- EUR swaps trading is intriguing on US holidays

- We don’t have many data points to play with…

- ….but the data shows continued EUR Swap activity on-SEF on US Holidays.

- Of this activity, much of it is client trading, which I find surprising.

- These volumes naturally filter into the data for Client Clearing at LCH on US Holidays..

- So whilst ISDA find evidence in the counterparty data of “liquidity segregation” along geographic lines for Dealer business….maybe the same isn’t true for Client business?

- The fact that we see a sharp drop in Dealer-to-Dealer business on US holidays, but not in Dealer-to-Client business on-SEF suggests that some non-US clients must value the workflow and electronic trading benefits of SEF trading.

Happy Thanksgiving!

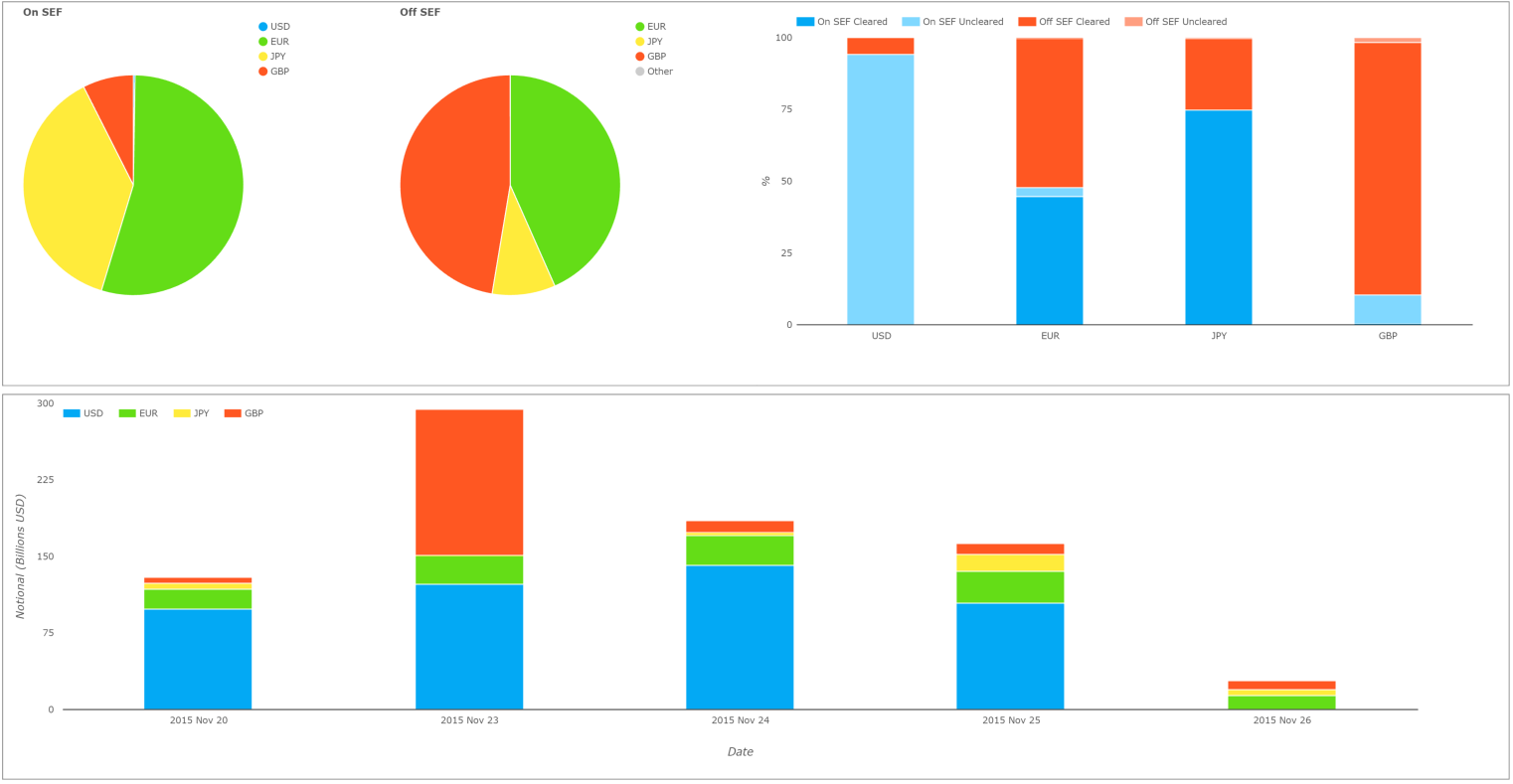

If you logged on to our website on Friday, you will have seen something fairly unusual:

Showing;

- For Thursday 26th November, almost no volume in USD swaps

- Of the reported activity in USD swaps, most of the activity was on-SEF and uncleared. This probably represents some kind of reporting anomaly, so I won’t dwell on this.

