Today ESMA published its Final Report on Regulatory Technical Standards for MiFID II. A process that started in May 2014 with a Discussion Paper and then two Consultation Papers, is now nearing completion.

For this article I have read as many of the 577 pages as possible, to try and understand what MiFID II will mean and while there is a lot of interesting information for Equities, Bonds, Structured Finance Products, Emission Allowances and Derivatives, I will limit my scope to Transparency for Interest Rate Swaps.

Background

The Final Report deals with Draft Regulatory Technical Standards (RTS) of which there are 28 and describes the consultation feedback received, the rationale behind ESMA’s proposals and details each RTS. The report is now submitted to the European Commission, which has 3 months to decide (Dec 28, 2015) whether to endorse the technical standards.

Assuming that it does so, MiFID II will come into effect in Europe on Jan 3, 2017.

RTS 2 – Transparency requirements in respect of Derivatives

RTS 2 has requirements on transparency to ensure that investors are informed as to the true level of actual and potential transactions, irrespective of whether the transactions take place on Regulated Markets (RMs), Multi-lateral Trading facilities (MTFs), Organised Trading Facilities (OTFs), Systemic Internalisers (SIs) or outside these facilities.

This transparency is meant to establish a level playing field between trading venues so that price discovery of a particular financial instrument is not impaired by fragmentation on liquidity.

Meaning that there are both pre-trade and post trade transparency requirements.

Post-Trade transparency

Trading Venues and Investment firms trading outside venues are required to make public each transaction in as close to real-time as possible and in any case within a maximum 15 minutes of execution, which drops to 5 minutes after Jan 1, 2020.

Meaning that most trades will be made public within a few minutes of execution and the data will include:

- Execution date and time

- Publication date and time

- Venue

- Instrument type code

- Instrument identification code

- Price

- Notional

- Transaction identification code

- To be Cleared or Not

As well as Flags to signify details such as Cancel or Amend transaction or Non-Price Forming or Package transaction and many others.

Importantly a time deferral of 2 business days is available for transactions which are either:

- financial instruments for which there is not a liquid market, or

- large in scale compared to normal market size for the financial instrument, or

- above a size specific to that financial instrument trading on a venue, which would expose liquidity providers to undue risk.

We will come back to the definition and operation of each of these.

Pre-Trade transparency

Trading Venues are also required to make public the range of bid and offer prices and depth of trading interest at those prices, in accordance with the type of trading system they operate. Interestingly for RFQ markets this means making public all the quotes received in response to the RFQ and doing so at the same time. In addition RFQ or Voice trading systems are also required to make public at least indicative bid and offer prices, where interest is above a specified threshold.

Which means lots of public pre-trade price information including depth.

Importantly this requirement is waived for the following:

- Derivatives which are not subject to a trading obligation (clearing and liquid market)

- Orders that are large in scale compared to normal market size

- Orders that held in a order management facility of a trading venue pending disclosure

- Actionable indications of interest in RFQ or Voice that are above a size specific to that financial instrument, which would expose liquidity providers to undue risk.

We now need to tackle the meaning of Liquid Market, Large in Scale and Size Specific to Instrument.

Liquid Market

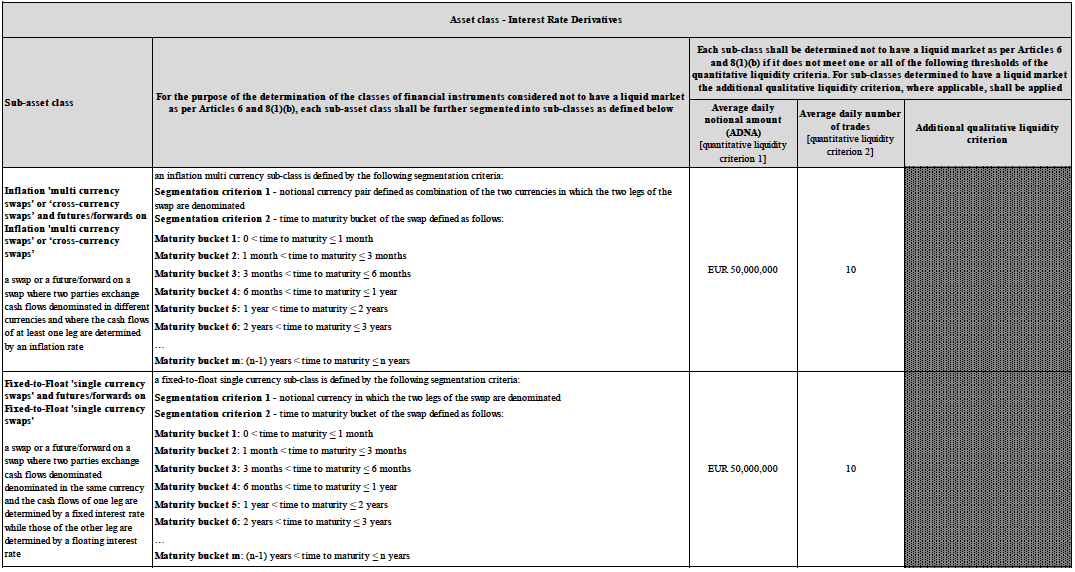

The assessment Liquid for Derivatives utilises two criteria, specified for a Sub-Asset Class and Sub-Class:

