As September 1, 2016 is the first date for the implementation of margin requirements for OTC Derivatives that are not cleared by a clearing house, I thought it would be interesting to re-visit this topic.

Background

My article Final US Rules on Margin for Non-Cleared Swaps, written in Oct 2015, summarises the US rules and compliance dates.

While Europe, Australia, Singapore and other jurisdictions have not kept to or have postponed the first compliance date of 1st September 2016, US and Japan regulators have stuck to their guns and it all begins next week.

VM & IM has to be collected and posted for new trades executed after 1st September 2016 between financial institutions with greater than $3 trillion outstanding gross notional and specifically IM calculated using either a Standardised Margin Schedule or an Internal Margin model that satisfies regulatory authorities.

The Standardised Margin Schedule method relies on a gross measure with limited netting benefit and as such leads to very high margin requirements and is not likely to be used by any firm.

The task of adopting an Internal Model that is acceptable to regulators and all of a firms counterparts is a daunting one and so ISDA have stepped in and proposed ISDA SIMM as an appropriate model. All or the majority of the large financial institutions impacted are using the AcadiaSoft Collateral Hub as the margin processing solution and this will offer both the Standardised Schedule and ISDA SIMM.

ISDA SIMM and FRTB SA

I covered ISDA SIMM in Nov 2015, with my article titled, Why the ISDA SIMM Methodology is Not What I Expected and now that I am over my surprise (time, momentum, facts on the ground) it is time to re-visit this.

The direction of travel in regulation is without doubt towards standardised models and away from be-spoke internal models and ISDA SIMM has chosen a model that is similar to the upcoming BIS market risk capital regulations; the FRTB Standardised Approach.

I covered FRTB in June 2016, with two articles, first Fundamental Review of the Trading Book – What You Need to Know and second FRTB – Internal Models or Standardised Approach.

Such a choice is sensible in that it makes consensus and regulatory approval easier to achieve and the commonality in the approaches reduces the costs and risks of adopting both.

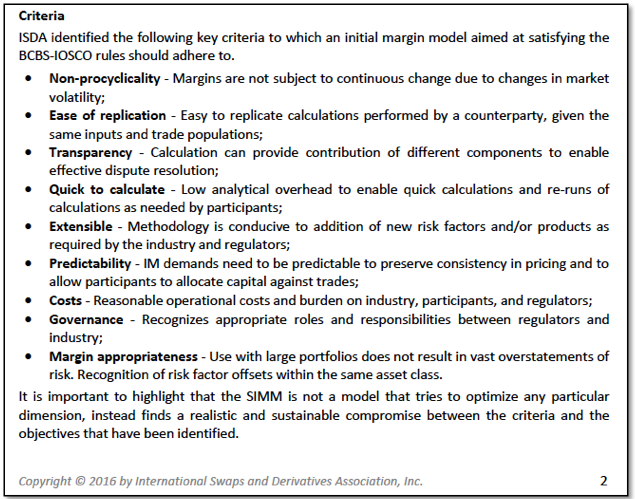

ISDA SIMM Principles

The ISDA document ISDA SIMM: From Principles to Model Specifications (available here) provides a good introduction to the model criteria, which extracted from that document are:

ISDA SIMM proposes an annual calibration of the model parameters which I believe are calculated using a “1+3” historical period, meaning a 1 year Stress period (2008?) and the most recent 3 year period. As such ISDA SIMM is not pro-cyclical in that margin does not increase due to volatility in times of stress, which is a good thing for the health of the overall market, though it may come at the cost of worse margin coverage for individual margin agreements, there being no such thing as a free lunch.

Data needs, costs and maintenance were key considerations for the ISDA WGMR and only the calibration agent (ISDA) needs to have access to historical time-series data, which is used to calculate the weights, volatilities and correlations that are then used by members. This avoids the burden of data licensing costs that would be required were Historical Simulation to be used. Certainly a worthwhile economy, provided of course that any cost to license SIMM is much lower than historical data costs would be.

And similar to the FRTB Standardised Approach, ISDA SIMM utilises a sequence of nested variance/covariance formulae to calculate margin and so avoids the need for a single large variance/covariance matrix covering all risk factors (as would be used in RiskMetrics). The aforementioned ISDA document provides a mathematical justification for the nested formulae, for those of you that way inclined.

