- ESMA have published Transitional Transparency Calculations for a number of asset classes.

- These calculations define which asset classes and instruments are deemed liquid for the purposes of making trade data public as of 3rd January 2018.

- Anything deemed “illiquid” will likely have a two-day lag applied to the trade record being made publicly available.

- The transitional calculations also include the trade sizes at which different levels of pre- and post-trade information is made available.

- These calculations are deemed “transitional”. We believe the next assessment will not occur until April 30th 2019.

What is MIFID II Transparency Data?

Amir covers this better than I ever could, therefore please check out his two posts on the subject below:

Why do we care?

ESMA valiantly bases things like Trading Obligations and Transparency Requirements upon actual data it collects (which is a good thing if the data is good).

Periodically, ESMA therefore need to notify the market of what this data has told them. We looked at the data behind the latest Trading Obligation Consultation Paper last month, and today we are looking at the Transparency Data. The findings from this data allow ESMA to define what information will be published per trade and made publicly available both pre-trade and post-trade for a given instrument (e.g. a 4 year EUR IRS) of a given size. It is important to note that data dissemination varies both pre- and post-trade depending on size thresholds, akin to block trade thresholds in the US.

As a 3 bullet summary, the key terms that ESMA will use their data to define are:

- Liquid. Is an instrument deemed to be “liquid”? If not, then transaction data can be subject to a two-day publication delay.

- LIS. Is a trade deemed “Large in Scale”? If so, then pre-trade transparency of an order is not as great, and post-trade disclosure can also be subject to a two-day publication delay.

- SSTI. What is the “Size Specific To Instrument” threshold? If a trade is above the SSTI, then the pre-trade transparency of responses to an RFQ is reduced and post-trade disclosures may be subject to a two-day publication delay.

Throughout writing this blog, I cannot help but think about Matt Levine’s series of blogs People Are Worried About Bond Market Liquidity. Perhaps ESMA and Mr Levine could have a chin-wag over what is “liquid”?

Where is the Data?

The point of this blog is that ESMA have now published the MIFID II TRANSITIONAL TRANSPARENCY CALCULATIONS. Whilst they state “transitional”, according to the below paragraph of the RTS2 (it is Article 13 for those interested) I do not believe that these calculations will be updated before April 30th 2019:

Given that, the data is very important. I’m surprised it didn’t get more press.

First, let’s take a look at the FAQ document. The key parts of this explanatory text are:

The data defines what is liquid, and the LIS (asset class level) and SSTI (instrument level) thresholds that will apply. Trades over these thresholds will likely have a two-day publication lag.

It is helpful that they are explicit about which instruments are illiquid as well as liquid – particularly when you take a look at the data. Yes, anything not on this list is deemed illiquid.

It is possible that a whole asset class is deemed illiquid. I want you to read this with a straight-face – ESMA have deemed that the whole of the FX asset class is illiquid:

