2020 is shaping up to be an important year for the development of markets in SONIA and SOFR. Recently on 21st November in a speech the FCA outlined plans to accelerate development of SONIA markets during 2020.

Although plans are well advanced, the markets are still developing liquidity in longer-dated derivatives. I recently looked at SONIA and SOFR markets to assess the growth in the notional volumes with maturities greater than two years.

Significant growth in the longer maturities can imply the involvement of ‘end users’ or buy-side participants. For example, debt issuers hedging back to floating rates or loans hedging into fixed rates tend to use derivatives with maturities longer than two years. At this time, it appears more end users are staying with LIBOR as a reference.

I still expect the SONIA and SOFR markets to expand liquidity in 2020, but what does this mean for the end user?

Using the new reference rates

Making the change from LIBOR to a new reference rate is not a trivial exercise. This will take planning and probably involve some changes to systems and processes to accommodate the new rates.

SONIA and SOFR (and equivalent rates in many other currencies) appear likely to offer two options for users: compounded, setting in arrears (as is used in OIS markets now) or a term rate setting in advance (as does LIBOR currently).

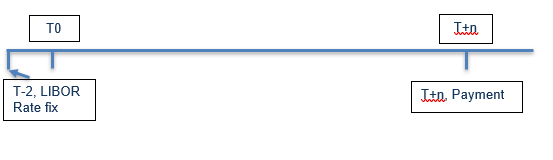

LIBOR rate fixing and cashflows with which we are familiar typically look like this:

The ARRC has published a guide to SOFR where a number of options for compounding/averaging methods are described in Table 3 of the publication.

1. Compounded or averaged, setting in arrears

This option is commonly used in OIS derivatives and has been used recently in some debt issues.

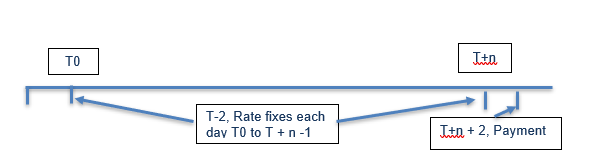

The rate, e.g. SONIA, published each day for the relevant period is compounded or averaged to create a discount factor. The simple interest rate is then calculated from the discount factor and this is used for the floating rate where LIBOR would have been used previously.

The following diagram shows one variant of the compounding/ averaging where the rates are fixed each day during the period and the payment is delayed 2 days.

This is common in OIS trades while other methods are often used in cash products.

Other variants such as ‘look-backs’ and ‘lock-outs’ (and the reasons for using them) are explained very well in the ARRC paper.

2. Term RFRs

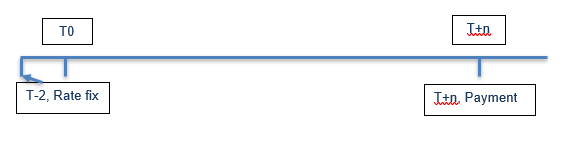

Term RFRs where the rate is known at the start of the relevant period (like LIBOR) are under development in many currencies.

For example, in the UK several parties have proposed solutions for creating the SONIA Term RFR to the BoE sterling working group. Also, the ECB working group has published a list of 5 responses to their request for expressions of interest.

The Term RFR diagram below looks very similar to the LIBOR diagram above in rate fixing and payments as follows:

It is highly likely that the two options above, with their variants, will be used by derivative and cash markets in the future.

What is the ‘spread’

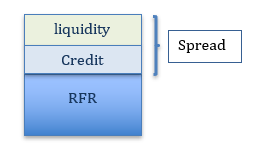

The ‘spread’ is often referred to when looking at the difference between LIBOR and RFRs. It is simply the difference between the RFR and LIBOR over the relevant period.

LIBOR includes credit and liquidity spreads where the RFR (i.e. Risk Free Rate) does not. The additional basis points for credit and/or liquidity are called the ‘spread’.

When comparing rates referencing LIBOR and RFRs it is important to recognize the spread in both pricing and valuation.

Choices for new trades

As liquidity increases in RFR markets, the choices for new derivative or cash trades can reference:

- LIBOR – This is still an option but robust fallbacks to accommodate the very likely cessation of LIBOR are essential inclusions.

