Following on from my earlier articles looking at European Trade Reporting and OTC Derivatives Reporting in Japan, I thought I would look at other jurisdictions starting with Canada.

Canadian reporting came into force for Dealers on 31 October 2014 and for Non-Dealers will do so on 30 June 2015.

Overview of Requirements

Key points:

- OTC Derivatives in Credit, Commodities, Equity, FX and Interest Rates (so excludes Exchange Traded)

- One side is required to report (same as the US)

- Dealers started to report new trades from 31 October 2014

- Pre-existing trades are required to be reported no later than 30 April 2015

- Public dissemination of aggregate data on a periodic frequency

- Public dissemination of transaction level data on a T+1 basis for Dealers and T+2 for Others

DTCC GTR is the approved Canadian Repository and their website provides much more detail.

Public dissemination of transaction data

Regular readers of the Clarus Blog will know that transaction level public dissemination is the most interesting data as it includes information on both price, volume and time of execution.

The good news is that Canadian regulators are requiring this to be made public; unlike the current status in Europe, Japan and other jurisdictions.

The bad news is that it is made public at the end of the next business day (T+1) for Dealer trades and the second day (T+2) for Non-Dealers. This is a shame as it constrains the value of price discovery and transparency. The only upside to this is that as a consequence there is no need for block rules, capped sizes and rounding of notionals, which means that the real size of trades will be reported (unlike the US where this is never disclosed in the public dissemination).

However we will have to wait till April 30, 2015 (or later?) to start seeing this public data.

So I will make a note to check back then and move swiftly on to what is available now.

[Update 12 May 2015: The date for public dissemination of transaction level data has been delayed by 15 months to July 29, 2016, “in order to permit study of the Canadian over-the-counter (OTC) derivatives market data and development of publication delay rules designed to maintain the anonymity of counterparties”. More details can be found at Ontario Securities Commission.]

[Update: This was further delayed and the new date is now 16 Jan 2017]

