Given the recent activity in CME-LCH Basis Spreads (see November review or Spreads Blow Out), we often get asked what further developments we see happening and specifically whether a basis will manifest between non-USD currencies and between other Clearing Houses. This article will look at both of these questions.

Indicative CCP Basis Quotes

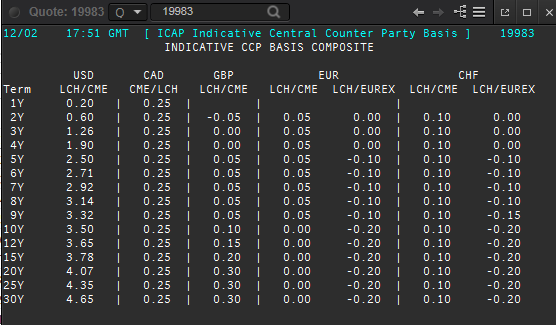

Lets start with a screenshot of the ICAP 19983 page on Reuters from 2 Dec 2015.

This is titled Indicative CCP Basis Composite and shows:

- CAD, GBP, EUR, CHF Basis spreads for LCH/CME

- EUR & CHF Basis spreads for LCH/Eurex

- Each of these are small, in the range -0.20 to +0.30 basis points

- (USD LCH/CME we have covered before)

Interesting and definitely worth exploring in more detail.

CME-LCH Basis in USD

But first a re-cap of the rationale behind the large basis we see in USD.

Clients at CME have a preference to pay fixed on swaps and Swap Dealers taking the other side (receive fixed) need to hedge by paying fix and historically had a preference to do so on LCH. As client business at CME increased significantly in 2014 and the first part of 2015, this imbalance in a Swap Dealers house portfolios at CME and LCH became very large and the margin cost prohibitive in terms both of funding cost and regulatory cost. Resulting in Swap Dealers adjusting their prices to make it more expensive to pay fixed at CME.

We can show this quantitatively by using CHARM to calculate Initial Margin for par swaps on major tenors.

Showing that:

- Paying Fixed on 30Y for DV01 $50k (@ $25m notional) at CME has an IM requirement of $1.8m

- A Swap Dealer would Receive Fixed on this Swap and have a CME IM requirement of $1.6m

- If the Dealer entered into a hedge at CME to Pay Fixed, the net DV01 of these trades would be zero

- So the Dealer would have no IM to pay at CME

- However if the Pay Fixed Hedge was done at LCH, an additional $2.7m of IM would be required

- In total the Dealer would need to fund two IMs, $1.6m and $2.7m, so $4.3m

- This funding cost and resulting default fund contribution is sizeable

- It is a stretch to say it is 4.65 bps (as the ICAP page shows)

- But it is the key contributor to that figure

In reality, a Swap Dealer should not be looking at the stand-alone IM of each trade, but the incremental change in IM of the new trades on their portfolio. As the imbalance grows between the Dealers House Account being massively Received Fixed USD at CME and massively Pay Fixed USD at LCH, another effect comes into play. The fact that one or both accounts are now above a liquidity threshold and so incur an additional IM charge; further increasing the IM and its cost. The net result being a further upward pressure on the basis spread.

Using CHARM, we can model both the portfolio impact and the liquidity add-on, both at time zero and over the life of the trade. However this recap is in danger of becoming the whole article, so I will stop there (contact us if you have further interest in this topic).

Except to note that given in November we saw $75 billion of CME-LCH Switch trade volume, there is clearly a two way market; meaning that not all Swap Dealers are the same way on CME and LCH or that there is a significant difference in opinion on what the true Basis Spread should be.

CME-LCH Basis in Non-USD Currencies

Back to the CAD, GBP, EUR & CHF currencies shown on the ICAP page.

- CAD shows 0.25 bps for all tenors

- GBP shows -0.05 bps at 2Y, then 0, 0.05 bps 5Y to 9y, 0.10 bps 10Y and 0.30 bps at 30Y

- EUR is 0.05 bps below 10Y and zero at 10Y and above

- CHF is 0.10 bps for all tenors

Lets corroborate by looking at what Tradition show on their Bloomberg page.

While this is from 23 Nov, given the Thanksgiving holiday in-between, still comparable to 2 Dec:

- CAD is 0.25 bps at 2, 5, 10, 30Y

- GBP is -0.05 bps at 2Y, 0.08 bps at 10Y, 0.25 bps at 30Y

- EUR is 0 at 2Y, 5Y and -0.05 bps at 10Y and 30Y

So generally the Tradition and ICAP pages are consistent, with small differences of 0.05bps on some tenors.

