Continuing with our monthly Swaps review series, let’s look at volumes in April 2017.

Summary:

- USD IRS price-forming volume > $1.8 trillion gross notional

- SEF Compression activity in USD IRS > $250 billion

- USD OIS volume was > $2 trillion

- Both USD IRS and OIS are well down from recent highs

- EUR IRS and OIS volume is mostly Off SEF

- USD, EUR, GBP, IRS, OIS and Basis Swap volume was $1.18 billion DV01

- Down from the $1.76 billion in March 2017

- Bloomberg the largest with $366 million

- Volumes down for all SEFs, except BGC

- CME–LCH Switch volume down to $60 billion from $96 billion

- Global Cleared Volumes down at $19.6 trillion, similar to Jan 2017

- In Asia, volumes down at LCH, ASX and CME

- In LatAm, CME volumes up at $582 billion, driven by MXN

- Inflation Swaps at LCH SwapClear down, but above Jan and Feb

- NDFs at LCH ForexClear also down, but similar to Jan and Feb

Onto the charts, data and details.

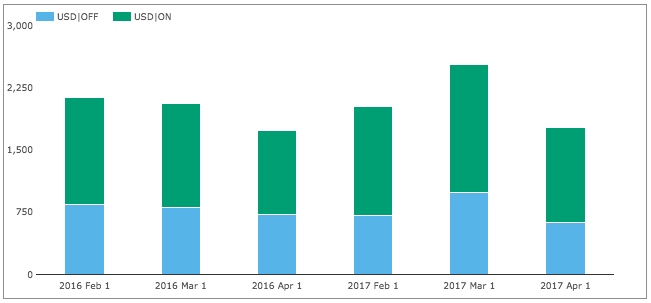

USD IRS ON/OFF SEF

Using SDRView the gross-notional volume of On and Off SEF USD IRS Fixed vs Float price forming trades (Outrights, SpreadOvers, Curve/Flys).

Showing:

- April 2017 On SEF gross notional is > $1.1 trillion

- (recall capped trade rules mean this is understated as the full size of block trades is not disclosed)

- This is 13% higher than April 2016, but the lowest month in 2017

- April 2017 Off SEF gross notional is > $630 billion

- 12% lower than April 2016 and also the lowset month in 2017

- Overall gross notional was > $1.8 trillion

- And On SEF vs Off SEF is 64% to 36%, close to the average

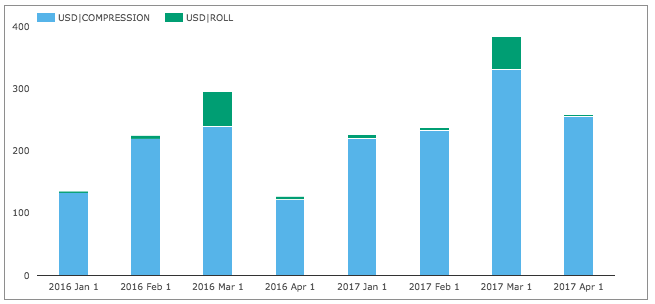

Next On SEF non-price forming trades; SEF Compression and Rolls.

Showing:

- SEF Compression in April 2017 was > $250 billion

- This is 108% higher than April 2016

- And the second highest month in 2017

- 34% higher than a year earlier

A subdued month for USD IRS in price forming, but reasonable in portfolio maintenance trades.

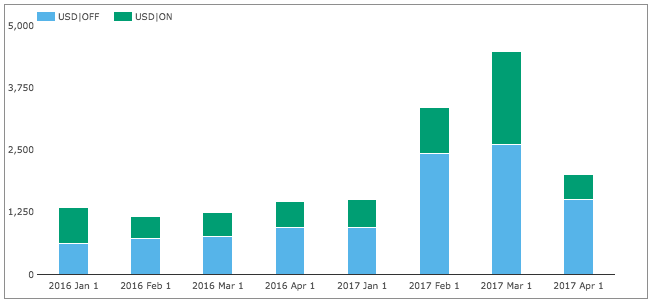

USD OIS Swaps

Next USD OIS Swaps volumes.

