Following my blog on CME and LCH: What Happened on May 19 and Jun 12, I wanted to re-visit the data now that we have another week of published volumes.

Weekly Volumes

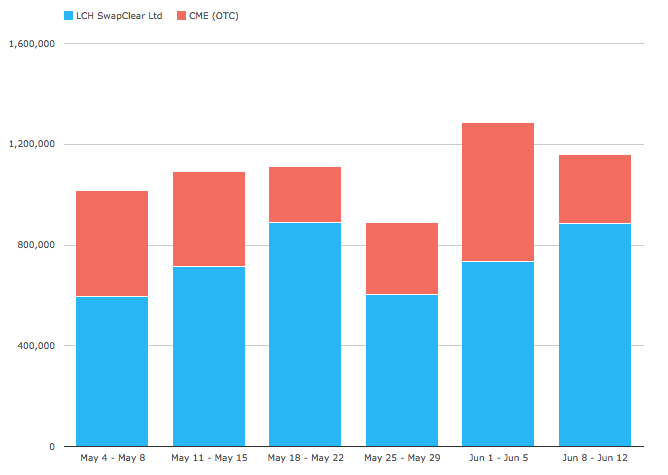

Using CCPView lets look at weekly volumes of gross notional for just USD IRS for the past 6 weeks and compare CME IRS Volumes with LCH SwapClear Volumes (All and not just Client).

Showing that:

- Jun 8-12 volume was $1.16 trillion

- Close to the Jun 1-5 volume of $1.29 trillion

- And higher than each of the first three weeks in May.

- Jun 9-12 shows CME volume is down and LCH volume up

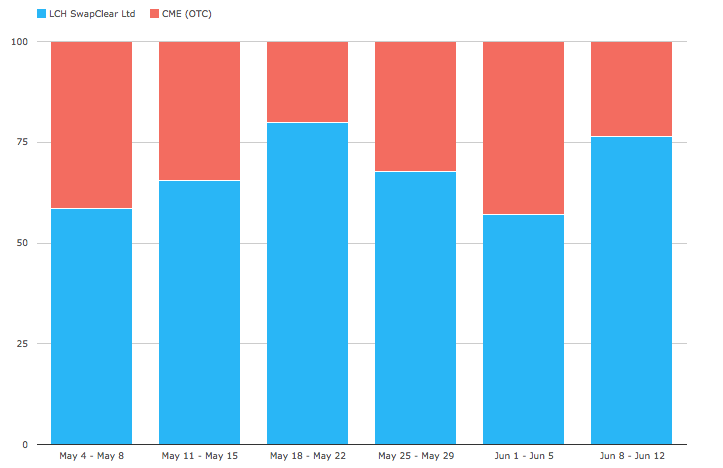

The LCH share is significantly higher, which becomes evident if we look at a chart and table of percentage share.

Showing that:

- Jun 8-12, CME Share is 24% vs LCH 76%

- This is the second lowest CME share in our period

- May 18-22 was the lowest

- The average share over the period is CME 33% and LCH 67%

Meaning that the uptick in CME share in the week Jun 1-5, has reversed back down and is close to the low of May 18-22.

Daily Volumes

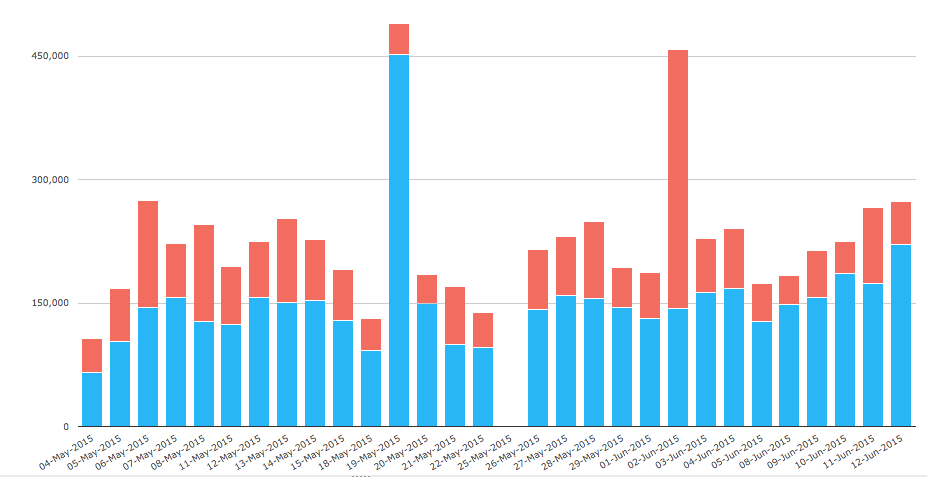

If we now switch from Weekly to Daily volumes, we get an interesting view.

