- We run the SSTI and LIS thresholds over US SDR data.

- We anticipate that over 80% of EUR swaps will not be subject to pre-trade transparency.

- Post-trade transparency will not be much better.

- 75% of the risk traded will remain dark for up to four weeks.

- We are intrigued to see what the APAs will publish on 3rd January 2018.

This week’s MIFID II news

This week we have seen the FCA approve a number of APAs. As we’ve written about in the past, we are intrigued to see what trade details these new venues will actually publish in January 2018. Will the data be anywhere near as useful (or as timely) as the data we regularly interrogate in the US SDRs? In today’s blog, I will expand upon the recalibration work that we did last month.

Instead of looking at what the levels should be, I will simply re-state the US SDR data with the current SSTI and LIS filters applied. What would we see for EUR swaps? Will it be as useful (or as timely) as the SDR data?

MIFID II “Transparency”?

As a brief reminder, Transparency Requirements depend whether a trade is:

- Liquid. Is the instrument deemed to be “liquid”? If not, then transaction data can be subject to a publication delay (defined by the National Competent Authority (NCA), between 2 days and four weeks).

- LIS. Is the trade deemed “Large in Scale”? If so, then pre-trade transparency of an order is not as great, and post-trade disclosure can be subject to the NCA’s publication delay.

- SSTI. What is the “Size Specific To Instrument” threshold? If a trade is above the SSTI, then the pre-trade transparency of responses to an RFQ is reduced and post-trade disclosures are subject to the NCA’s prescribed publication delay.

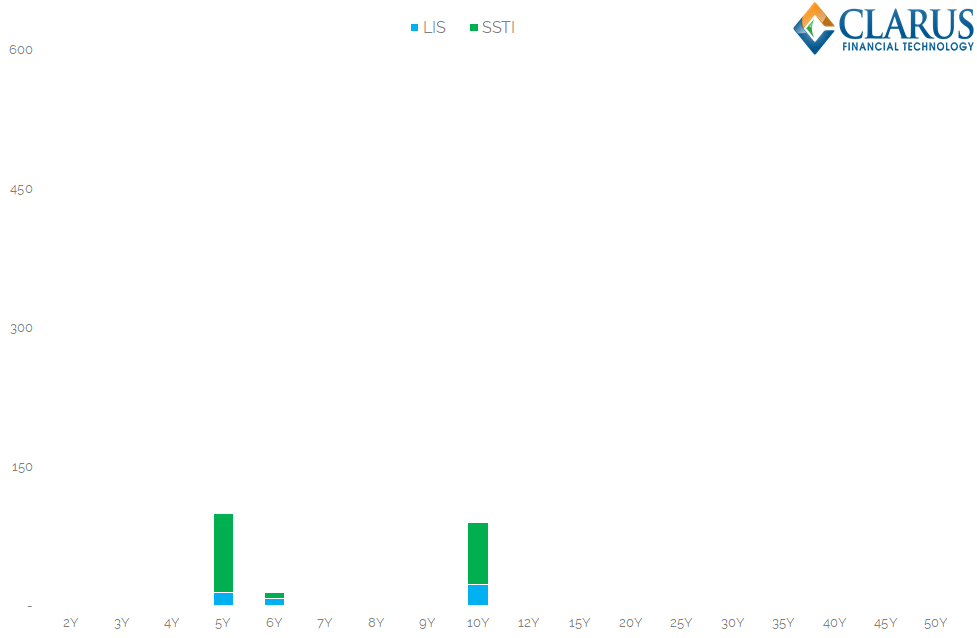

Here are the ESMA calibrated limits for Swaps:

Showing that the instruments deemed to be liquid are;

- EUR IRS maturing in 4 to 5 years

- EUR IRS maturing in 5 to 6 years

- EUR IRS maturing in 9 to 10 years

- USD IRS maturing in 5 to 6 years

In a nutshell, these limits have been calibrated such that there will be no pre-trade transparency for EUR trades above €20m in size. There will also be sizeable delays in post-trade transparency for trades above ~€100m (depending on maturity).