Showing:

- April 2017 volumes back down from the highs of Feb and March 2017

- An overall gross notional of >$2 trillion

- (recall capped trade rules mean these are understated as the full size of block trades is not disclosed)

- Off SEF gross notional at > $1.5 trillion is 58% higher than April 2016

- On SEF gross notional at > $0.5 trillion is similar to April 2016

- Overall volume is higher than Jan 2017, but much lower than Feb and Mar 2017

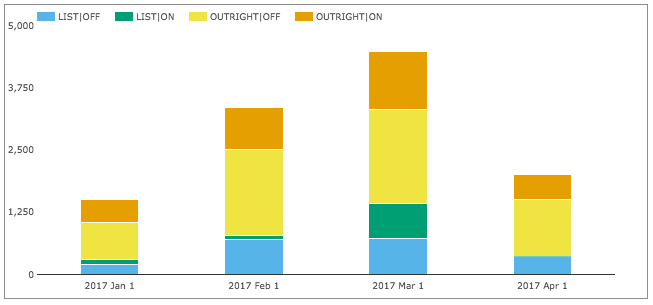

Splitting the volume by List (Roll activity) and Outrights for On and Off SEF.

We see that March 2017 was a record month, specifically for List On SEF (see TrueEx in March Review), but also record volumes for price forming outright trades.

EUR, GBP, JPY Swaps

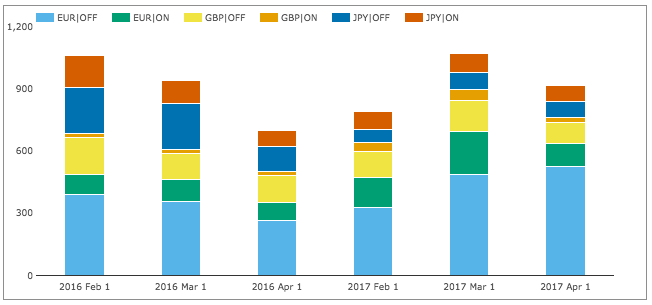

Next On and Off SEF volumes of IRS in the other three major currencies.

Showing:

- Volume in April 2017 was > $910 billion

- 31% higher from a year earlier

- EUR Off SEF is the largest at > $525 billion

- Overall Off SEF at > $700 billion is 64% of the USD IRS Off SEF

- Overall On SEF at > $210 billion is 34% of the USD IRS On SEF

Showing that a much higher portion of EUR, GBP, JPY is transacted Off SEF.

Next SEF Compression activity.

Showing that April 2017 volume was > $85 billion, much higher than a year earlier, the second highest month tis year and 34% of the USD IRS Compression figure of > $250 billion.

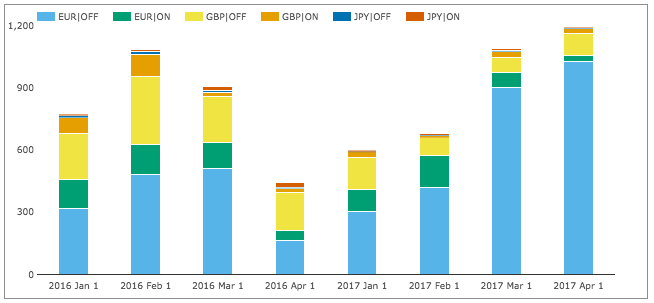

EONIA, SONIA, TONAR

Next lets check how volumes in EONIA, SONIA and TONAR have performed.

Showing:

