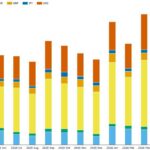

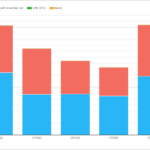

Q2 2026 cleared rates swaps: 17% below the Q1 high but up 23% YoY

This blog covers global notional volumes of cleared rates swaps in quarter two (Q2) 2026, focusing on volumes of OIS, fixed-float IRS and zero-coupon swaps with a material volumes’ share for each currency. Key takeaways In Q2 2026 global core cleared rates swaps volumes were US$262 trillion notional – up 23% YoY but down 17% from their Q1 2026 […]

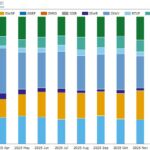

Q2 2026 shares of D2D platform core rates swaps

This blog reviews Q2 2026 D2D platform market shares of major currency rates swaps risk-trading, continuing the quarterly series from Q1 2026 shares of D2D platform core rates swaps. Key takeaways Q2 2026 saw the following D2D platform market share leaders and shifts in each major currency: All the charts and statistics in this blog […]

Q1 2026 shares of D2D platform core rates swaps

This blog covers D2D platform shares of core rates swaps in G6 currencies in Q1 2026. Key takeaways Read on for further analysis and explanation. All the charts and statistics in this blog were sourced from SDRView. Background We focus on the core rates swap products: cleared OIS and fixed-float IRS, of which at least […]

Q3 2025 rates swaps CCP competition

In our quarterly blogs on cleared rates swap volumes, we review CCP market shares across all currencies. However, only a few currencies show meaningful competition between clearinghouses. This blog focuses on the competitive dynamic in those competitive currencies. Key takeaways: In Q3 2025, only four currencies – EUR, JPY, CNY, and INR had more than […]

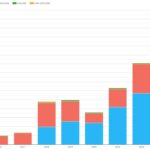

What’s new in AUD swaps in 2025?

This blog looks at another year of AUD swaps activity, continuing from the blog with a similar title published at about the same time last year. Should you want more information on AUD swaps, the blog linked above contains links to several other blogs on the topic. AUD market total size First, we extend the […]

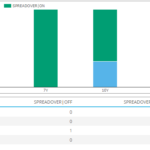

SOFR SpreadOvers are now starting to trade

On June 8, the CFTC’s Market Risk Advisory Committee’s (MRAC) Interest Rate Benchmark Reform Subcommittee voted to recommend market best practice for switching interdealer trading conventions from Libor to SOFR (see release 8394-21). Referred to as SOFR First, it is modelled on the UK’s SONIA First and is a prioritization of interdealer trading in SOFR […]

USD & EUR Swap Volumes – May 2021

USD IRS , OIS and SOFR volumes EUR IRS, OIS and €STR volumes May compared to prior months and 1Q 2021 CCP market share for currency and product CCPView provides transparency on Swap volumes USD IRS From CCPView, USD IRS only, so excluding OIS, Basis, ZC, VNS and FRAs. May with $6.8 trillion, similar to April and down from the high […]

Cleared Swap Volumes and Share – 1Q 2021

USD IRS with record volume in 1Q 2021, LCH share up YoY SOFR Swaps at new highs, LCH dominant, CME share higher than in IRS EUR IRS volumes up, Eurex share up YoY as it’s gains continue €STR Swaps a record month, LCH dominant, Eurex share higher than in IRS JPY Swaps volumes up, JSCC […]

2020 CCP Volumes and Market Share in IRD

In this article I look in detail at the 2020 volumes and market share for OTC Derivatives in Interest Rates reported by Clearing Houses. Clarus CCPView has daily volume and open interest data published by each CCP, which is filtered, normalised and aggregated to allow meaningful comparisons of volume and has been used to produce all the charts below. Table of […]

Swap Volumes in October 2020

In the transition from LIBOR to SOFR, the recent change by Clearing Houses to discount swaps using a SOFR curve instead of a FedFunds curve has long been trailed as a key milestone for higher volumes in SOFR derivatives. In today’s blog I look at how SOFR Swap volumes did in October 2020. I also […]