Clarus SDRView consolidates all Swap or Trade Data Repositories that publish transaction level data and have meaningful volume. As only the United States and Canada have transaction level public reporting, our focus has been on these jurisdictions, which provide by far the most interesting and useful data.

European, Japanese, Australian, Singapore and other jurisdictions have periodic (weekly or quarterly) and highly aggregated reporting of transactions or outstanding positions. We see very little value in this data, only occasionally do we look at it, rarely do we comment on it, so we are a long way from seeing any value in collecting transparency data from these jurisdictions.

SDR Sources

Recently we added the CME SDR (for the US) into SDRView.

Showing the CME SDR selected. The others are DTCC (US), DTCC_CA (Canada), BBG (BSDR) and ICE.

BBG has a lot of volume from Oct 2013 to Aug 2018, as the Bloomberg SEF reported its transactions to this until it switched to DTCC, while ICE has some Credit Derivatives volume.

DTCC is by far the largest repository.

Lets look now at CME SDR.

CME SDR – Rates

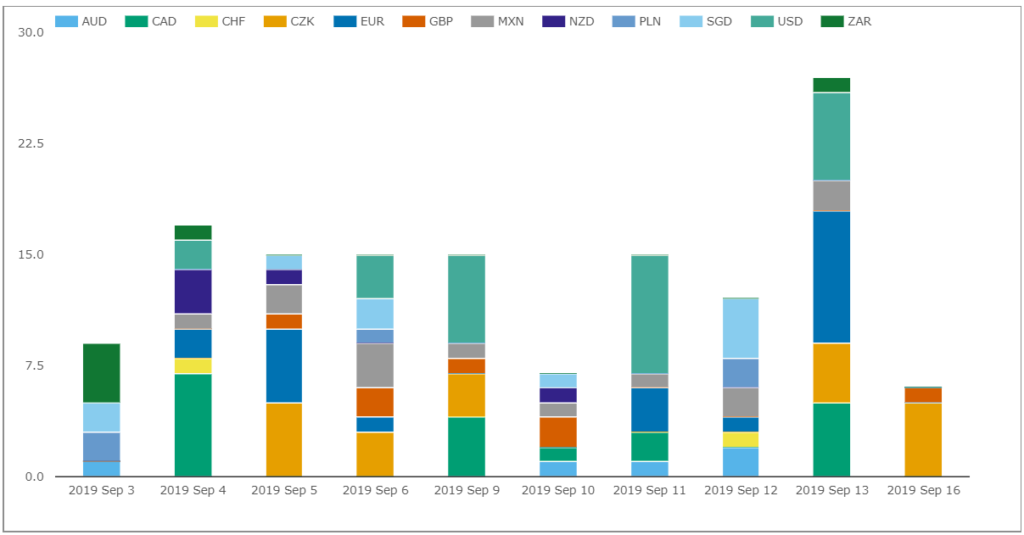

Starting with Rates Derivatives and FixedFloat Swaps.

Showing between 6 and 27 trades each day in the last two weeks, so pretty low numbers, but the range of currencies reported is very interesting. Trades in the twelve selected currencies are reported in this 10-day period, with the list including AsiaPacific, Europen, LatAm as well as North American currencies.

All these trades are Cleared and OFF SEF, which in itself is interesting and is possibly a clue as to the origin of these trades. (More on this later).