I will now re-state 2016 SDR data to show what US transparency would look like with these limits in place.

Restating 2016 SDR Data

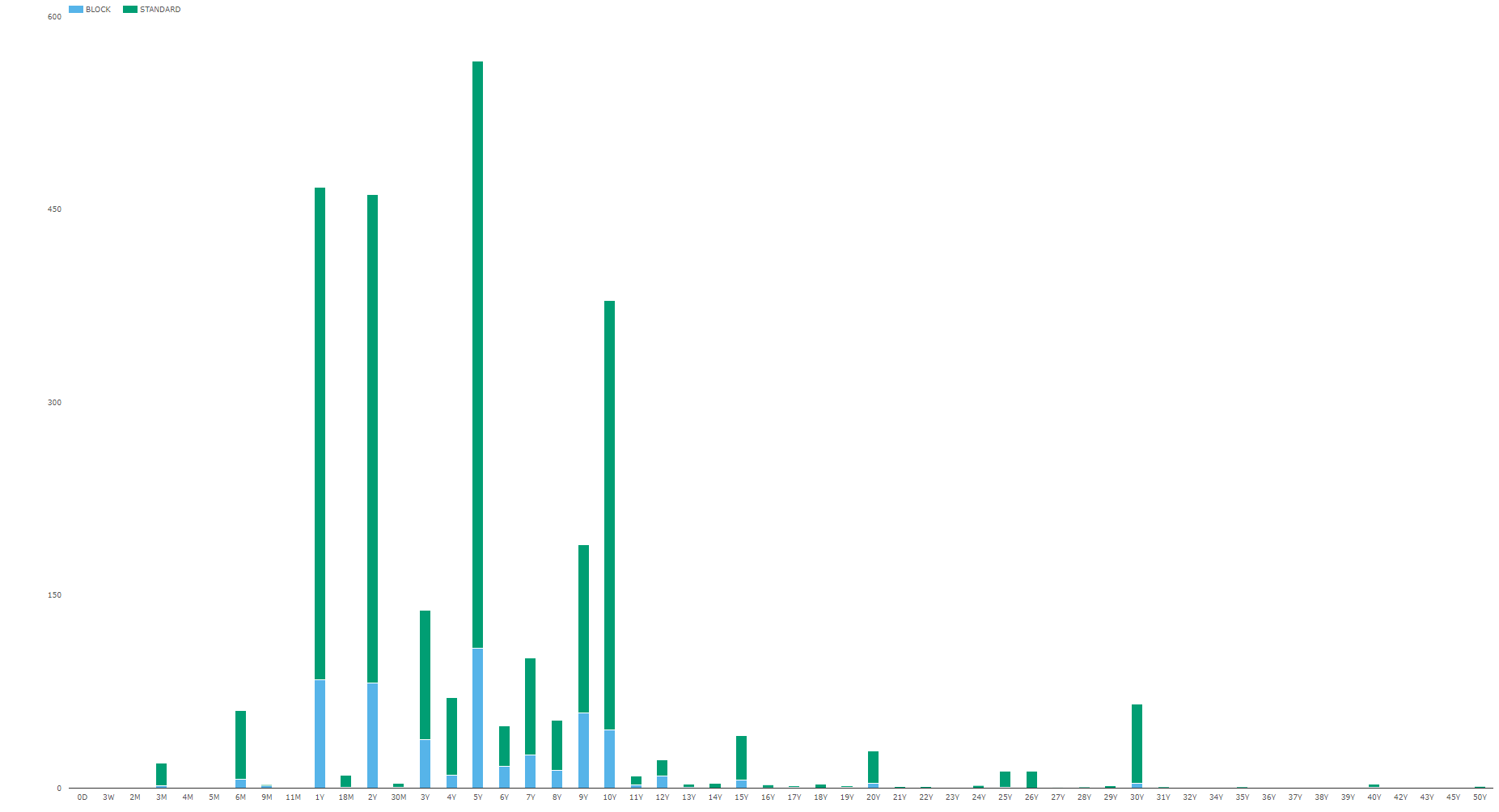

These limits were calibrated versus trading data for the second half of 2016 (the same sample period as used by ESMA to calibrate the thresholds). From SDRView Pro, we can see the notional traded of EUR swaps within 15 minutes of the trade being transacted. The data for EUR swaps traded during the second half of 2016 is shown below:

Showing;

- The bars in green show the notionals reported below the block threshold in the US. This means that these trades were reported shortly after they were transacted. These trades tend to be reported within two minutes to the public feed.

