On the 27th February 2020, the UK FCA wrote to asset management firms to emphasise the need to prepare for LIBOR to likely become unusable after December 2021. This extended previous ‘Dear CEO’ letters from 2018 to major banks and insurers and was designed to ensure firms are well prepared for LIBOR cessation.

As we move towards the likely end date for LIBOR in December 2021, the markets are still trading in LIBOR derivatives. Recent Clarus blogs, Spotlight on RFR Swaps and Trading RFRs have shown the slow progress from LIBOR to RFRs.

The issue is most problematic in maturities greater than two years where cleared derivatives show RFR trading as a small percentage of LIBOR. Currently SONIA trading is around 20 – 25% of GBP LIBOR, while SOFR is almost negligible compared with USD LIBOR.

Contents of the ‘Dear CEO’ Letter

The letter contained a number of very clear steps the FCA expects asset management firms to address. And to just to make sure the message is clear, the FCA includes a paragraph in bold type about the urgency of acting on the points in the letter! The steps are:

Priorities and milestones

Firms are encouraged to get clear priorities for changes to products and systems which need to reference RFRs rather than LIBOR. And to have milestones to achieve this well before December 2021.

Products and services

Transition products and services from LIBOR to RFRs to ensure they are ‘fit for purpose’ before the end of LIBOR.

Governance and planning

The Board should have oversight of the transition process and make certain that there are sufficient resources available. The Board should also seek support and challenge from 2nd and 3rd lines of defence.

Replacing LIBOR with RFRs in current and new products

Be proactive in locating and replacing references to LIBOR in products, return benchmarks and constitutional documents.

Investing on client’s behalf

Third party funds and/or accounts will have to be managed. It is imperative that firms ensure these third parties are well prepared for LIBOR cessation.

Conflicts of interest

Firms must manage their conflicts of interest especially in how they represent changes to portfolios and returns to investors.

This is a very short summary of the letter: it is worth a full read if you can spare the time.

Fiduciary Duties

The letter and the points above are very clear about the expectations of FCA in representing the interests of investors. The obligations of the asset management firms are of great interest to the FCA.

Apart from a programme of work to manage the transition from LIBOR to RFRs, firms are expected to pay close attention to their fiduciary duties to their investors. And the FCA makes it very clear that this is a board-level responsibility.

These duties include proper management of exposures, looking after the interests of the investors and clear communication with all impacted parties (internal and external). There are many facets of fiduciary duties but I will look at two in the next section: transition of existing derivative exposures and investing in products linked to RFRs.

Two examples of fiduciary duties

As markets inevitably transition from LIBOR to RFRs, how should a firm value and/or revalue products to ensure investors are not disadvantaged? And how are firms to ‘prove’ that they have indeed taken all due care to look after the interests of their clients?

Cash products generally have a price, clean or dirty. Products with the same basic details but referencing LIBOR or RFRs can be readily compared with each other simply by looking at the published price.

However, derivatives are somewhat more challenging as they typically do not have published prices. Firms will need another way to value the before and after trades.

The new benchmarks could include compounded, setting in arrears RFRs (with lockouts or lookbacks), Term RFRs or other variants mentioned in a previous blog. These options need to be assessed and valued to ensure client interests are protected.

Valuation of existing derivatives before and after the changes

It is likely many asset management firms will need to amend derivative transactions to move from LIBOR references to new benchmarks. The existing derivatives need to be replaced with new ones with the same value.

Valuation of new derivatives

New types of derivatives will certainly be required to replace the LIBOR versions. Again, there are options for the RFR references which will need to be valued.

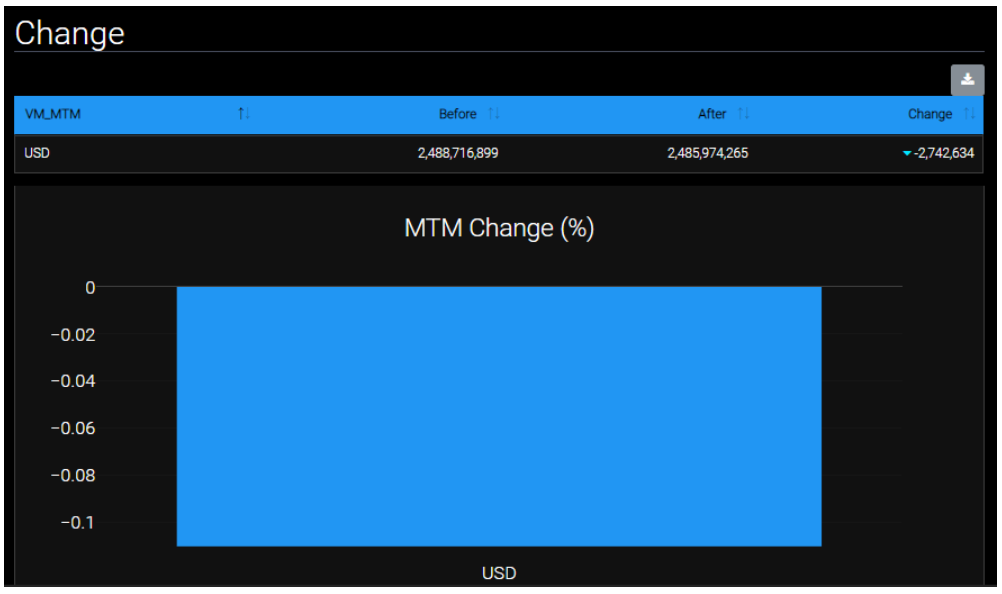

Being able to value the changes is extremely important but proving this is correct is equally important.

This where Clarus IBOR Transition tools can help asset managers with valuations and scenarios.

Fiduciary obligations and Clarus Tools

The fiduciary obligations are extremely important when dealing with client money. Not only should an asset manager take due care and diligence with assets but they also need to make sure valuations and systems are calculating accurate returns.

Clarus IBOR Transition tools can assist with the valuation of derivatives for transition or new trade, they offer asset managers an independent and efficient way to show valuations and not rely on counterparty valuations alone.

The independent derivative valuation will add to the ability to show high levels of fiduciary care and preserve the value of client investments. Whether conventions are consistent or remain varied, Clarus tools are able to value a full range of scenarios and is a valuable tool.

Summary

The transition form LIBOR to RFRs is starting in earnest. Regulators are urging all market participants to identify risks and have programmes of work in place to manage this transition in a timely and low-risk manner.

Asset managers have additional risks because they are the managers of client money. Fiduciary duties oblige them to make sure they act in the investor’s interest at all times.

Clarus IBOR Transition tools offers an efficient and simple way to check derivative valuations independently. The service shows valuations and scenarios so that can greatly assist asset managers truly look after client money.