- Volume in April 2017 was > $1.2 trillion

- 170% higher from a year earlier

- EUR Off SEF is by far the largest at > 1 trillion

- GBP Off SEF is next with > $100 billion

- On SEF volumes are tiny compared to Off SEF

SEF Market Share

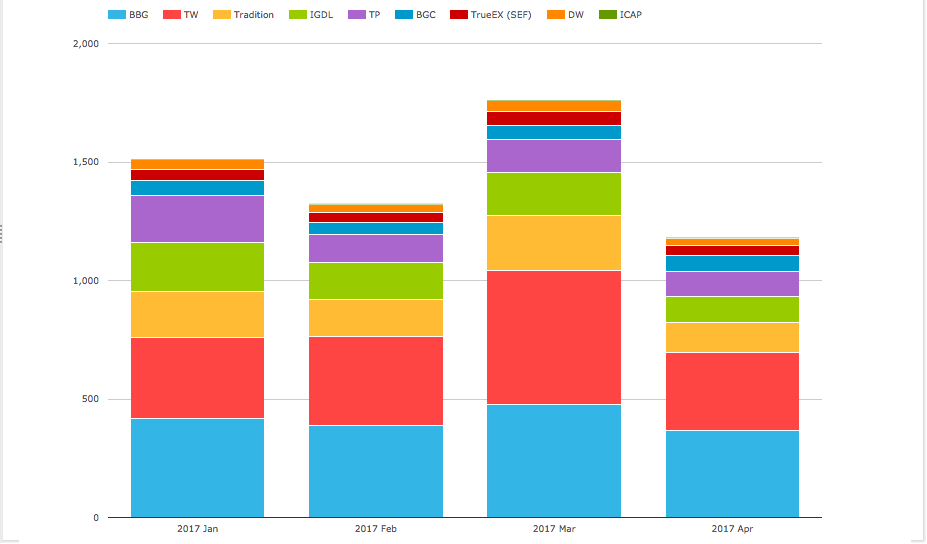

Lets now turn to SEFView and SEF Market Share in IRS including Vanilla, Basis and OIS Swaps.

DV01 (in USD millions) by month for USD, EUR, GBP and by each SEF, including SEF Compression trades for the prior four months.

Showing that:

- April 2017 volume at $1.18 billion DV01 is the lowest in 2017

- Bloomberg is the largest with $366 million

- Tradeweb next with $333 million

- D2D SEFs are all down from prior months, except for BGC

- Tradition with $123 million, followed by IGDL/ICAP with $114 million

- Then Tullet, BGC and Dealerweb

In gross notional terms $1.74 trillion of USD IRS traded On SEF in April 2017.

Meaning that the $1.1 trillion in SDR for On SEF Price-forming and Compression should be increased by 58% to equal the SEF reported number, suggesting a much larger number of trades above block size in the month than usual (given this percentage is usually 30%).

In gross notional terms $633 billion of USD OIS was reported On SEF, compared to the $500 billion in SDR, meaning that the SDR number is understated by 28% due to capped notional rules.

A quiet month for SEFs.

CCP Basis Spreads and Volumes

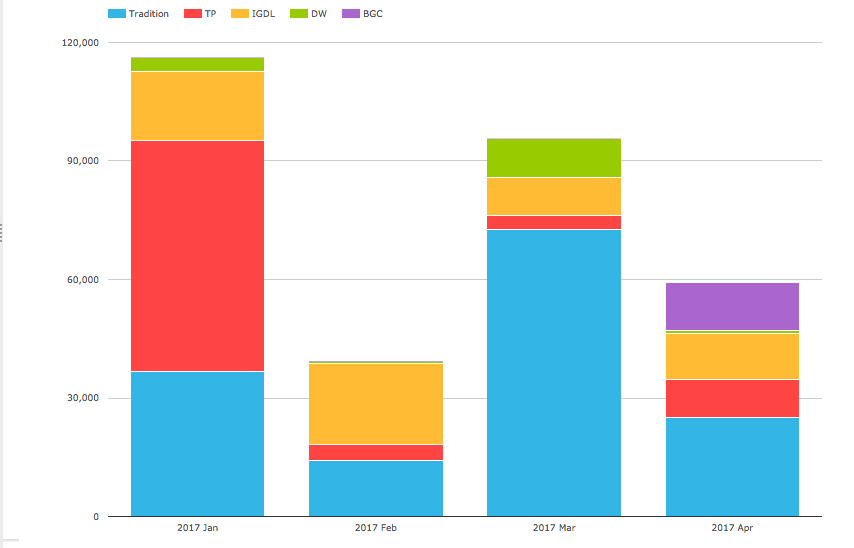

In SEFView we can isolate CME Cleared Swap volume at the major D2D SEFs (on the assumption that this is all CME–LCH Switch trade activity). Lets look at this for the past 4 months.

Showing:

- Overall volume in April 2017 was $60 billion

- Significantly down from the prior month

- Tradition the largest with $25 billion

- BGC next with $12 billion and its highest monthly volume

- ICAP/IGDL with $11.7 billion

- TP with $9.5 billion

CME-LCH Basis Spreads ended the month at 2.95 bps for 10Y and 4.20 bps for 30Y, which are up 0.30bps and no change respectively.