- Continued volumes in EUR, GBP and JPY swaps

EUR Swaps On versus Off SEF trading as a percentage share per month in 2015 - For EUR swaps in particular, nearly 50% of volumes were traded on-SEF. This compares to a normal average of around 18-20% – see chart to the right.

USD Holidays

I’m not surprised that we saw almost no volume trading in USD swaps last Thursday, due to the Thanksgiving holiday in the US. That is consistent with the volumes we see reported to SEFView by each individual SEF on all USD holidays – i.e. USD swaps just do not trade when the UST market is closed.

However, what I did find surprising were the non-USD volumes reported by the SEFs on Thanksgiving:

Here we see that;

- Daily volumes in non-USD swaps have been erratic throughout November.

- However, Thanksgiving, a USD holiday, was far from the worst day for volumes.

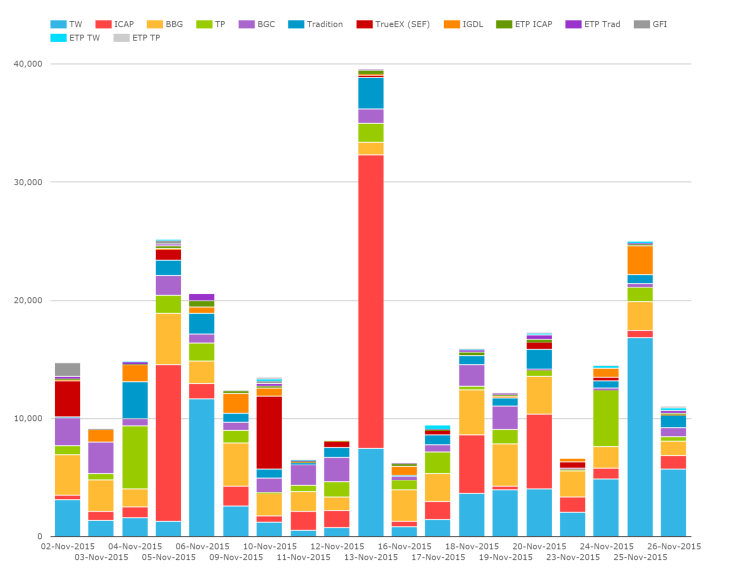

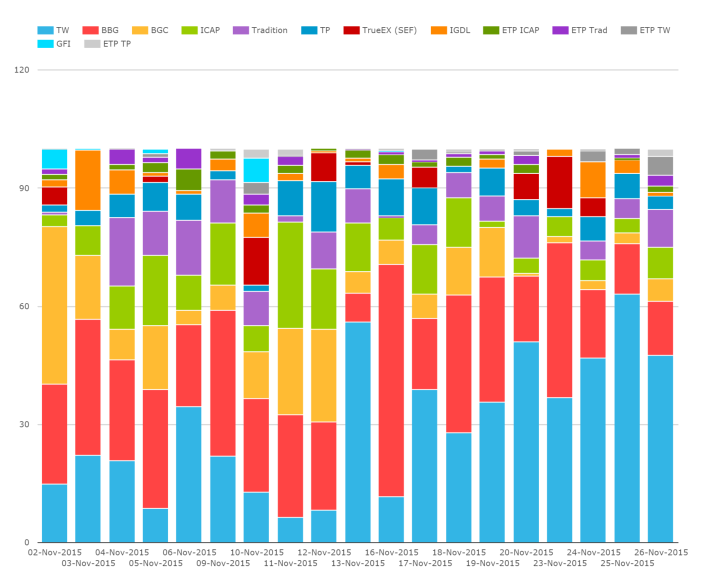

- Tradeweb had the lion’s share of volumes on this day, with a market share on both 25th and 26th November last week at the highs for the month:

- On that chart above, we can see that D2C activity on Thanksgiving was over 60% of the market.

That last point got me thinking – because it really surprised me. My interpretation of SEF-trading on US holidays has typically been that it is volumes recorded by London-based US banks. But if that were the case, why don’t we see more volume in D2D space on US holidays and zero volumes on the D2C platforms? In addition, I had expected BSEF to outperform Tradeweb, because common wisdom states that many of the smaller interbank tickets now trade with a simple click on a Bloomberg terminal. Strange.

Volumes vs ADVs on USD Holidays

Using SEFView, I downloaded daily data for both EUR and USD swaps for 2015. I then calculated Average Daily Volume each month, and finally calculated the percentage of notional that trades on a US holiday compared to these monthly averages.

For USD swaps, the story is consistent – little to no volumes trade on a US holiday. This applies to both Dealer-to-Dealer and Dealer-to-Client SEFs, although D2C venues did see slightly more volume on Good Friday (a half day, according to SIFMA recommendations).