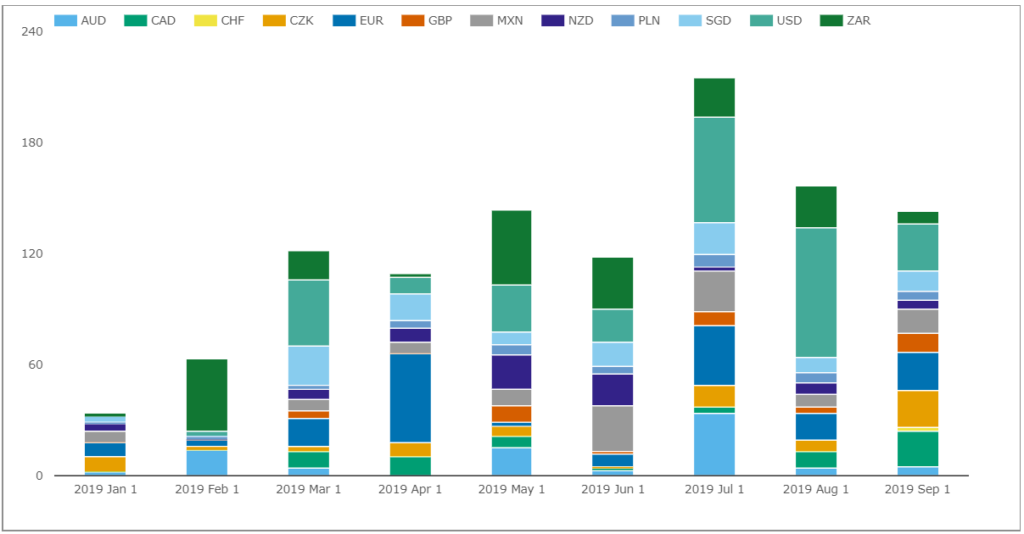

Lets now aggregate the trade counts by month for 2019 year-to-date.

Showing between 34 and 215 trades in these months, again small numbers given that DTCC averages 70,000 trades per month in this period with USD representing 52% by trade count and EUR 19%.

But again rather than the absolute volume, the range of currencies represented as well as the trade level information of price and size is more interesting.

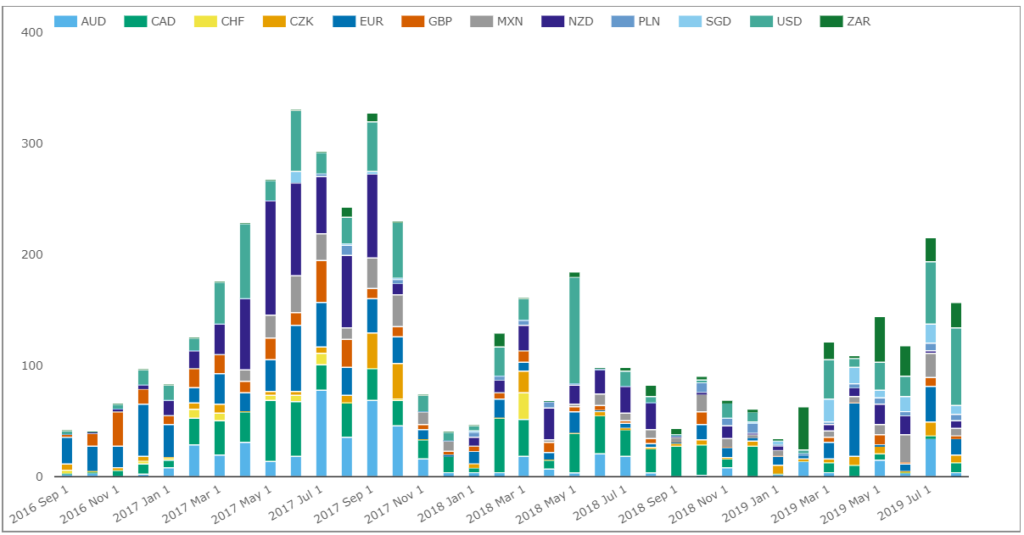

And looking at monthly volume for the past 3 years.

Showing that March 2017 to October 2017 was the peak period for trades reported to and published by the CME SDR, while 2018 fell back and 2019 seems to be on the up again.

It is hard to know what is behind this trend and which firms are reporting these trades or indeed if some post trade process is creating them. The fact that the execution timestamp of all/most of these has a time of 0:00:00, is possibly a clue that they are the outcome of an automated process or it could be a red herring as this information has not been reported to the SDR.

I feel like the answer to the origin of these trades is staring me in the face, if I just spend a bit more time digging, but you know that feeling when something does not quite click but you feel it is close and then suddenly sometime later it comes to you, when you are doing something completely different…

If one of our readers knows, please add a comment below or email us.