Public Aggregate Data

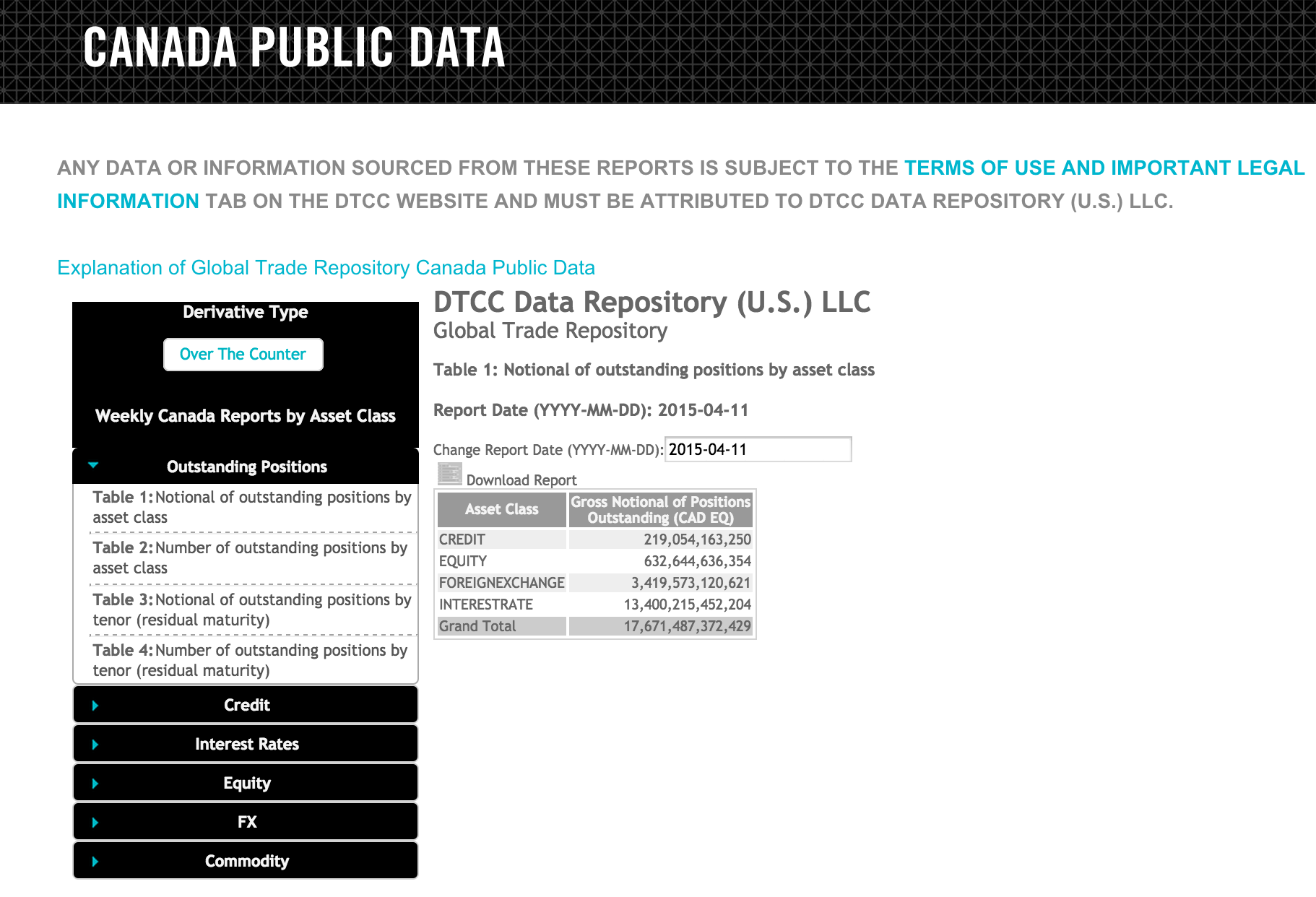

The DTCC GTR-Canada website provides a link to Canada Public Reports, as shown below.

The most recent data today is as of April 11, 2015, so a week old, which suggests the data is published weekly with a weeks lag. There are 15 different reports, which are described in the Explanation document found on the above page.

Lets take a look at What the Data Shows.

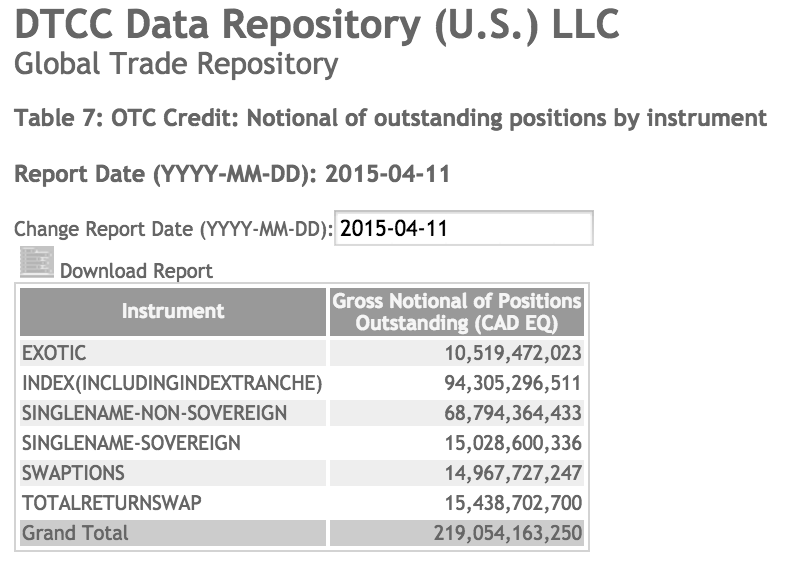

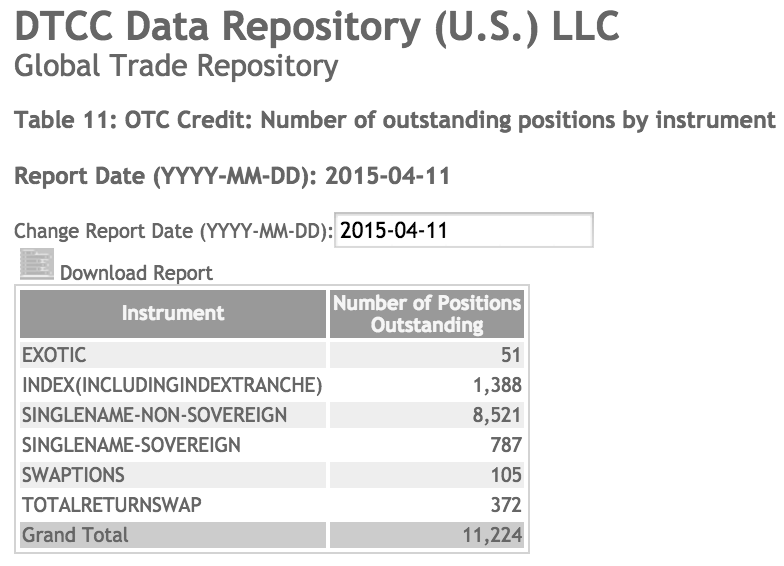

Credit

Both Index and Single-name volume is available, unlike the US where we are still waiting for the SEC regulated implementation of single-name public dissemination. Lets look at April 11 data, first Gross Notional and then Positions/Trades.

