Currencies

Almost a year has passed since we last looked in detail at CCP Basis, which just goes to show how normal and accepted this has become in the market. Since the shock emergence of the CME-LCH Basis Spread in June 2014, we have seen regular trading of CME-LCH Switch trades to manage the CCP Basis […]

CME-LCH Basis For Dummies

We occasionally still get asked about the price differential between CME and LCH swaps. I typically refer folks to our online articles that have explained the phenomenon. Since 2014, we have written 18 separate pieces on the CME-LCH basis spread. A few of the ones that begin to quantify it include: May 20, 2015 – […]

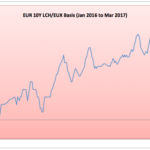

LCH-Eurex Basis in EUR IR Swaps

In my Dec 2015 blog, CCP Basis Spreads:What Next, I opined that we would see CCP Basis Spreads becoming significant in non-USD Interest Rate Swaps and I subsequently covered the LCH-JSCC Basis in JPY Swaps. Today I will look at the LCH-EUREX Basis in EUR Swaps. Broker Quotes Lets start with Tradition’s EUR CCP Basis Swaps prices […]

LCH-JSCC Basis: An Update

My blog last week on LCH-JSCC Basis in JPY Swaps has been massively popular and now that we have another week’s data under our belt, it is worth an update. Indicative CCP Basis Quotes Let start with Tradition’s page as of Friday April 22, 2016. Showing, Yen IRS quotes at JSCC, Yen IRS quotes at LCH, LCH/JSCC Basis and 6v3 […]

LCH-JSCC Basis in JPY Swaps

Last week a number of our readers alerted us to the sudden formation of a Basis in Yen Swaps between LCH and JSCC, which is interesting to say the least. So lets look at what the data shows. Indicative CCP Basis Quotes Tradition kindly sent us a screenshot of their new page. Showing, Yen IRS dealer quotes at JSCC, […]

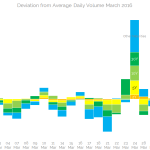

CME Compression and CCP Basis

The CME Compression run in March coincided with a peak in daily volumes for 30 year USD Swaps. Amongst falling Average Daily Volumes in USD Swaps over March as a whole, this extra 30 year activity was particularly noticeable. We also saw a peak in 30 year CCP Basis trading a day before the CME Compression run. We wonder […]

How to identify the CCP of trades from the SDR data

We use Linear Regression on price time-series to identify discontinuities in price These discontinuities represent jumps in price We use these jumps to identify which USD IRS trades are cleared at CME This allows us to extract yet further information from the publicly reported data The methodology is dynamic, and therefore is suitable across a range of products and maturities Forecasting Swap Prices […]