- The bars in blue are the trades with notionals above the “block” threshold. The actual size of these trades is above their reported notional. They are reported within 15 minutes of execution.

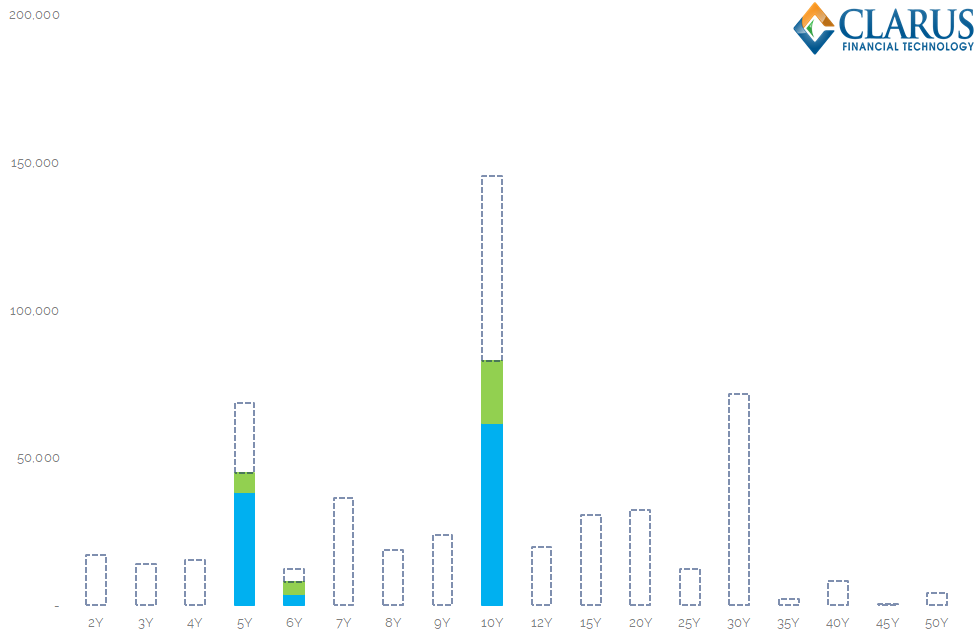

Let’s compare this to what MIFID II post-trade transparency data will look like within 15 minutes of execution. Using the same EUR swap population, the above chart is transformed to:

Showing;

- A small subset of the total trade population, at just 27% of total notional.

- This is clearly disappointing, but it is also higher than I anticipated! It is an interesting visual trick that the chart makes it look a lot less than 27%.

- Recall from the table above that only swaps maturing in 3 maturity buckets (4-5y, 5-6y and 9-10y) are deemed “liquid” for purposes of Transparency in EUR swaps. On the chart, these buckets are segregated using the longer maturity only.

- In 5y swaps, a total of €151bn traded in the six months of 2016. Under MIFID II Transparency thresholds, €85bn would be below the Size Specific to the Traded Instrument threshold, and hence subject to immediate post-trade transparency. An additional €14bn was also below the Large in Scale Threshold.

- The remaining €52bn of 5 year EUR swaps (i.e. over a third of the notional) was above the Large in Scale threshold. These swaps will be subject to a reporting delay of between two days and four weeks!

- It is a similar story in 10 year EUR swaps. €156bn total was traded, €66bn was below the SSTI and an additional €23bn below the LIS thresholds. This means that the remaining €67bn of EUR swaps will remain “dark” for up to four weeks.