- Compounded RFR – Compounded, setting and settling in arrears (i.e. at the end of each relevant period).

- Averaged RFR – Averaged, setting and settling in arrears (i.e. at the end of each relevant period).

- Term RFR (when available) – Setting at the start of the relevant period and settling at the end of that period similarly to LIBOR.

All options have their merits and challenges!

Liquidity is expected to increase in RFR trading at the expense of LIBOR trading by the end of 2021. Buy-side participants will likely wish to use the most liquid markets for new trades which may mean a shift to the RFR options above.

Choices for existing trades

Existing, or legacy, trades have the same options as for new trades. However, in most cases the fallbacks in case LIBOR is unavailable (e.g. it ceases to publish) have to be replaced by more robust arrangements.

Recently Chris Barnes wrote on this subject so I will not go into detail on this complex area in this blog.

Suffice to say, existing trades will need to be amended and there is a likelihood there may be a valuation difference whichever option you take.

How Microservices can help

Clarus Microservices are a very useful tool to assist with decisions for new and existing trades. The transition from LIBOR to RFRs either directly or via a fallback mechanism can be complex which is where Microservices can help.

1. Valuation

Whichever option you take for new and existing trades, there will likely be a difference in the rate and valuation. These can be easily compared in Microservices for either RFR option, using fallbacks or changing the fallbacks in existing trades.

2. Scenarios

The valuation of the different options will change over the life of the trade and the relationship could vary (as it has in the past).

Microservices will give you the ability to look at different scenarios based on historical performance (averages and extremes).

3. Independence

Since Microservices analytics and rates are independent they act as a very effective way to check your own systems and those of your counterparties.

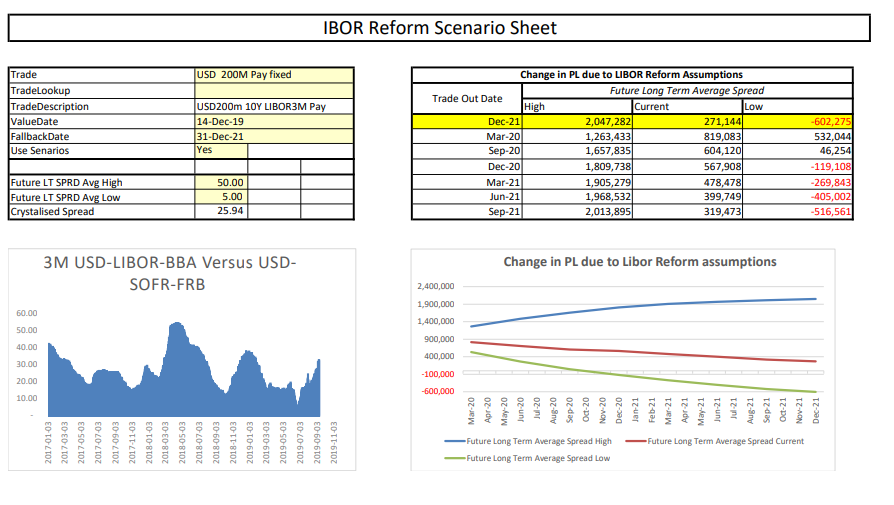

Using Clarus Microservices we can a spreadsheet to value the fallbacks and different scenarios.

This is for a new interest rate swap in USD for 10 years and $200 million. The panel on the top right shows the forward valuations graphed directly below for different scenarios added in the top left panel

The bottom left chat is the historical LIBOR/SOFR spread.

Of course, you can easily expand this method to add RFRs, different assumptions for LIBOR cessation dates and other currencies. Likewise, you can build up the scenarios to your own specifications.

And it can all be done in a spreadsheet, scripting languages like python or other applications!

Summary

As we approach 2022 when LIBOR is expected to cease publication, the markets will evolve to use new benchmarks like RFRs. As new markets develop in 2020 and 2021 buy-side participants will have to adapt.

This creates problems and opportunities for amending existing trades as well as making decisions about new trades. A well-prepared and informed firm will likely make better decisions across the options for trades as well as the timing.

Clarus Microservices offers an accessible and straightforward way to help in these decisions.

Contact us to find out how to use them in your IBOR Transition project.