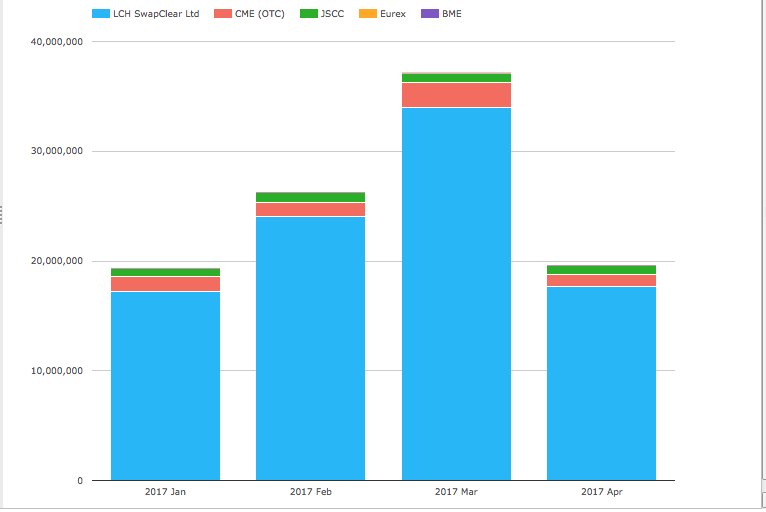

Global Cleared Volumes

Next lets move onto CCPView and Global Cleared Swap Volumes of EUR, GBP, JPY & USD Swaps (IRS, OIS, Basis, ZC, VNS types).

Showing:

- Overall Global Cleared Volumes in April 2017 of $19.6 trillion

- Significantly down from March and Feb and slightly above Jan 2017

- LCH SwapClear volume at $17.7 trillion is just above Jan 2017

- CME volume at $1.1 trillion, is below the Feb volume of $1.3 trillion

- JSCC volume at $773 billion is down from $842 billion in March

- Eurex with $55 billion, down from $79 billion

- BME with $32 million, down from $73m

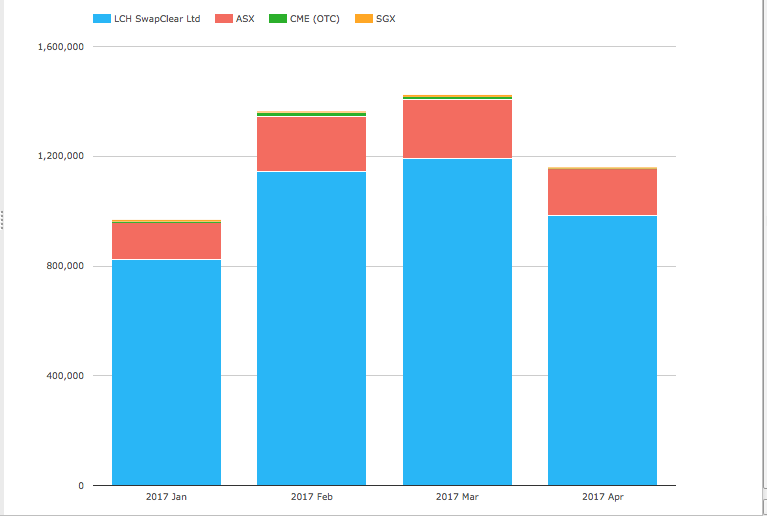

Asia and LatAm

Next the volume of AUD, HKD, SGD Swaps (including Vanilla, OIS, Basis, Zero Coupon).

Showing:

- Lower volumes than the prior month

- LCH SwapClear at $985 billion, down from $1.19 trillion

- ASX at $169 billion down from $215 billion

- CME at $1.4billion down from $9.2 billion

- SGX at $5 billion, up from $8.7 billion

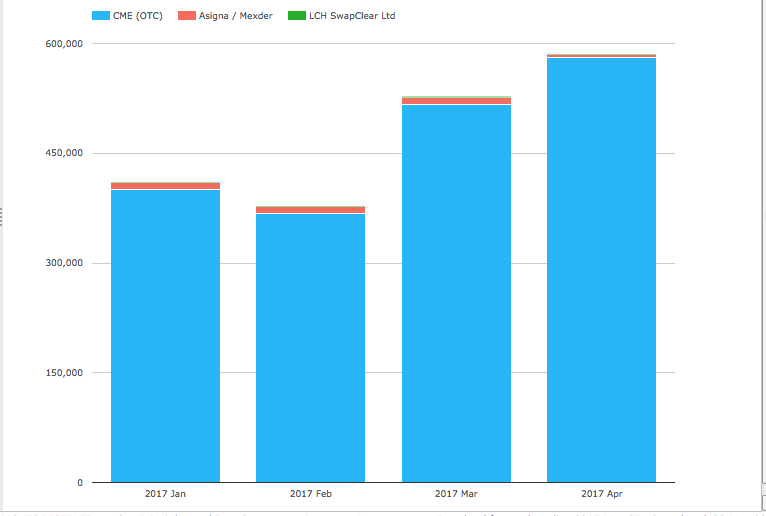

And next the volume of MXN and BRL Swaps.