Which show that:

- Index has the highest Gross Notional with 94 billion CAD$ from 1,388 positions.

- Single name Non-Sovereign is next with 68 billion CAD$ from 8,521 positions.

- Single name Sovereign has 15 billion CAD$ from 787 positions

- Exotic, Swaptions, Total Return Swap are the rest.

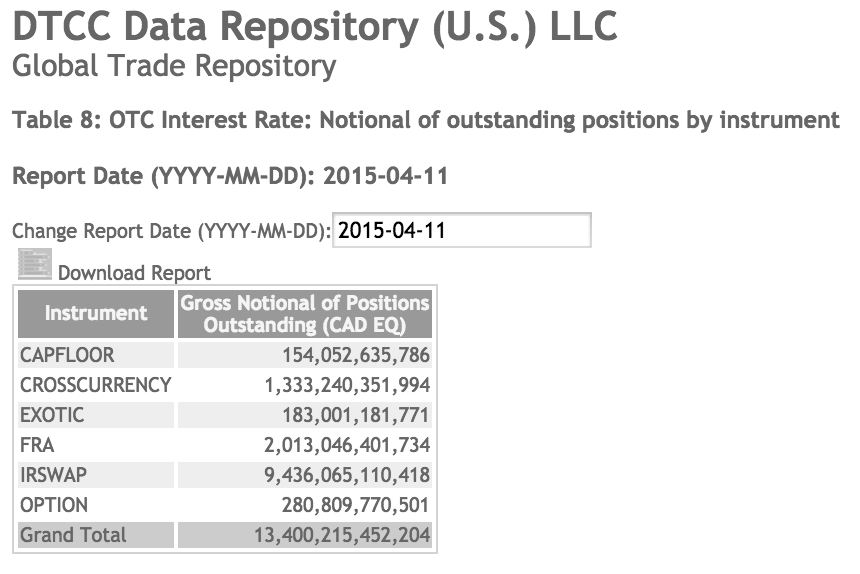

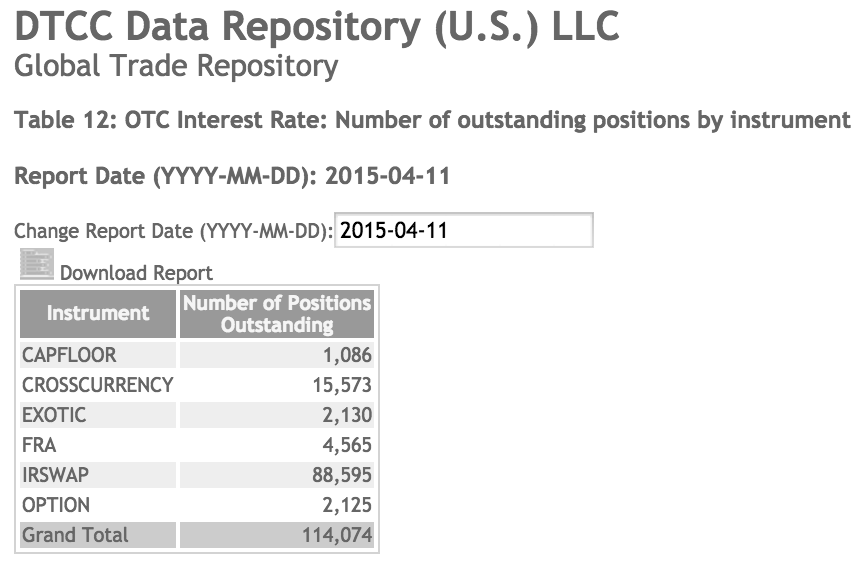

Interest Rates

Lets now look at the two available reports for Interest Rates.

Which show that:

- IR Swap are the largest with 9 trillion CAD$ and 88,595 trades

- FRAs are next with 2 trillion CAD$ and 4,565 trades

- Cross Currency Swaps are 1.3 trillion CAD$ and 15,573 trades

- CapFloors, Exotic and Options make up the rest

It would be more useful if we had Currency and Maturity breakdowns, so will we can assume that the majority of volume is CAD, it would have been useful to know how much is USD, how much others and for Cross Currency which currency pairs make up the numbers.

Another case of as soon as data is aggregates, we lose useful information, even more so if asset class specific aggregation dimensions are not used.

What else can we glean from the data?