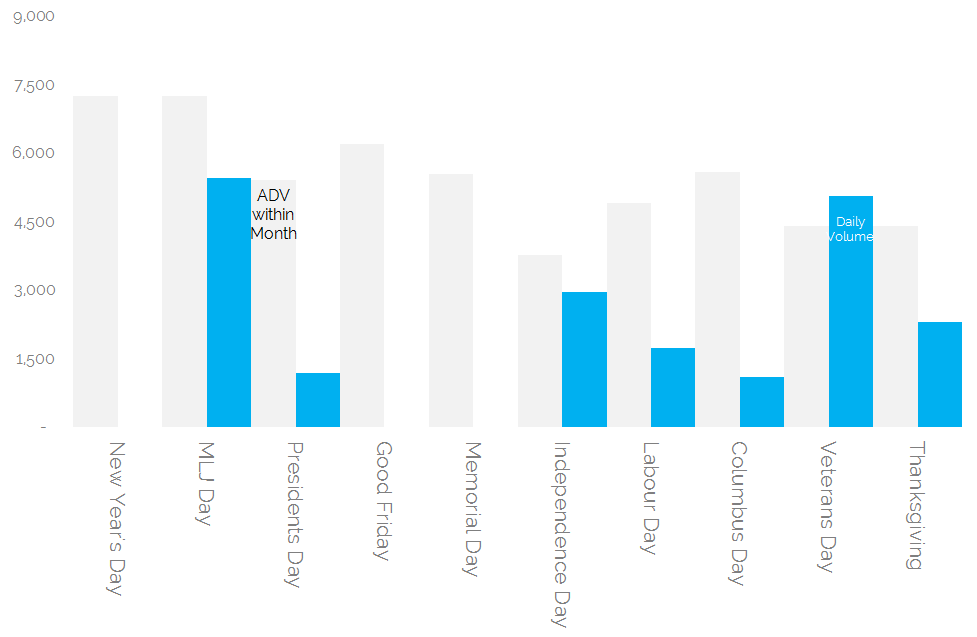

But for EUR Swaps, we see a completely different story. First for Dealer volumes:

Showing that on-SEF EUR Swaps traded almost as normal on Martin Luther King day, Veterans Day and even Independence day this year. This kind of activity, as I said at the top, may broadly be attributed to US banks operating EUR franchises out of London, plus some Australian and Canadian banks who prefer to trade on-SEF. Generally speaking, whilst these market participants are free to trade off-SEF as well, maybe they have become more ambivalent as time wears on?

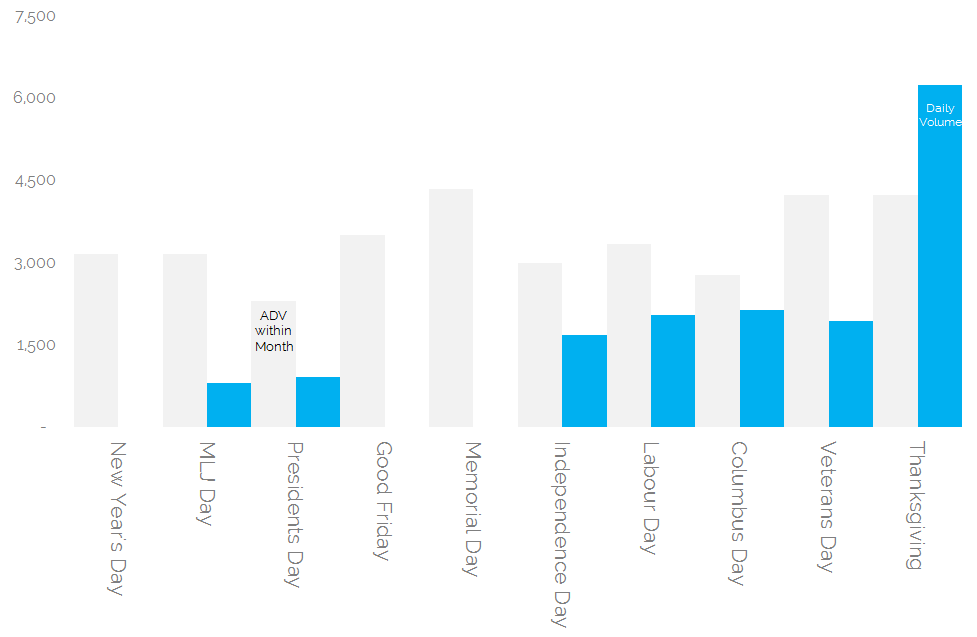

Now, what about EUR on-SEF Client trading on US holidays? Surely there are no US clients in the office to trade with? So there might be prices, but who would choose to trade in a reduced liquidity pool compared to Off-SEF trading? A lot of people, it turns out!