Cleared Volumes

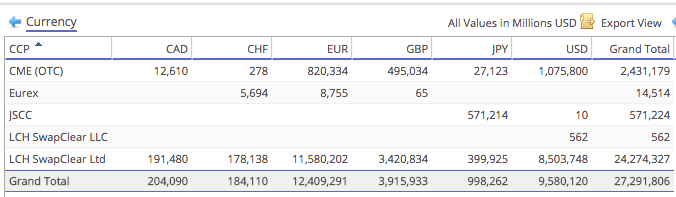

Lets now look at Cleared Volumes at CME and LCH for these currencies.

Using CCPView, we first produce a table of November 2015 volume in USD millions.

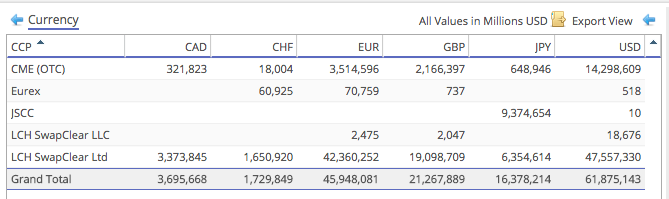

Then Outstanding Notional as at Nov 30, 2015.

Showing that:

- CAD volume in Nov is $12.6b at CME and $191b at LCH

- CAD outstanding notional on Nov 30 is $322b at CME and $3,374b at LCH

- Now we do not know if any CAD client business on CME is hedged by Dealers at LCH

- But given the CME amounts are relatively small compared to LCH, it is likely not significant for Dealers

- A 0.25 bps spread is small, but the fact it exists suggests some hedging at LCH

- CHF is even lower at CME and the spread is at 0.10 bps, so similar arguments apply

- For both CAD & CHF, the fact the basis is the same across all tenors is also interesting

- Implying little or no active pricing of basis in these currencies

- EUR and GBP are quite different

- There is a term structure to the basis spread

- And both are significant at CME, 8% and 10% of the Combined LCH and CME Outstanding Notional

- But the fact that the basis is small or negative, implies different supply and demand dynamics

- Meaning their is none or less bias from firms to pay fixed in these currencies at CME

- Possibly only for GBP in long tenors

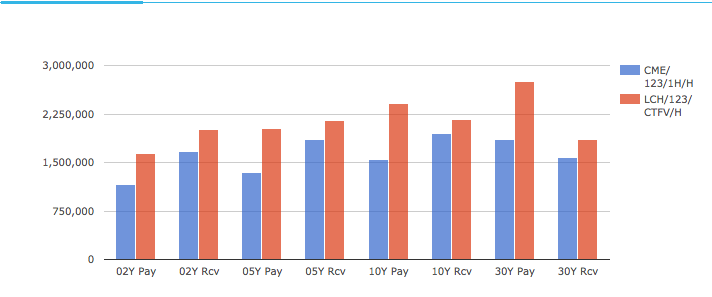

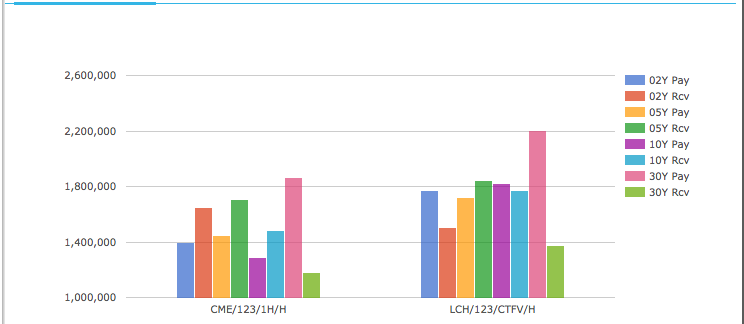

Interestingly for GBP swaps at 30Y there is significant asymmetry between pay and rec at both CME & LCH.

Compare the pink bars for 30Y Pay with the adjacent green bars for 30Y Rcv.

In summary EUR and GBP have the potential for the CME-LCH Basis to be volatile going-forward.

Basis between other CCPs – LCH/Eurex

Lets now look at other CCPs.

The ICAP page quotes LCH/Eurex spreads in EUR & CHF.

First the global cleared volumes as before, this time including JPY; first volumes in November.

