We often monitor the FCM data within the US, primarily to gauge our quarterly FCM rankings (eg Year End 2017).

Avid students of the FCM data will also know that besides sheer customer margins and customer funds reporting, these reports also reveal how much excess funds the FCM’s carry alongside the customer funds (aka Residual Interest). We’ve touched on this before in an article last year, but I wanted to have a closer look at this.

What is Residual Interest

Your FCM holds your client balances, and by law, they have to keep these secure and not touch them for anything but requirements stemming from your own accounts, primarily to cover your margin requirements. Specifically, the FCM cannot use Client A’s funds to cover losses for Client B, nor can the FCM use Client A’s funds to cover the banks prop desks’ losing bets in European debt.

The general idea behind Residual Interest is that the FCM has its own funds (cash) that can act as a cushion to make sure that their clients obligations are fulfilled, including when the client may not be able to make good on a payment to the FCM. This could be as simple as a time delay in payment, to something more sinister such as a client default.

As the NFA website puts it:

- “… if a customer fails to have sufficient funds on deposit with an FCM to meet the customer’s obligation, then the FCM must use its own funds to make up any deficiency in a customer’s account”

- “The excess funds in these accounts are referred to as the FCM’s residual interest and the funds are for the exclusive benefit of the FCM’s customers while held in these accounts.”

- “The FCM’s policies and procedures must establish a target amount … that the FCM seeks to maintain … to reasonably ensure that the FCM remains in compliance with … customer collateral requirements.”

The CFTC also has a report on this topic (back in 2013) that says much the same thing, but additionally points out practical examples whereby in many cases, clients are operationally unable to deliver margins to the FCM in time for same day calls, and as such, makes the case for having enough residual interest to cover those clients until they can deliver funds. In fact, their rule states that FCM’s residual interest must be at least equal to their clients under-margined accounts from the previous day.

How Much Residual Interest Is Held

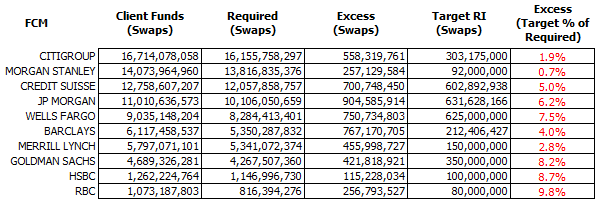

Below, I have taken January’s FCM report for the top 10 Swaps FCMs. Let’s have a look at these numbers.

A brief description:

- Client Funds is a combination of two values:

- Total cash and securities the FCM’s clients have deposited to support swaps

- PLUS the total cash and securities the FCM has kept aside to support client swaps

- Required: the amount of required margins these clients have generated with positions

- Excess: This is the “Residual Interest”. It is the FCM’s cash on hand to support client requirements, should they be required.

- Target RI: This is the Target Residual Interest, which is a number the FCM has communicated to their regulator that they intend to keep on hand to support client requirements. The actual excess should always be above the target (or else the FCM has some red-tape to report to regulator)

- The Excess % column reflects the amount of targeted Residual Interest as a percent of how much client margins are required.

What catches my attention is the varying amount of residual interest. Target Residual Interest ranges from $92 million at Morgan Stanley to $631 million at JP Morgan, even though their clients have similar sized margin requirements ($13 bn vs $10 bn). In percentage terms, Morgan Stanley believes it only needs to pony up less than 1% of client margins to maintain their obligations, while some of the firms lower down the list are putting up closer to 10% of the requirements in their own cash.

There’s a real cost of this residual interest, as this is a funded amount, implying a real cost to the FCM to have this cash sitting around. Using a rough 50bp net funding cost, if you are keeping $500 million tied up for the rainy day fund, that’s $2.5 million a year that someone has to pay for. So there is pressure to keep this number as low as possible.

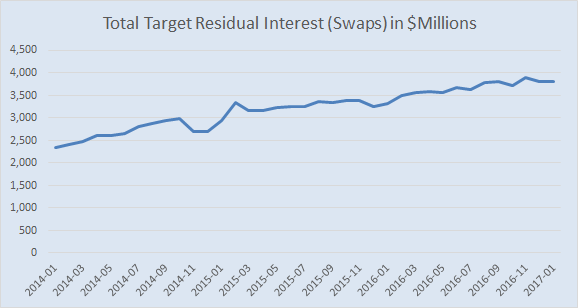

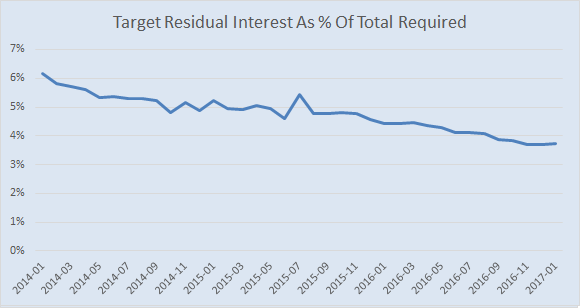

In fact, let’s digest the following two charts:

These tell us that while the total amount of residual interest has increased over the past 2 years, it has not kept up with the amount of margins held. One might say that the amount of FCM’s own funds has not kept up with the amount of risk in the system, but that is probably a stretch – we cannot necessarily equate an aggregate amount of margin with a total amount of risk. But we can see that FCM’s are only putting up 2/3rds of the amount they were putting up 2 years ago (from 6% to 4% of Required Funds).

How to calculate Residual Interest

So, where does the Target Residual Interest come from?

Well, it seems to be more of an art than a science. The NFA has some guidelines which I will summarize below. The considerations should include:

- FCM’s type of Customers

- Customers general creditworthiness

- The type, and volatility, of markets and products traded by the Customers

Nothing there is terribly quantitative. So its worth referencing one sentence the NFA have in their interpretive notes:

The primary purpose of the residual interest is to ensure that sufficient funds are on deposit with an FCM to meet customer obligations

So it would stand to reason that really we want to size this buffer to be at least enough to cover customer obligations over some horizon. As I referred to back in April of 2016, this could be something as simple as a stress test, or something slightly more onerous such as a 1-day VaR analysis. Whatever the approach, you can then choose to have enough residual interest to cover all client losses over a 1 day horizon (that would be large) or something more clearing-house-esque such as being able to support your top 3 client’s worst case losses.

So we suggest at least starting with some sort of historical scenarios, such as the 1-day VaR or Worst-Case-Losses for the client accounts.

Of course, there are qualitative considerations that go into the equation as well. Besides the ones listed above, you would think that the firms ability to monitor their assets (collateral) and liabilities (margins) in a timely and accurate fashion justifies being more aggressive with how much FCM Residual Interest is required.

Summary

I learned a few things by digging a bit deeper into Residual Interest:

- Residual Interest is FCM cash that is only to be used for client obligations

- The amount of residual interest has to cover at least the previous day’s under-margined client balances

- The amount of residual interest held by FCMs vary considerably

- The guidance for adequately sizing Residual Interest is not terribly prescriptive

- The industry seems to have become more efficient, with target Residual Interest % decreasing, over the past couple years.

- We recommend tools to quantitatively size the target residual interest in a way that balances cost and risk appetite