- Average Daily Notional Amount

- Average Daily Number of Trades

The table extract showing single-currency interest rate swaps in the second row is as below:

Showing that for each maturity (e.g. IRS 5Y), there needs to an Average Daily Notional of at least EUR 50 million and an Average Daily Number of Trades of at least 10.

ESMA will publish by July 3, 2016 its first assessment of which Financial Instruments are Liquid and will do so using data for the period Jul 1, 2015 to Dec 31, 2015 and this assessment will apply from Jan 3, 2017 to May 18, 2018, after which it will be periodic/yearly.

Meaning we will know by July 3, 2016 which are liquid e.g. EUR IRS 5Y and which are not e.g. EUR IRS 13Y.

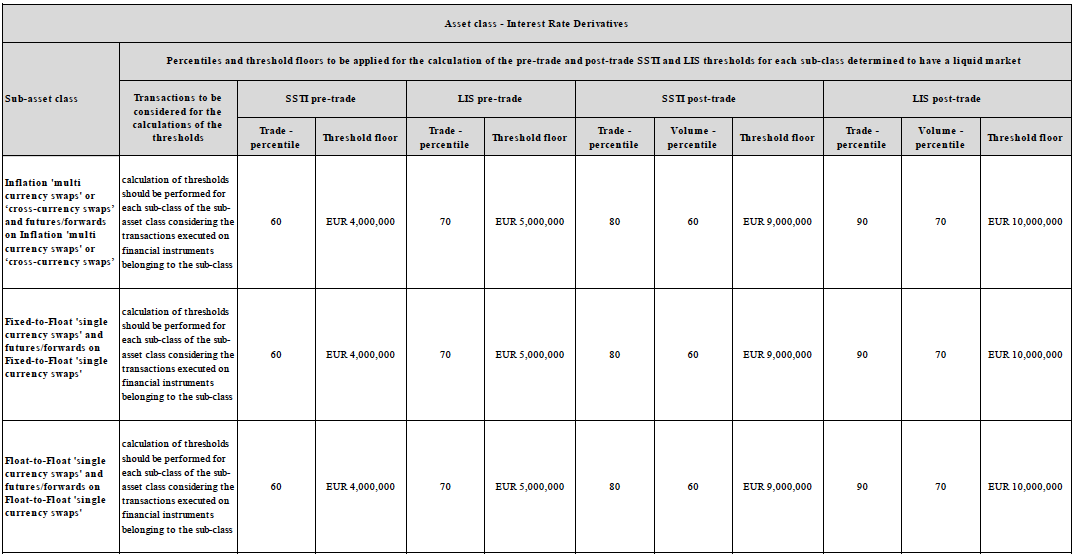

Large in Scale (LIS) and Size Specific to Instrument (SSTI)

For Pre-Trade and Post-Trade there are distinct thresholds for a Financial Instrument as to what is Large in Scale (LIS) or Size Specific to Instrument (SSTI) and these are lower for pre-trade given the greater sensitivity of this information. These are specified based on a trade or volume percentile.

The table extract for Liquid markets showing single-currency interest rate swaps in the second row is as below:

Showing that for a liquid IRS (e.g. EUR 5Y) pre-trade LIS is 70% trade percentile and SSTI is 60%.

While for post-trade the LIS is 70% volume percentile and SSTI is 60% volume percentile; unless the volume percentile is greater than 97.5% trade percentile, in which case the trade percentiles of 90% and 80% are used (this addresses the bias caused by a very small number of transactions of very large size).

In exceptional circumstances where a liquid instrument does not have a sufficient number of trades (1,000 trades in the period), the threshold floor values would apply.

Again the same yearly basis determination process will be used.

So we will know the threshold sizes by July 3, 2016, which will then apply from Jan 3, 2017 to May 18, 2018.