Showing;

- More and more trading on-SEF throughout 2015 on US holidays in EUR swaps. Bizarrely, Thanksgiving really was a bumper day for volumes, both compared to previous holidays and other days in November.

- So who are these clients who trade EUR swaps on-SEF on US holidays? And why don’t their volumes filter down in a more meaningful manner into the D2D market?

- As we said at the top, much of these D2C volumes were transacted on Tradeweb.

- Using SDRView, I’ve checked Compression volumes, and these are very low on Thanksgiving. So it’s not something as simple as that.

ISDA Liquidity Fragmentation

Looking at what else has been written around these ideas, ISDA are very keen on the concept of bifurcated liquidity pools – namely a US-persons EUR swap liquidity pool versus a Europeans-only pool. There is plenty to read on this in their 3 or 4 reports on the ISDA Research pages. In summary, they make a very fair assumption that LCH is the global heart of all cleared EUR swap liquidity and look at trades between US Persons, Europeans only and US Persons with Europeans.

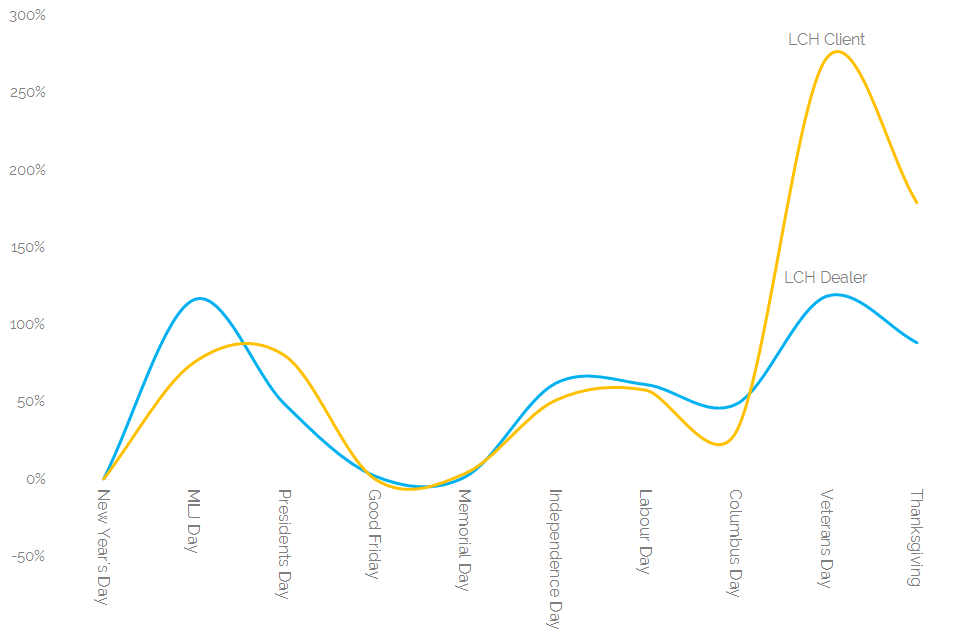

Also noteworthy about the data-set that ISDA use is that they only consider dealer volumes. So I wondered if we saw anything similar using CCPView for Client trades.

Unfortunately, we don’t have the detailed counterparty information that ISDA are privy to, but we can look at how cleared EUR swap volumes at LCH change on a US holiday as a rough proxy. This should give us some idea of how many clients are US-based (SPOILER: I thought clients would be much more US-centric than the data suggest, particularly given the absence of a Clearing Mandate in Europe).

Showing;

- Consistent with the SEF data, clients really aren’t fazed by the thought of trading in potentially reduced liquidity circumstances on US holidays for EUR swaps.

- On the two most recent US holidays (Veterans Day and Thanksgiving), there has been a lot of Client activity.

- This is less surprising for cleared data than for SEF data, because we are considering a “global” liquidity pool, but I did assume that much of the client-clearing activity at LCH was US-centred.

- Maybe this is why the CCP basis is much tighter in EUR than USD? i.e. there is less of a geographical bifurcation of the cleared EUR swaps market leading to a single pool of liquidity (LCH)?

- The single caveat being that we have very few data points here to draw trends or conclusions from!

In Summary

- It is noteworthy how much on-SEF activity there is in EUR swaps when US market participants are absent.

- This activity is generally down to continued client trading.

- For example, on Thanksgiving, nearly 50% of EUR swaps volume traded on-SEF – compared to a typical average of 18-20%.

- Generally speaking, there is a drop in Dealer-to-Dealer activity both on-SEF and across the global pool of liquidity at LCH on US holidays.

- This has not been replicated recently in Dealer-to-Client activity on the same days.

- We have too few data points to be sure, but we may have a more global client base trading on Dealer-to-Client SEFs than just a US pool of names.

- This could be a further sign that the workflow and electronic trading benefits offered by trading on-SEF are being valued by the market.