In November I looked at the risk implications of a LIBOR pre-cessation announcement which was widely expected in December 2020. Basis markets such as SOFR/USD LIBOR and SONIA/GBP LIBOR clearly priced the spread to be fixed at the announcement in December (i.e. over the next month or so) and that the fallbacks would take effect in derivatives after 31 December 2021.

How wrong was that assumption! On 18 November 2020 there were a number of announcements by ICE Benchmarks Administration (IBA), FCA, FED and ISDA. This was followed up by another series of announcements by all four on 30 November. These announcements are covered in Chris Barnes’ recent blog. I also recommend you take a look at the ISDA webinar from 4 December (replay or transcript are both great) which does a fine job of explaining the potential sequence of events.

In short, IBA will consult on the future of LIBOR in two parts: USD LIBOR and the rest. They released the consultation on 4 December which proposes the discontinuation of all LIBORs except USD with the last publication date being 31 December 2021.

USD LIBOR would continue (and importantly be representative of the market) with last publication on 30 June 2023. However, IBA are proposing to discontinue 1-week and 2-month USD LIBOR on 31 December 2021 in line with the other currencies.

USD basis markets reacted quickly to the news that the expected date for the spread to be set would be later than previously expected. The SOFR/LIBOR basis narrowed as more of the lower, future-priced spreads were included in the five-year median as calculated by Bloomberg.

This nasty case of whiplash reversed the move out from June 2020 when the pre-cessation announcement expectations were brought forward to December 2020.

ISDA triggers

The ISDA Definitions will include the concept of the Fallback Cessation Event.

The ISDA ‘Fallback Cessation Event’ is based on three basic triggers:

- a public statement by or on behalf of the administrator announcing they will cease to provide the benchmark (the IBA announcement);

- a public statement by the regulatory supervisor (FCA for LIBOR), the currency central bank (e.g. FED for USD), a resolution authority with jurisdiction over the administrator or a court or resolution authority with similar insolvency or resolution over the administrator that states the administrator has or will cease publication of the benchmark; or

- a public statement that the benchmark is no longer representative of the underlying market (the pre-cessation announcement).

Any of these options could trigger a benchmark cessation event.

But a word of warning: not all contracts and trades include all or some of these triggers.

The new triggers will apply to new derivatives referencing the ISDA 2006 Definitions from the effective date of the Supplement (25 January 2021) and legacy derivatives if counterparties adhere to the Protocol (or agree bilaterally).

But many loans, securitisations, debt issues etc. may not have these triggers and may not move to fallbacks at the same time as the ISDA-referencing contracts.

Care needs to be exercised to fully understand the individual risks and hedges to understand the actual triggers and fallbacks!

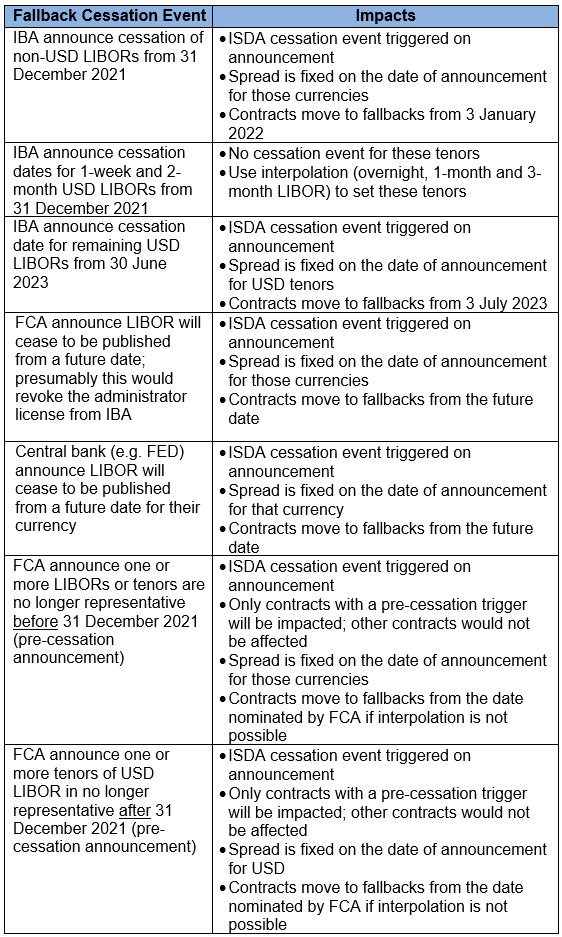

Cessation or pre-cessation annoucement

We now have a few different options for 2021 which revolve around the actual announcements and potentially the order in which they occur.

Firstly, let’s look at the possible events and announcements which could trigger the ISDA Fallback Cessation Event:

Note: FCA has continuing obligations to review LIBOR so may make a pre-cessation announcement after 31 December 2021 and before 30 June 2023 if they conclude USD LIBOR is no longer representative.

