Today we put out the press release, Clarus Financial Technology releases IBOR Transition Management Tools and in this blog I wanted to provide more details on our offering. Before I do that, another point to note is that we recently authored a whitepaper with our friends at Finastra, titled “IBOR Transition Made Simple“, which is available for download here and well worth a read, (after you have finished reading this blog of-course).

Background

As our regular readers will know, we have written many articles on IBOR reform, starting in May 2017 with Euribor Reform and Sonia Reform, as well as the Sep 2017 article, Libor Reform – What You Need to Know. Since then we have published sixty articles on the topic (see Index/Fix), responded to industry consultations, published Term RFRs, attended conferences, spoken on panels and held discussions with many participants.

After all that, one can expect that we should know a fair amount about IBOR Transition.

That experience, coupled with our core expertise in innovative software and data products, led to today’s release of a set of tools for IBOR Transition Management. Let’s look at a few of these.

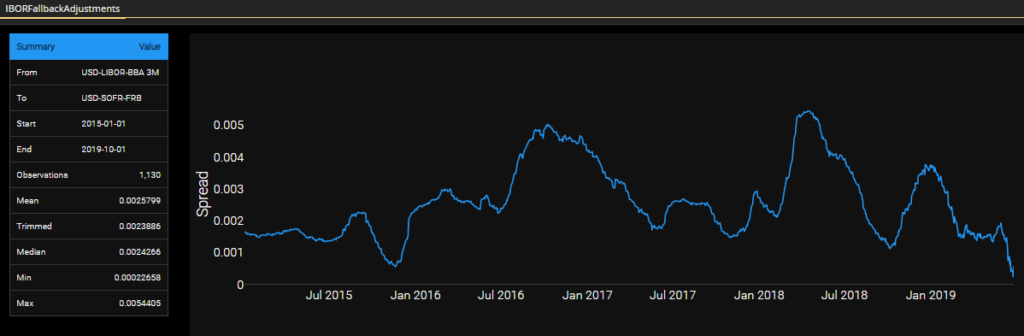

IBOR Fallback Adjustments

An App to calculate estimates for IBOR Fallback Term and Spread Adjustments, super useful and even more so as the industry responds to the ISDA Consultation on Final Parameters and waits for the final specification.

Showing USD LIBOR 3M with a mean spread adjustment of 25.8 bps and a median of 24.3 bps for the historical period starting Jan 1, 2015 and ending October 1, 2019.

Users can select the currency and IBOR tenor of interest (e.g. GBP LIBOR 6M), the historical period and get back statistical measures such as median or trimmed mean, along with the full time series data.