Showing:

- CME at $582 billion, up from $516 billion in the prior month

- The growth is in MXN, whic is up to $477 billion from $376 billion

- Asigna/Mexder with $3.7 billion, down from $10 billion

- LCH SwapClear with $450 million, down from $1.4 billion

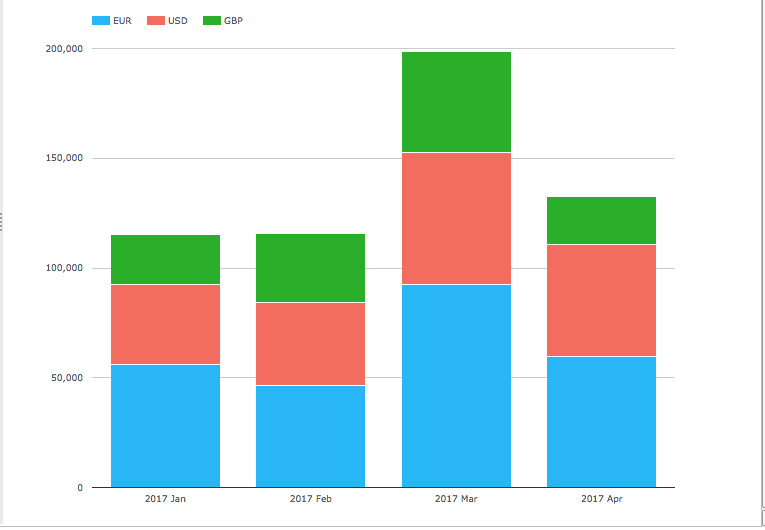

Inflation Swaps

Finally lets look at the two products that have gained the most cleared volume from the Uncleared Margin Rules (UMR), starting with Inflation Swaps.

Showing:

- All the volume is at LCH SwapClear

- Total in April is $132 billion, down from $199 billion

- But above the $115 billion in earlier months

- EUR and USD similar in size this month

Non-Deliverable Forwards

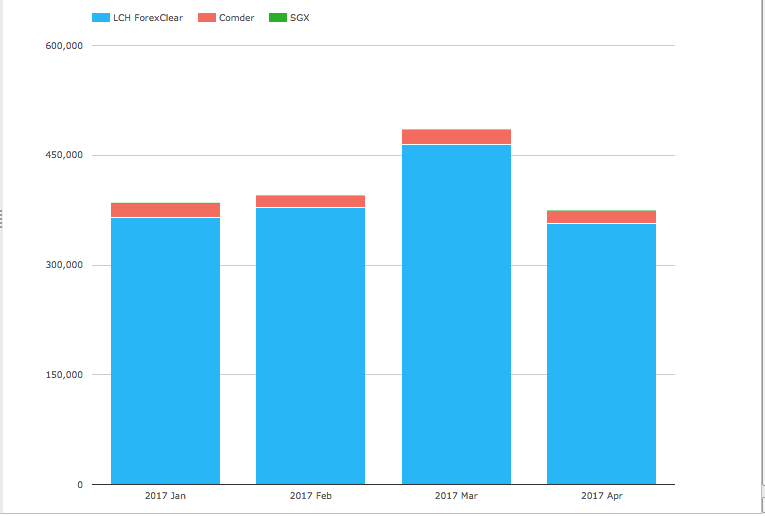

And last but by no means least, NDFs.

Showing:

- LCH ForexClear with $357 billion, down from $464 billion

- Comder with $17 billion, down from $17 billion

So both Inflation Swaps and Non-Deliverable Forwards with lower volumes.

April with Easter holidays showing up to be a quiet month all round.

That’s it for today.

Thanks for staying to the end.

Our Swaps review series is published monthly.