Implications of different triggers

As noted above, these are the ISDA triggers and apply only to new transactions from 25 January 2021 and existing transactions where agreed bilaterally or via Protocol adherence.

When any of the announcements or events above are made, derivatives with those inclusions will move to fallbacks then or at a future, nominated date.

But what happens to the trades without these triggers? In some circumstances where the benchmark is still published then they could continue to reference it. For example, a pre-cessation announcement would trigger the derivative but LIBOR could still be published and used by some transactions.

However, a cessation announcement based on points 1 and 2 above would logically result in non-publication and therefore trigger more contracts to fallbacks.

The actual announcement and the entity making that announcement is actually very important. The ‘cease to provide’ version has wider impacts than the ‘no longer representative’ one and the two scenarios should be considered separately per contract.

As we see, the order of announcements could have quite complex implications for different products and contracts.

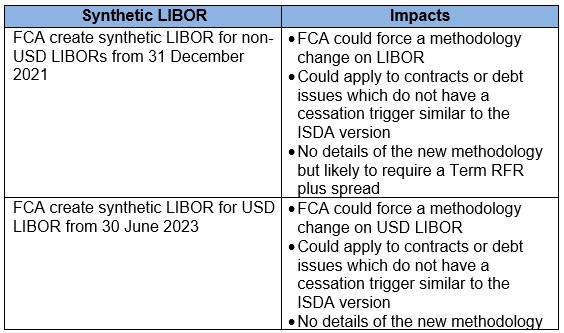

Synthetic LIBOR

If any of the Fallback Cessation Events are triggered then the implications for derivatives are quite clear. But if LIBOR is still published in some form, then the ‘tough legacy’ contracts may continue on as before.

If the ‘cease to provide’ announcement is made but FCA announce a change in methodology, i.e. synthetic LIBOR, to be provided on the same ticker then presumably some contracts could continue simply because they do not include the announcement as a trigger.

For example, the derivative would move to the fallback on a pre-cessation announcement but LIBOR could change to a different methodology and continue to publish. This would allow some trades or contracts to continue referencing LIBOR.

Synthetic LIBOR announcements could look like this:

The actual outcome is clear but the path to a synthetic LIBOR is not obvious. If IBA make an announcement to cease providing LIBOR from a certain date but the rate is still on the same reference pages (synthetic LIBOR) then has LIBOR really ceased to be published?

The actual process could be problematic and create outcome differences for some participants and possible disadvantage for a few.

This appears to be the main point in the UK and USA which may require some legislative changes to avoid disputes of this type.

Does synthetic LIBOR equal fallbacks?

The answer is probably no.

The current proposal for synthetic LIBOR is to use the Term RFR plus a spread to create the rate for each tenor can, and probably will, have a different economic outcome to a fallback based on the Bloomberg Rule Book.

Firstly, the Term RFR is unlikely to be the same as the compounded RFR unless the forward rates used to calculate the Term RFR just happen to equal the actual rates. Clearly this is not always the case otherwise an OIS done at midpoint would settle at zero every time – this is not the market experience.

Secondly, the spread will need to be different. The Bloomberg fallback spreads are calculated from the LIBOR minus the fallback whereas the spread for the synthetic LIBOR will need to be LIBOR minus Term RFR: these are different. Also, the Term RFR five-year history set which is needed for the calculation is not available at this time.

A second word or warning: a synthetic LIBOR will probably not have the same outcome as a fallback to compounded LIBOR and definitely not the same as the original LIBOR it replaced.

Is this a problem for users? Perhaps it will create winners and losers which may depend on the exact language in contracts and how it applies fallbacks.

Summary

The LIBOR transition situation is changing as we get closer to 31 December 2021. New announcements and possible solutions to the complex world of LIBOR will very likely continue changing market pricing and positions for market participants.

The development of RFR markets is still challenged as shown in the most recent ISDA-Clarus RFR Adoption Indicator. Moving from LIBOR to RFRs needs to accelerate soon to minimize disruption for markets.

Tough legacy trades are still problematic and perhaps synthetic LIBOR is a solution. But be aware a synthetic LIBOR may not be identical to either LIBOR or the fallbacks.

I have summarized a few of the points from this blog below:

- The possible announcements and their implications is complex and important to understand;

- These announcements could occur early 2021 and will have immediate effects (e.g. when the spread is set);

- The order and wording of the announcements will be critical to the impact on your firm;

- Exact contract language is critical to document and understand so you can react quickly;

- Synthetic LIBOR may apply but will likely not equal fallbacks;

- Manage your exposures to the spreads; and

- Beware the cliff

This will be a complex time for all of us. Valuations and risk measures will be challenged as the impacts of announcements change contractual outcomes.

The announcements and the order in which they are made (or not made) could be a critical determinant in performance of contracts and trades.

And as always, Clarus CHARM, Microservices and the Clarus Data all provide a necessary toolkit for managing your exposures.