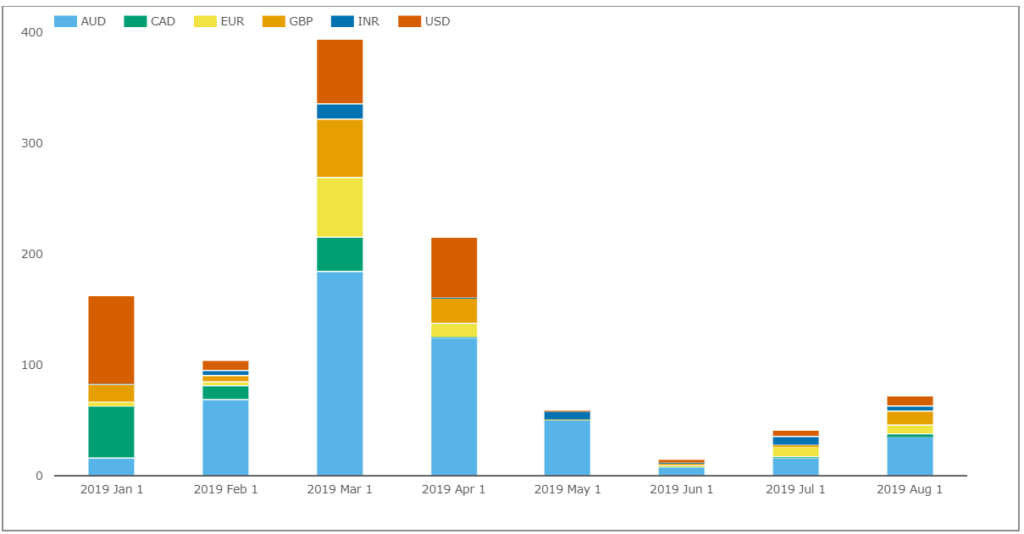

Before I move on from Rates, a quick look at OIS Swaps, as they are the future when IBOR is replaced by RFRs.

Showing a large spike in March with 400 trades, mainly in AUD AONIA, which is the largest trade count in most months. Again the range of currencies is more interesting than the size of the numbers.

CME SDR – FX

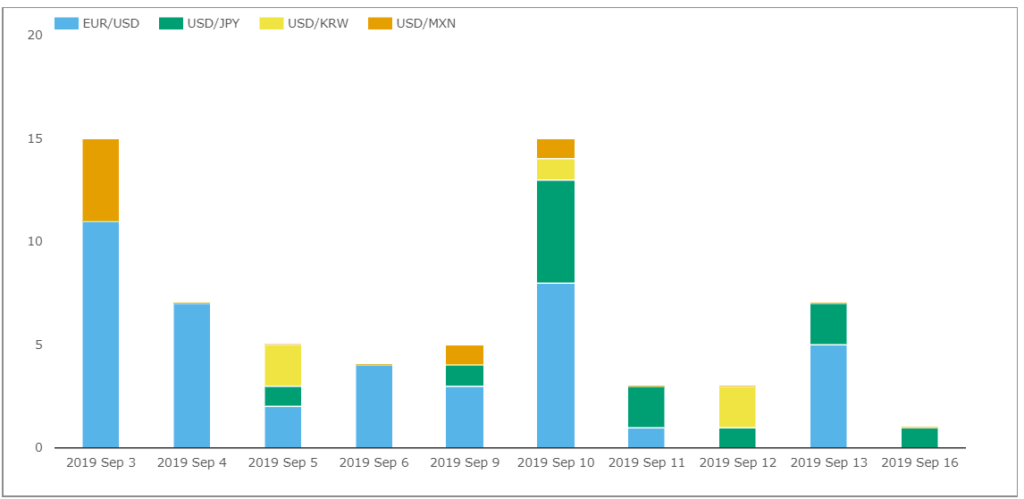

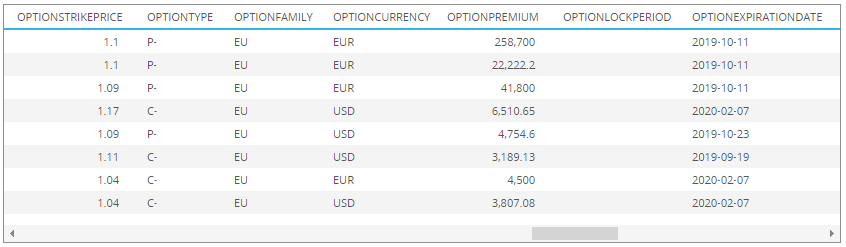

As well as Rates, the CME SDR also has FX and of particular interest to us both FX Options and Non-Deliverable Forwards.

Showing up to 15 trades a day in the four selected currency pairs, so again low numbers, but interesting data nonetheless, particularly if we drill-down to the trades to see the strikes and premiums.

The End

That’s it for today.

We are pleased to enhance SDRView to include CME SDR.

If you are interested in this data, please register for a free trial here.

One day we hope to see trade level transparency in EU and Asian jurisdictions.

Its only been 5 years and counting….

Surely equivalence is an important objective.