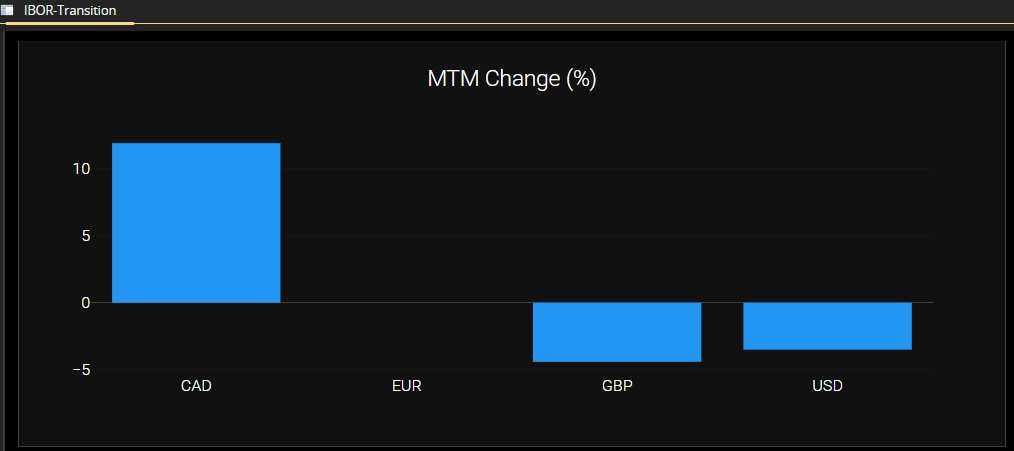

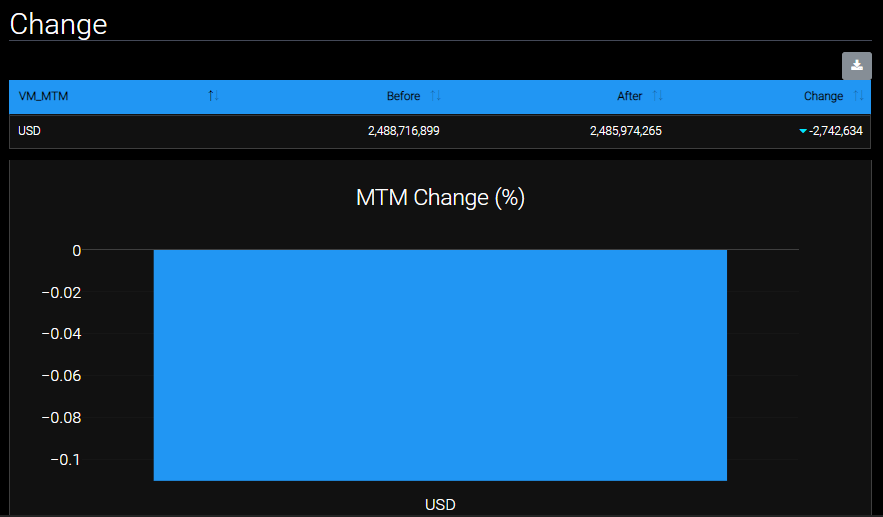

Valuation Impacts

An App to upload your trade or portfolio, cleared or bi-lateral, in a choice of of industry standard formats and calculate the change in market to market valuation resulting from IBOR Fallbacks.

Showing the change in MTM expressed as a percentage change for each currency in the portfolio on the adoption of IBOR Fallbacks on a future cessation event.

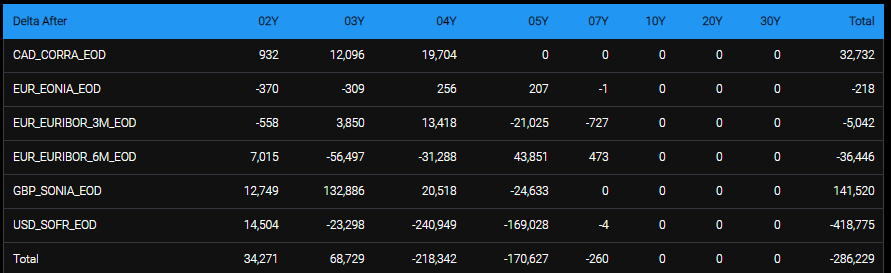

Risk Impacts

And how interest rate risk for a trade or portfolio will change from IBOR to RFR curves.

Showing IRDelta risk in major buckets for a sample portfolio; CAD, GBP and USD all now projected onto single RFR curves.

SOFR Discounting

While IBOR discontinuation is not expected before Jan 1, 2022, well before that in 3Q 2020, we will see cleared Swaps at CME, LCH and other CCPs, move from USD FedFunds to SOFR discounting. Closely or at the same time, followed by bi-lateral derivatives (e.g. Swaptions and Cross Currency Swaps) .

We have an App for that.

Well the same App, different mode.

Transition Tools

It almost goes without saying that transition tools cannot require projects with many years of implementation effort, as by the time they are working it will be far too late to get any value. I do feel I have to point this out to those considering upgrading in-house or vendor systems to implement a new module….. don’t say you were not warned.

Our Apps, are deployed on AWS Cloud, offer many industry standard formats to upload data, we provide the reference and historical data and support you to get going on day one . And when these tools have served their purpose and the transition is done, we expect them to be discarded in favour of BAU production software.

Apps and APIs

As well as Apps, we provide APIs for firms that want to integrate and customise for their own needs. Available in Excel or python, these APIs make it easy to build specific views or create easy to understand charts, tables and factual data to discuss with customers. Customer outreach is a key part of IBOR Transition and obtaining fair outcomes as agreements are changed is crucial to good conduct.

There is much more on this topic, but that is a blog for another day.

That’s It

That is all I have time for today.

To learn more, please contact us to schedule a demo.

And don’t forget to download the whitepaper.