Today I want to look briefly at the reported solvency of FCM’s during the most recent market panic.

Back on February 5th of this year, the US equities market suffered a volatile day and significant losses. The Dow Jones index had its worst ever one-day loss in terms of points (down 1,175), and other indices were similarly hit. The story of the day was that volatility was back in the equities market, with the volatility “index” (the VIX) more than doubling during the day. Further, crowded trades betting against volatility, such as in the inverse VIX (the XIV), saw losses of 90%, as prescribed hedging/selling had to take place. Interest rates were also volatile with the 10-year rate off 6 basis points, and just about every asset class saw some sort of panic.

BRIEF LESSON IN SEG FUNDS

I have talked here a few times about the various regulatory FCM capital measures, and have periodically published league tables of which FCM has the most client funds on deposit. The important one (for Futures) is Segregated Funds or “Seg Funds” for short. This measures the amount of funds on hand to cover clients’ margin requirements at clearing houses.

In the US, regulation 1.55(o) requires FCM’s to publish a daily “Seg Funds” report , detailing the amount of Seg Funds on hand, as well as the amount of Required Seg Funds. The idea being that there should always be enough funds to cover all of their customers required margin. And if there is a shortfall, the FCM will top it up on behalf of their clients.

The horror story this all tries to avoid is insolvency and the knock-on effects. Let’s assume you and I were the only client of an FCM. We each deposit $10,000. So Seg Funds is $20,000. With no positions, the required funds is 0. Everyone is happy.

But let’s assume you lever up, go long the XIV, and your required margin is the full $10,000 that you posted (say to cover a $50,000 position in the XIV). Let’s also assume I have taken the opposite position and am short the same amount of the XIV. On this particular day (Feb 5, 2018), you would have lost 80% of that, or -$40,000. You have lost $30,000 more than you posted to our FCM and would be getting an urgent phone call. I would have made $40,000.

The good news, in this example, is that the FCM can comfortably make the net margin call to the clearinghouse ($0). However CFTC regulation 1.22 “prohibits an FCM from using one customer’s funds to meet the obligations of another customer”. In other words, they can’t just use $30,000 of my windfall to cover your losses, as this leaves the door open to me losing that money if you never paid up, leading to our FCM having to close their doors and me without my $30,000. Hence, they need to demonstrate they have $30,000 of their own capital dedicated to client’s Seg Funds.

In day-to-day practice, this $30,000 comes from the “Residual Interest” buffer they keep on hand. This buffer is delicately sized to be large enough to cover bad days, but small enough to not be a capital drain on the business (I dedicated an entire blog to residual interest last year.)

DATA

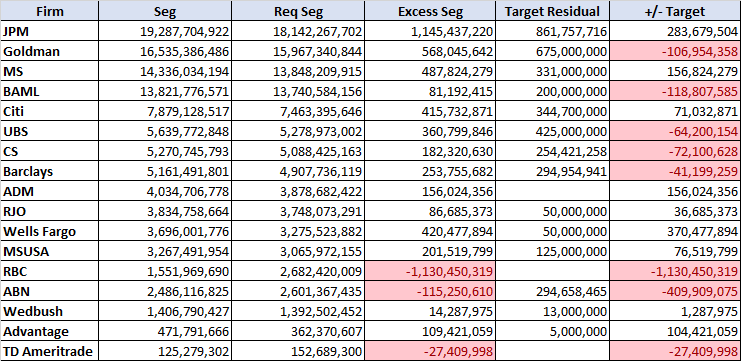

That’s the brief lesson on Seg Funds. So how did the FCM’s do on February 5th? Unfortunately, I did not have the foresight to gather all of the FCM reports on February 6th. But I know a guy (or is it a girl?) who’s into this stuff, and did have the presence of mind to do just that! So let’s have a look.

The data covers nearly all of the top FCM’s in my most recent league table, with the exception of SocGen (couldn’t find the correct website for their data).

The table shows:

- “Seg” – the amount of Seg Funds on hand

- “Req Seg” – the amount of Seg Funds that is required

- “Excess Seg” – the surplus of funds available. If this is negative, it’s not good.

- “Target Residual” – the FCM’s pre-reported (monthly?) goalpost for how much extra funds they plan to have around

- “+/- Target” – how their excess funds compare to their target

I’ve sorted this by the amount of Required seg funds (just like my league tables I publish). Interesting to note:

- 3 firms were “Under-Seg”. RBC, ABN, and TD.

- 8 firms ended the day with an actual excess less than their target excess. I’m not informed enough to know if this is frowned upon. On one hand, and long as they are not under-seg, it still demonstrates that their target buffers were sufficient. On the flip side, it demonstrates that the firm did not top up those buffers with more of their own funds on the day.

- Generally speaking, the larger firms fared (or topped up) the best.

And of course with over a month of hindsight now, it’s worth noting that none of the FCM’s went bust. Though there is at least one lawsuit I am aware of where an FCM is trying to recover margin payments from a firm that went bust.

MY TAKE

What do I make of all of this? The thing I struggle with the most is – and I’m no expert – but how do you end up under-seg? Does your operations team look at their watch at 5:30 and say “My son has baseball practice in 10 minutes, gotta go”? Is the funding just not available to top up the seg funds? Are they not aware they are under-seg when they go home? Do they just trust their clients will top them up the next day? Are the funds actually there, but just don’t make it into the “Seg Funds” report for some reason?

I have to think that in most cases, the funds are “somewhere”. So maybe, in our example, you lost $40,000 on your long XIV position in the CFTC regulated asset classes, but the “Firm” as a whole also knows you as a prime brokerage client that made a killing being long put options on the S&P. So, as a whole, the firm is covered, it’s just that the CFTC regulated bucket looks short.

But perhaps I am just wearing rose-tinted glasses and choosing not to look at the reality. Alas, I don’t have an answer. I’d be interested to know if anyone does.

FINAL SIGNOFF

Importantly, I would like to inform you that this is my final blog. After 5 years with the firm, I am going to be taking some time off. I remain a strong advocate of firm and all that we have accomplished. You’ll be hearing lots more from Clarus. Which leaves me just to thank you for taking the time to read my posts. After 144 posts over 5 years, I’ve learned a lot and enjoyed hearing from and meeting many of you. On to the next chapter.