- 16% of the global EUR D2D swaps market is now on-SEF.

- This has recently increased above the levels we saw in January 2021.

- We do not know why there has been another increase in EUR SEF trading. But the data shows it is happening!

- US venues continue to be the main beneficiaries of Brexit in the derivatives world.

It’s time to run our Brexit-impact analysis again. As per our previous blogs (see our January, February and March analysis), we look at how much of the global Rates market now executes on US venues (SEFs). There has been a marked increase in the amount of derivatives executing on SEF in 2021. This has been a result of Brexit, where the US regulatory regime is the main jurisdiction that benefits from equivalence for both UK and European counterparties.

Data Methodology

CCPView provides a global view of cleared Derivatives markets. Most CCPs split their activity between Dealer (House) and Client volumes.

SEFView provides us with total volumes executed on-SEFs. Like CCPView, these volumes are uncapped, reflecting the true volumes executed (even above the block thresholds).

The SEF world is split between interdealer central limit order books (CLOBS) such as those operated by tp-ICAP, BGC, Trads etc. These are all D2D venues. Tradeweb and Bloomberg, for Rates, are RFQ platforms and trade Dealer to Client (D2C) volumes.

We can therefore compare the D2D volumes on-SEF versus the Dealer volumes in CCPView to calculate the percentage of the global dealer market that is executing on-SEF.

We do the same for D2C volumes on-SEF versus Client cleared volumes in CCPView to calculate the percentage of the global client market that is executing on-SEF.

The Brexit-effect is pretty clear! On to the charts….

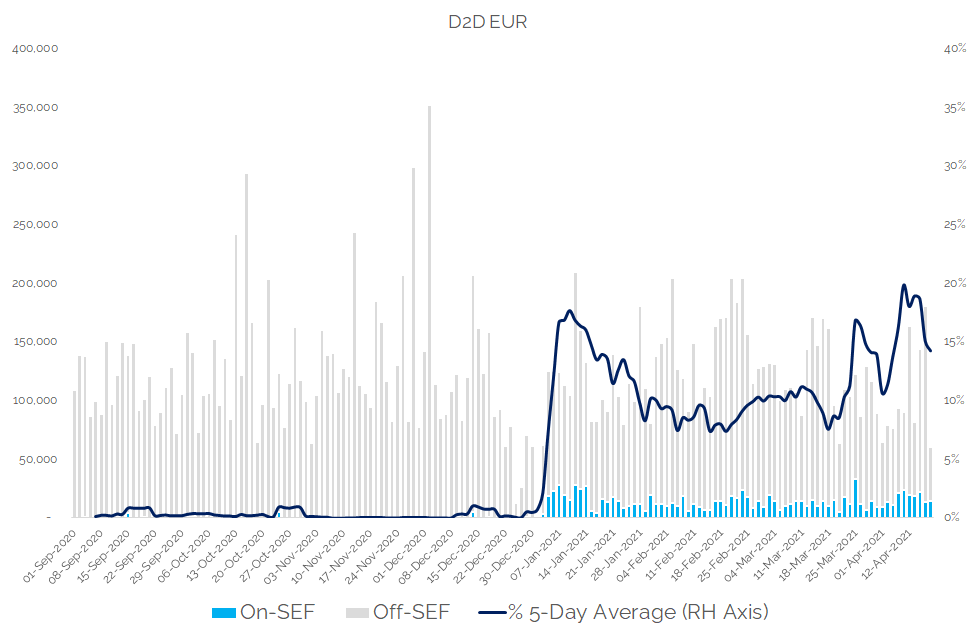

EUR D2D Market

What portion of the global D2D EUR swaps market is currently executing on-SEF?

Showing;

- EUR swap trading was rarely seen on D2D SEFs during Q4 2020.

- 11% of the global EUR D2D swaps market executed on-SF in Q1 2021, a huge increase.

- This has again increased in Q2.

- 16% of the global EUR D2D swaps market has executed on-SEF so far in Q2 2021.

- The peaks seen in recent days up to 27% of the global market are even larger than we saw in January.

- This is particularly surprising given that the amount of on-SEF trading had reduced slightly at the end of Q1 down below 10%.

- We believe that the initial move to SEF trading was entirely down to Brexit.

- It would be interesting to hear why there has been even more recently?

Since our previous blog in March 2021, we were wrong to call it a “new status quo”. It is notable that the proportion of the EUR D2D swaps market executing on-SEF is again increasing and above the levels we saw in January.

Why is this happening and what will the final “status-quo” look like? We can only follow the data to find out!

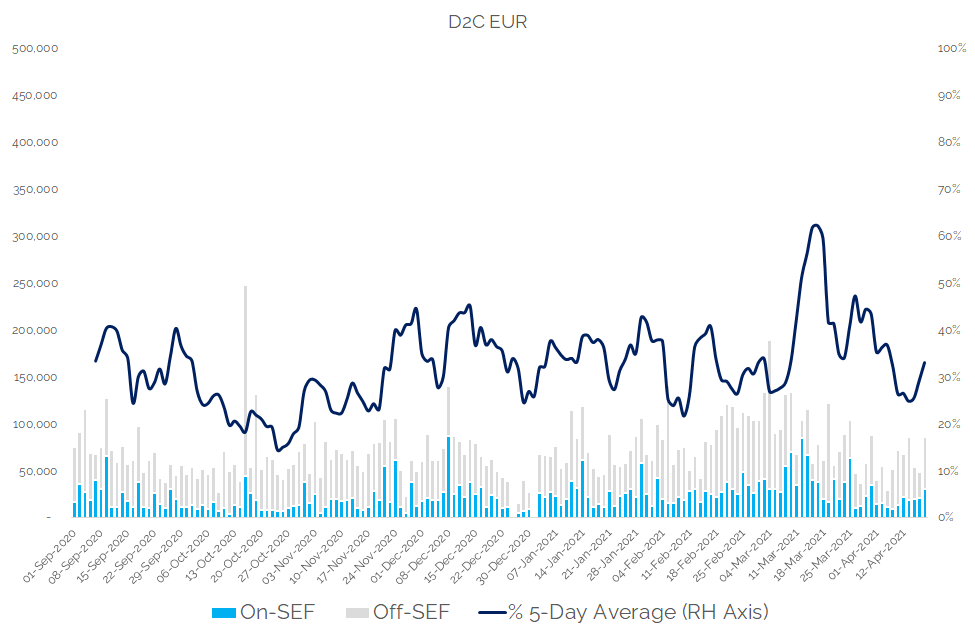

EUR D2C Markets

In D2C markets, the EUR market has seen little impact from Brexit. We don’t see any significant change in client behaviour when comparing EUR volumes on D2C SEFs to client-cleared volumes in EUR:

In Summary

- 16% of the interdealer EUR swaps market has executed on-SEF so far in Q2 2021.

- On some days, 27% of the global EUR swaps markets has been executed on SEFs.

- This is an increase from the 11% average we saw in Q1 2021.

- There has, however, been little impact to Client markets.

- The interdealer move to SEFs in EUR has recently increased again, even beyond the January amounts. Why?

- We need to keep an eye on the data to follow this trend.