Then Outstanding Notional at November 30.

Showing that:

- CHF volume in Nov is $5.7b at Eurex and $178b at LCH

- CHF outstanding notional is $61b at Eurex and $1,651b at LCH

- The ICAP basis quotes show -0.10 bps for 8Y and below, -0.15 bps for 9Y and -0.20 bps 10Y and above

- Meaning it is more attractive to pay fixed at Eurex, albeit a spread comparable to the bid-offer

- Not sure why that would be

- Perhaps due to the fact that Eurex have waived clearing fees for a period?

- But as the volume on Eurex is currently low, we know that few trades are being done

- So we should not draw too much from the spread prices

- EUR volume at Eurex is comparatively even smaller than CHF compared to LCH

- And the ICAP basis is similar to that in CHF, from -0.10 bps to -0.20 bps

- So again not much to say

We will need to wait for EU Mandatory Clearing (end 2016 for Category 2 firms) to see what happens to Eurex volumes and the LCH/Eurex basis.

It now appears trickier for Eurex to gain traction given that Swap Dealers will be reluctant to hedge client business on Eurex with dealer hedges at LCH, for fear of losses arising from a similar scenario to CME-LCH. Consequently supply and demand (pay vs rec) will need to be better balanced and the benefits of portfolio margining with Bund Futures more significant than hitherto seen in the US with CME Futures.

Basis between LCH/JSCC?

Lets now look at JPY and JSCC volumes:

- JPY volume in Nov is $571b at JSCC vs $400b at LCH

- JPY outstanding notional at Nov 30, is $9.4 trillion vs $6.4 trillion at LCH

- Both larger than LCH

However we don’t have an ICAP or Tradition basis quote page.

So where else can we look?

Luckily if you follow our Japan ETP blogs, you will know that there is now post-trade disclosure of price and size of 5Y, 7Y, 10Y Swaps Cleared at JSCC.

And if you know our SDRView product, you will know that JPY Swap trades executed by US persons are publicly disclosed, which from the above volumes we know are dominantly LCH.

So we can look for evidence of a LCH/JSCC Basis in actual transactions.

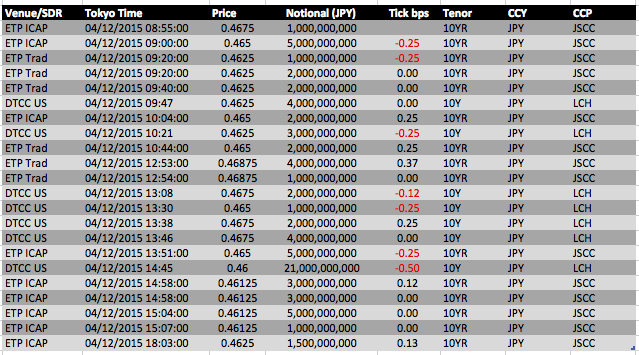

Lets try for Friday 4-Dec and 10Y JPY Swaps.

Unfortunately there are only 7 trades on the US DTCC repository and 15 on ETPs. Even so lets create a table and sort by time.

Showing:

- Either ETP ICAP or ETP Tradition (which are JSCC as CCP)

- Or DTCC US as the SDR (assumed to be LCH CCP)

- Sorted by Tokyo time

- Price, Notional and Tick bps (change from previous trade price)

- Tick bps is usually 0, 0.12 or 0.25 and once 0.37

Assuming that the bid-offer is 0.25bps, the prices do not show any evidence of a basis.

We would want to repeat for more days, more tenors and more volume to be sure.

Possibly JSCC participants are operating in a domestic liquidity pool and LCH participants in a separate foreign liquidity pool, both of significant size and on the same economic instrument.

However Client Clearing of JPY IRS is still in its infancy in Japan and it is possible that when these volumes build up, we will see new pressures on supply and demand, an increase in activity between the JSCC and LCH and a LCH/JSCC Basis Spread develop.

Summary

We are starting to see evidence of non-USD CCP Basis.

Both ICAP and Tradition have indicative quote pages.

Currently the quotes range from -0.20 bps to +0.30 bps.

So are not significant.

There is a possibility of these becoming significant.

In EUR, GBP, JPY, CAD, CHF?

And including other CCPs e.g. LCH/Eurex, LCH/JSCC.

But not until Client Clearing is mandatory and significant in Europe and Japan.

Or possibly not even then.

Only time will tell.