I however will move onto looking at a few of the differences between these two methodologies.

Differences between ISDA SIMM and FRTB SA

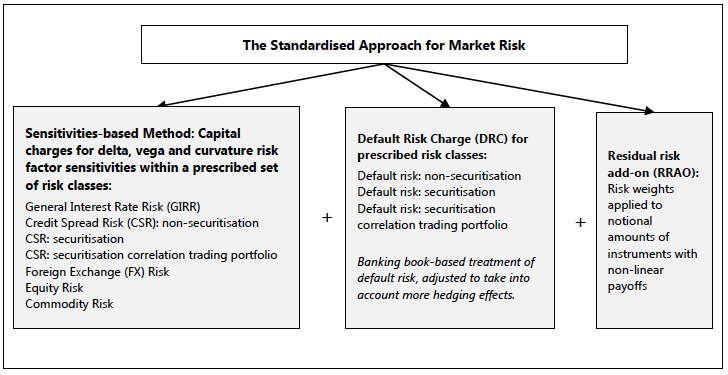

Lets start with a diagram showing a high-level summary of the FRTB SA methodology.

And highlight some differences:

- ISDA SIMM does not need a Default Risk Charge or a Residual Risk Add-On, while it does use the same Sensitivities Based Method for Delta, Vega and Curvature risk.

- ISDA SIMM has six risk classes as opposed to the seven in FRTB SA, the difference arising in the Credit Spread Risk classes where ISDA SIMM has Credit (Qualifying) and Credit (Non-Qualifying).

- ISDA SIMM also utilises four product classes (RatesFX, Credit, Equity, Commodity) and each trade is assigned to a single product class and within each product class the risk class takes its component risk only form trades within that product class. For each product class the total margin is given by a formulae that aggregates each of the six risk classes and the total margin is the sum of the four product class margins.

This last seems subtle but important as it means under ISDA SIMM a Credit Default Swap would have risk in the Interest Rate and Credit Risk classes but these risks are kept separate from the risks of an Interest Rate Swap in the Interest Rate risk class. Meaning that any offset in a risk class across product classes is not recognised, so the IR DV01 of CDS would not offset the IR DV01 of IRS. I think this is direct consequence of the Final US Rules and is different from the FRTB SA.

Other differences include:

- Different weights and correlations, as expected for a model calibrated for capital versus one for margin

- Differences in buckets/nodes, e.g. ISDA SIMM for Interest Rate risk adds 1-week and 1-month buckets

- Vega and Curvature risk may have small/subtle differences in detail, but hard to say without comparing and converting the formulae in the respective methodology documents, so I will leave that to those of you interested in such arcane detail

- FRTB SA has the concept of three different risk charges, for each of high, medium and low correlation and takes the largest of these

- ISDA SIMM has a model for concentration risk using concentration risk factors and thresholds, though this is expected to be inactive for the September 1, 2016 effective data

I will leave it there, as my intention is not to dwell on the differences, but just to point out there are some and to use a well-worn cliche, the devil is in the detail.

The reality is that there is much more similar between FRTB SA and ISDA SIMM, with ISDA SIMM being a variant of the Sensitivity Based Approach in FRTB SA.

And the majority of the differences arise from the requirements of a margin charge as compared to a capital charge, as well as regulatory compliance.

Summary

September 1, 2016 is the first effective date for compliance with Uncleared Margin rules.

The US and Japan are the first and only jurisdictions that will start on this date.

Bi-lateral OTC Derivative trades entered into after September 1, 2016 will be subject to these rules.

The Standardised Margin schedule produces very high IM requirements.

Thankfully ISDA has developed ISDA SIMM as an Internal model for regulatory approval.

ISDA SIMM is very similar to the FRTB Standardised Approach.

With a few necessary differences and a few subtle ones.

UPDATE: We now offer free 14-day trials for our SIMM for Excel product

Until now the focus as been on pushing more products into Clearing.

From September 1, 2016 the emphasis will shift to margining of Uncleared products.

A fundamental shift in the direction of travel?

Only time will tell.

Update : Canada and Switzerland have also met the September 1, 2016 date.