The Data

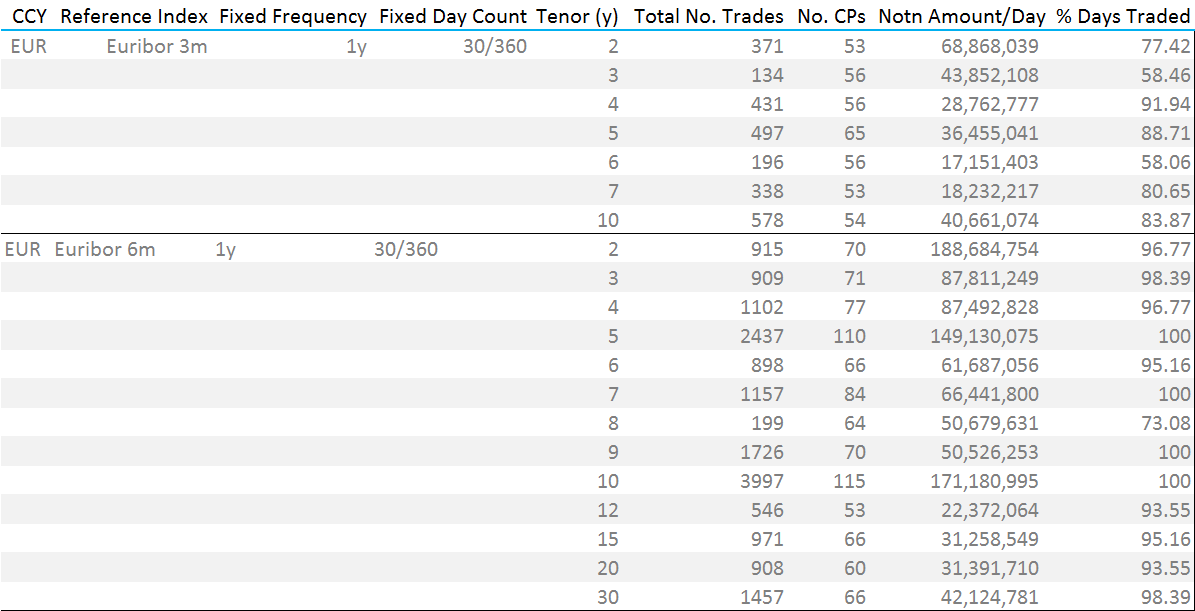

As always, we will focus on Interest Rate Derivatives. The file is a little, ahem, underwhelming for OTC products;

Showing that the instruments deemed to be liquid are;

- EUR IRS maturing in 4 to 5 years

- EUR IRS maturing in 5 to 6 years

- EUR IRS maturing in 9 to 10 years

- USD IRS maturing in 5 to 6 years

The Transitional Calculations have been performed on 2016 trading activity provided by trading venues (3rd July 2016 until 2nd January 2017). From the results, this looks like a different overall set of data to the one used in the recent consultation paper on the Trading Obligation.