Showing:

- The spike in volumes on 19 May at LCH (blue)

- The spike in volumes on 2 Jun at CME (red)

- (Both covered in last weeks blog)

- And a clear trend showing LCH gaining share over the period

- Ignoring the spike days, CME low daily share is 17.4% and high 48.3%

- The 17.4% low is on 10 Jun

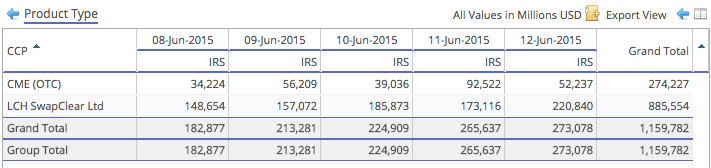

Looking just at the numbers for last week.

We see LCH show consistently higher volume each day, with no single day dominating; unlike the week of May 18-22.

What of the Basis Spread?

Lets take a quick look on what has happened to the CME LCH Basis by looking at todays Tradition page.

Which looks like a tightening in USD and EUR but a widening in GBP compared to 26 May.

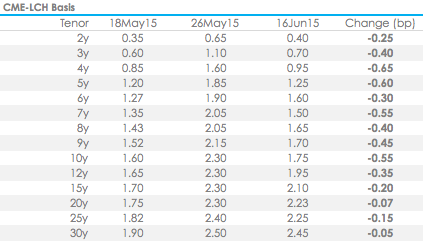

Lets compare USD.

Showing:

- A fall across all tenors compared to 26 May

- 5Y and below are back close to 18 May figures

- 10Y is down from 2.30 to 1.75

- 30Y is almost un-changed

- (Worth re-reading Chris’s blog on Term Structure)

So a tightening of the spread but 1.75bp at 10Y and 2.45bp at 30Y are certainly very significant.

Client Clearing Volumes

As LCH break-out Client Volumes from All Volumes,lets look at whether this shed lights on a change in where Clients are choosing to clear their USD Swaps. (While CME does not break out its figures, we assume that vast majority of its volume is Client).

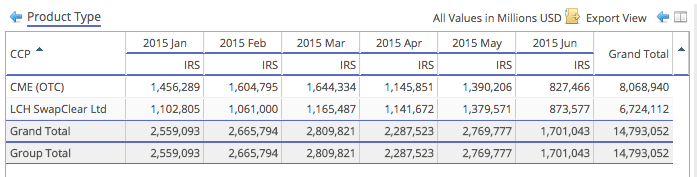

Lets use CCPView to look at monthly volumes for USD IRS since 4 Jan 2015.

Showing very clearly that CME volume in the first 3 months were a clear majority and the share between CME and LCH was consistent mont on month.

Then April and May show parity between CME and LCH, while June shows LCH slightly ahead.

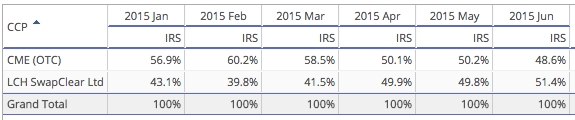

The same numbers shown as percentages:

The 1Q2015 60% to 40% share in CME’s favour now running at 49% to 51% in LCH’s favour.

Meaning that CME has lost 10% of market share in Q2 and LCH has gained 10%.

While June 17 is an IMM Date and likely to introduce noise due to MAC and IMM Rolls, it will be very interesting to see where June volumes end up.

And even more to see how July and August develop.

Particularly as we get closer to the first Federal Reserve Rate hike, where will Clients choose to clear their Swaps?

Only time (and CCPView) will tell.

Make sure to subscribe to our blog to stay informed.