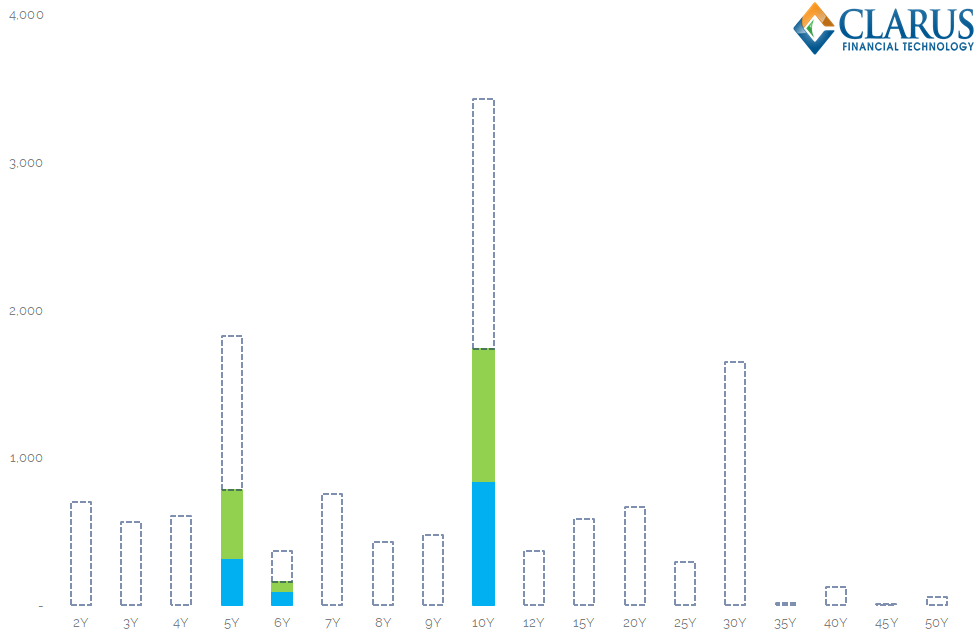

75% of Risk traded will remain dark

The chart below shows what the MIFID II data will look like versus the SDR data in DV01 terms:

Showing;

- DV01 traded under the SSTI limit in blue, DV01 traded below the LIS limit in green and all trades that will remain dark for up to four weeks in dotted bars.

- On a DV01 measure, only 25% of the risk will have timely post-trade transparency applied. Trading is very much concentrated in three tenors – 5y, 10y and 30y. This highlights that 30 year swaps should have been deemed liquid.

80% of trades will not have any Pre-Trade Price Transparency

Remember that MIFID II is trying to improve price transparency as well as volume transparency. Providing post-trade data on swaps that trade in just 3 tenors is not enough to build an interest rate pricing curve. Maybe the price-data can be derived from pre-trade price transparency then?

Think again. The thresholds for SSTI and LIS are even lower for pre-trade transparency (which of course makes sense to avoid information leakage and front-running of potential market-moving trades). For pre-trade transparency:

- I am really driving this point home by showing another similar chart!

- Eighty-percent of all EUR swaps traded will not be subject to pre-trade transparency. They will remain dark.

- Pre-trade transparency will only give us price data for 3 points on our interest rate swap curve. This is not enough to calibrate any meaningful pricing data.

- 30 year swaps traded 30 times more often than 6 year swaps, and traded 6 times more DV01. 30 year swaps were not deemed liquid in the calibration process. This highlights how poor the calibration data was.

In Summary

- ESMA used a poor data set to calibrate pre- and post-trade transitional transparency thresholds.

- This means that 75% of risk traded in EUR swaps will remain dark for up to four weeks.

- 80% of EUR trades will have no pre-trade transparency.

- There will not be any meaningful price transparency either pre- or post-trade to build an Interest Rate Swap curve.

- We believe that the LIS and SSTI thresholds, along with the liquid designations, should be re-calibrated using the freely available SDR data.