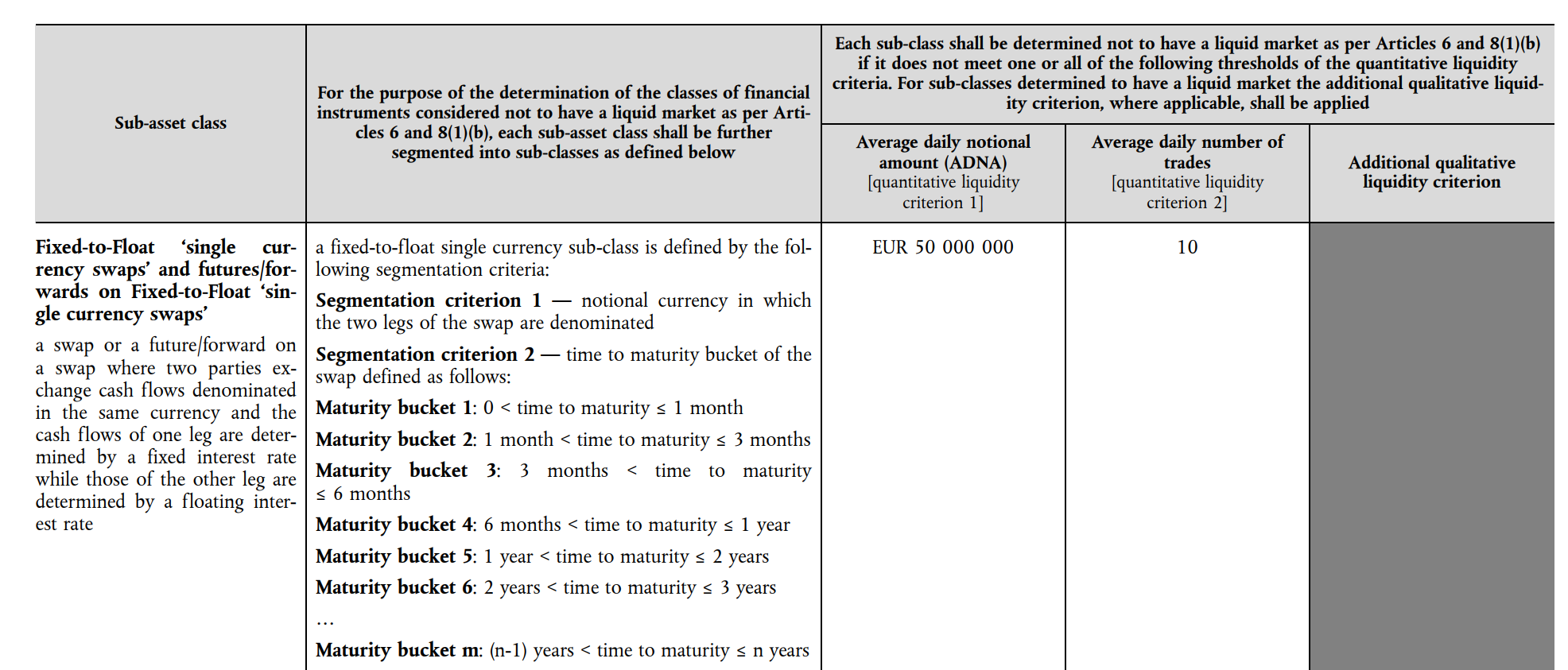

Flicking through the RTS2 details, I believe these are the criteria used to ascertain whether an instrument is liquid for the purposes of transparency:

Showing;

- For an IRS to be deemed liquid, it must have an Average Daily Volume in excess of EUR50m and/or see at least 10 trades per day.

- There are similar tests that apply for OIS, Cross Currency Swaps, Swaptions and Inflation Swaps.

- These tests of liquid/illiquid therefore appear to be different to the ones outlined in the Trading Obligation.

Therefore, whilst I expected to see all instruments that are subject to the Trading Obligation be deemed “liquid” and hence appear in the Interest Rate Derivatives file, this has not happened. As a reminder, the recent Trading Obligation consultation paper proposed the following instruments be deemed liquid:

It looks like these Transitional Transparency Calculations were therefore not only performed using a different definition of “liquid” (i.e. the one defined in the RTS2), but also possibly on different data! I guess the data-sets will converge over time given that trades subject to the Trading Obligation will have to occur on a trading venue, and hence this data will feed into the transparency calculations.

These Transitional Calculations serve well to highlight some of the complexities involved in actually implementing the technical requirements of the law.

I’m sure the irony surrounding the lack of transparency around these….transparency calculations is not lost on our readers. I sense that the lawyers in Paris and Brussels have a good sense of irony too….

Stating the Blindingly Obvious

People should be really really really bl*@#dy worried about European bond market liquidity if there are only 4 instruments that trade in more than €50m per day. It is simply not possible that the only instruments trading above this size are 4y to 10y EUR IRS in Interest Rate Derivatives. It suggests that ESMA are using a very narrow view of the tradeable universe (i.e. data from platforms that very few market participants actually transact across and/or a failure to reconcile TR data).

Luckily, we do have reliable sources of Interest Rate Derivatives data in both CCPView and SDRView. The Clarus API even provides Average Daily Volumes. As we said last time, liquidity is not globally constrained, therefore a regulator’s view of the market should not be so narrow as to focus only on European trade data – particularly when better quality, trade-level data is publicly available (e.g. from US, Canadian and Japanese SDRs).

We know that OIS, Cross Currency swaps, even Swaptions all trade much larger average daily volumes than €50m. I refer you to our previous analysis here, here and here for some data.

Examples

Using this latest data, let’s update Amir’s previous examples;

RFQ for a EUR IRS 5Y in 25m notional size

This is a Liquid Market, but above the SSTI, meaning that pre-trade the quotes provided to the RFQ will NOT be made public in real-time and all at the same time.

Post-trade details will be made public, including execution time-stamp, instrument code, price and size.

RFQ for a EUR IRS 13Y in 25m notional size

This is illiquid, meaning that no pre-trade quotes will be public and on trade execution only on T+2 business days will details be made public.

RFQ for a EUR IRS 5Y in 100m notional size

This is Liquid and above both LIS and SSTI threshold for pre-trade but below the post-trade thresholds.

Meaning no pre-trade quotes are made public but on trade execution the details will be made public in real-time.

RFQ for a EUR IRS 5Y in 500m notional size

This is Liquid and above the LIS or SSTI threshold for pre-trade and post-trade thresholds.

Meaning no pre-trade quotes are made public on trade execution, with details made public on T+2 business days.

In Summary

I’m going to leave you with a single statement.

- There will be no pre-trade transparency in RFQ IRS markets for trades above EUR20m.

Wow.

ESMA had to rely on voluntary data submission by European venues. I wonder how many responded?!