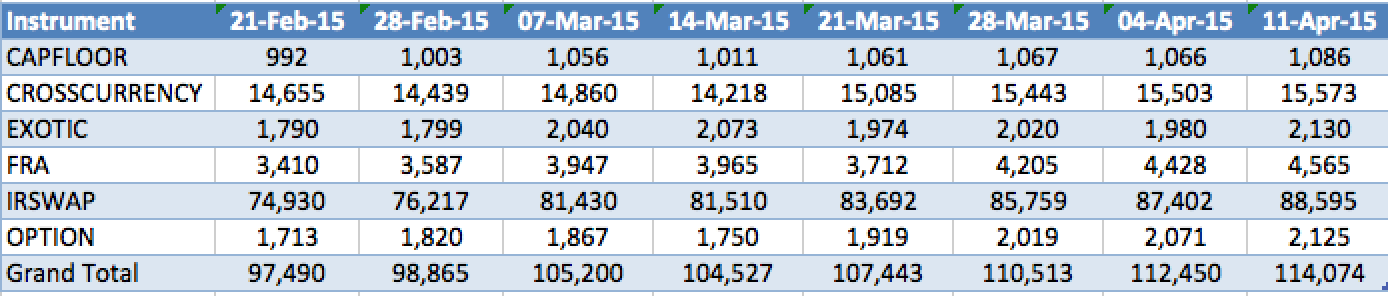

Well we have weekly history going back to the start of the year. Exporting this and looking at the trend could be interesting.

First the number of trades at the end of each week for the past 8 weeks.

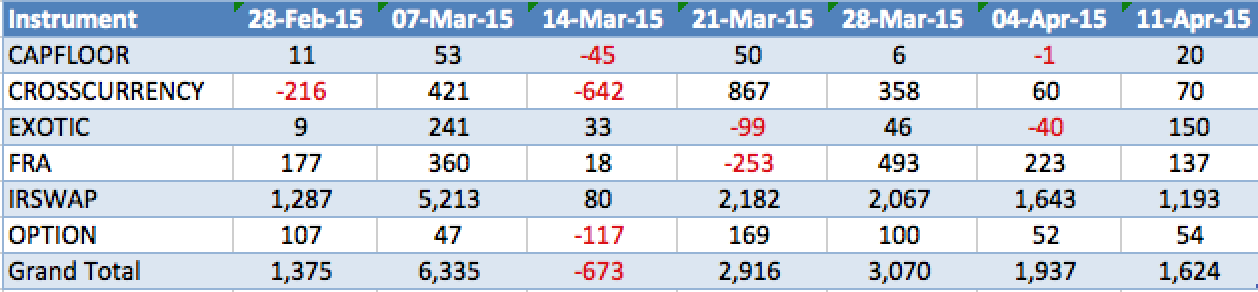

Then the change in trade counts for each week.

Showing that:

- IRSwap trade counts vary from 80 to 5,213, which is odd

- But if we assume a reporting glitch where 14 Mar trades have ended up in 7 Mar

- Then we can say IRSwap trades range from 1,200 to 2,200 per week

- FRA we know that 21-Mar is the IMM week, so explains the drop in trades

- FRA trades range from 140 to 360 a week

- Cross Currency also shows odd drops in 28 Feb and 14 Mar weeks, might be maturing trades

- Cross Currency volumes vary a lot from 60 to 860

We could produce similar tables for Gross Notional, which would also show drops in gross notional in the same cells as drops in trade count above. It woudl also suggest that much pre-existing trades have been reported (back-loaded) as just extrapolating the weekly volume of 1,200 to 2,200 IRSwaps back to 31 October is not going to get us to 88,000 trades.

However I will leave it at that and suffice to say that there is a reasonable volume of trades being reported each week.

And if the bulk of these are CAD then certainly far higher volume than we see in US SDRs for CAD. For the same period the US SDR weekly volume for CAD in IR Swap trades is in the range is 243 to 569, there is no FRA volume and Cross Currency Swaps range is 8 to 32.

So the Canadian Public Reports certainly add a meaningful amount of data to that available in the US.

FX, Equity and Commodity

We could look at the similar reports for these, but I will leave that to those of you that are interested to do yourself.

Just go to DTCC GTR Canada Public Reports.

For me, I will wait till April 30 or May 1 and check back to see the transaction level data.

Summary

The DTCC GTR Trade Repository is live in Canada.

Dealers have been reporting since 31 Oct 2014 and Non-Dealers will report from 30 Jun 2015.

Transaction level public dissemination will start soon.

Aggregate weekly public reports have been published since Jan 2015

These show that a large number of trades and gross notional is reported each week.

The reports lack useful dimensions like Currency, but nonetheless show a tantalising glimpse into OTC Derivatives Data.

Roll on 1 May 2015.