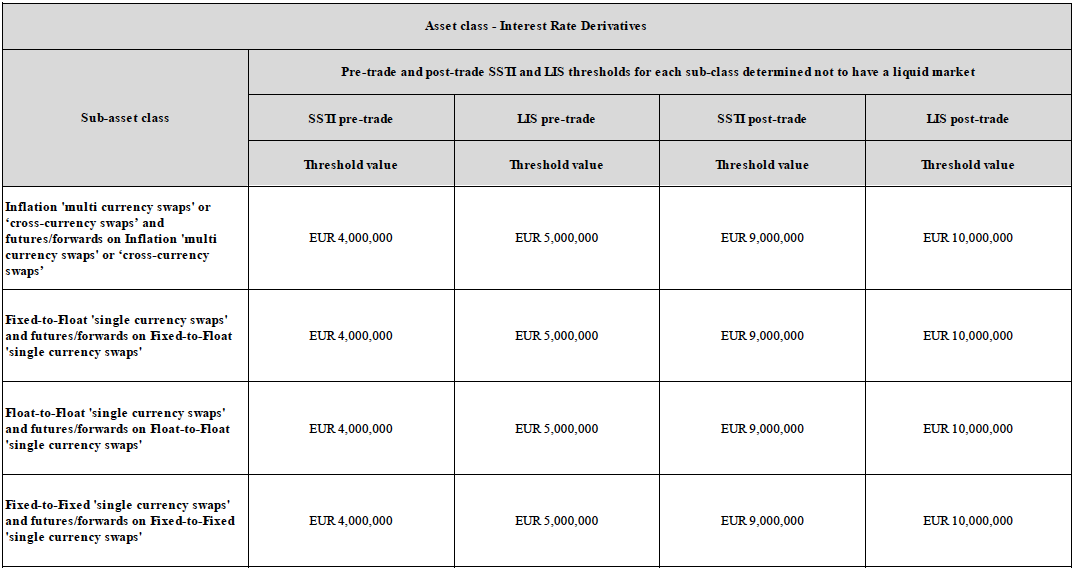

And for Financial Instruments that are determined to not have a liquid market, the following thresholds apply.

Well that completes the definitions and meanings.

Phew! I hope you are still with me.

An Example

Time for a few simple examples.

RFQ for a EUR IRS 5Y in 25m notional size

This will surely be a Liquid Market, meaning that pre-trade the quotes provided to the RFQ will be made public in real-time (as technologically possible) and all at the same time.

And post-trade details will be made public, including execution time-stamp, instrument code, price and size.

RFQ for a EUR IRS 13Y in 25m notional size

This will likely not be Liquid, meaning that no pre-trade quotes will be public and on trade execution only on T+2 business days will details be made public.

RFQ for a EUR IRS 5Y in 200m notional size

This will likely be Liquid and above the LIS or SSTI threshold for pre-trade but below the post-trade thresholds.

Meaning no pre-trade quotes are made public but on trade execution, details will be made public in real-time.

RFQ for a EUR IRS 5Y in 500m notional size

This will likely be Liquid and above the LIS or SSTI threshold for pre-trade and post-trade thresholds.

Meaning no pre-trade quotes are made public but on trade execution, details will be made public on T+2 business days.

Final Thoughts

Thats it for MiFID II and transparency.

I am sure you will agree that the transparency changes are profound and significant.

The pre-trade rules in particular are more far reaching than Dodd-Frank.

There is further detail on Derivatives that I have left out today for clarity’s sake.

And then there is a much wider scope, Futures, Derivatives in Other Asset Classes, Bonds, Equities, …

I plan to cover further aspects of MiFID II in future blogs.

I look forward to a world of more data and more transparency.

Roll on Jan 2017.

In post-trade transparency who should make public the transaction in the following scenarios:

– An asset manager trade OTC a swap with a European counterparty?

– An asset manager trade OTC a swap with a non-European counterparty?

– Etc.

Also which instruments are in scope for post-trade transparency? Does it includes any OTC including FX Forward, NDF, etc.?

If the trade is done on a Trading venue, then the Trading venue will make public.

If it is not on a trading venue, then an Investment firm is required to make public via an Approved Publication Arrangement (APA). APAs are third-party firms authorised under MiFID II to provide such a service.

If both parties are Investment firms, then generally the seller party is required to make public, unless only one of the parties is a Systemic Internaliser and a buyer, in which case this party is required to make public.

For non-European counterparty, the answer is not a simple one, or at least I have not found it yet. So that is a topic for another day.

The instrument list is very extensive and yes for FX it includes FX Forwards and NDFs.

Thank you for the interesting summary and examples. What is your prediction on how it’s going to affect the market in terms of trading trends and new businesses leveraging this public information.

Hello,

This is very interesting.

One question I have though: now a party trading in derivatives is already obliged to report trades under EMIR within a few hours after completion to a global trade repository. It looks to me as if this new MIFID II rules are partly the same as the EMIR rules (except for some other fields). Is it possible to use EMIR upload to a GTR for the MIFID II rules as well? That would reduce workload for trading parties (for so far it concerns the post trade reporting obligation). Do you have an idea?

This would make sense, however I believe EMIR trade reporting is required by end of next day (T+1) and the TRs only make aggregate data public.

Consequently this path would not satisfy the MiFID II requirements on transparency.