We analyse the CME-LCH Basis volumes by tenor and look at what the forward curve implies for prices in the future. There are no signs of normalisation trades in the market, with the basis widening over the past week. We suggest some thoughts as to how this may play out for other Currencies and other CCPs.

Amir did a great job looking at the fundamentals of the fast-evolving CCP Basis market last week. It’s clearly a hot topic, so let’s combine some of the data we didn’t use last week with price information from TradX to show how the market expects the basis to evolve over time.

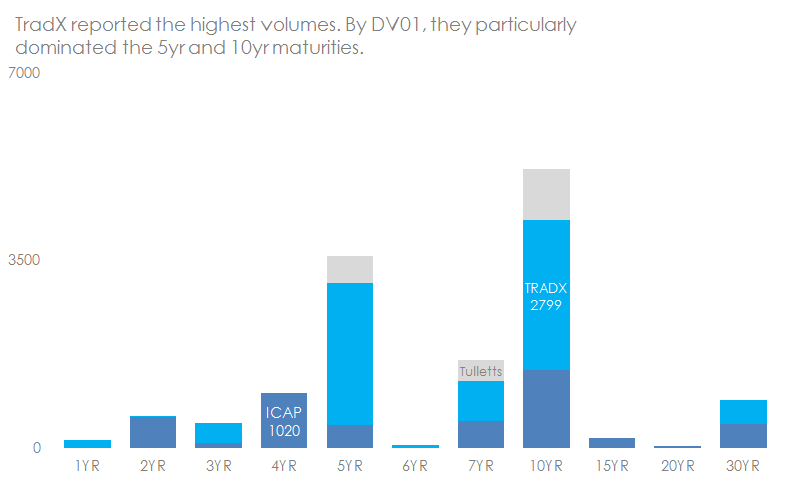

CME-LCH Basis Volume by Tenor

We can imply most of the volume data for CCP Basis through our SEFView app. Whilst there are some articles in Risk that suggest clients are also switching exposures, we assume these volumes are small relative to dealer activity. Therefore, using SEFView we simply look for the “CME” mark-up on Dealer-to-Dealer SEF reports each day to identify CME-LCH Basis trades. Most of the D2D SEFs report this, and ICAP have helpfully provided us with some private data showing their volumes split by tenor (which is not available via their public SEF reporting).

I’ve used the same data as Amir used (30th April – 15th May), but split by DV01 per tenor. This allows us to look at both the market volumes in different maturity buckets, and the market share by SEF (only including ICAP, TradX and Tulletts for now):

As we said last week, the TradX figures are probably a little inflated due to the presence of outright CME trades. However, given that these were very probably hedged at LCH anyway, we are comfortable including those volumes for now. It is worth noting that TradX did have a huge volume day on 30th April, so as with any emerging market, these volume figures can be very sensitive to the exact time window.

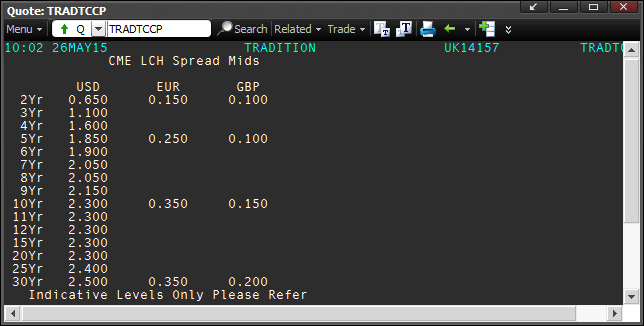

Price Data by Tenor

So why bother with volumes by Tenor? What does it tell us? There are 3 significant points I want to highlight:

- 21% and 15% of total USD Swap volumes on TradX in 7yr and 10yr maturities were CME-LCH basis related. This highlights how significant this market has become in a very short space of time.

- 30 years has seen decent volumes already, highlighting the long-dated nature of some of the risk out there.

- Some maturities have seen very little trading activity – so we need to take the price information out there with a pinch of salt when looking at non-benchmark points.

Back in the day when Libor-OIS and Libor 3m-1m basis were evolving into long-dated markets, the “term structure” (i.e. shape of the curve) was driven by an expectation that “normality” would return. Hence 10yr and 30yr basis was much narrower than the short-end. With this CCP Basis market, this is precisely what we do not see.

I used the price-data from ICAP and Trads to generate a simple model for the forwards in Excel (this hasn’t gone through the proper Clarus forward curve generator, so single curve only).

TradX were kind enough to provide us with updated prices earlier today:

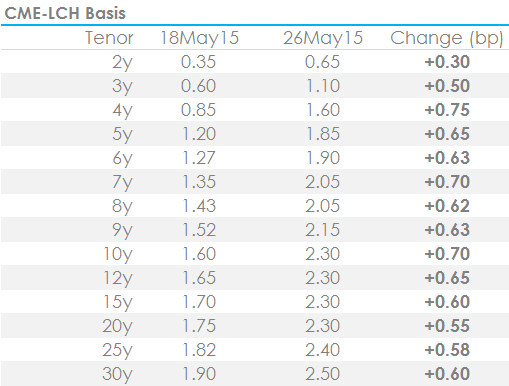

Since Amir published his blog we can see that the basis has continued to widen:

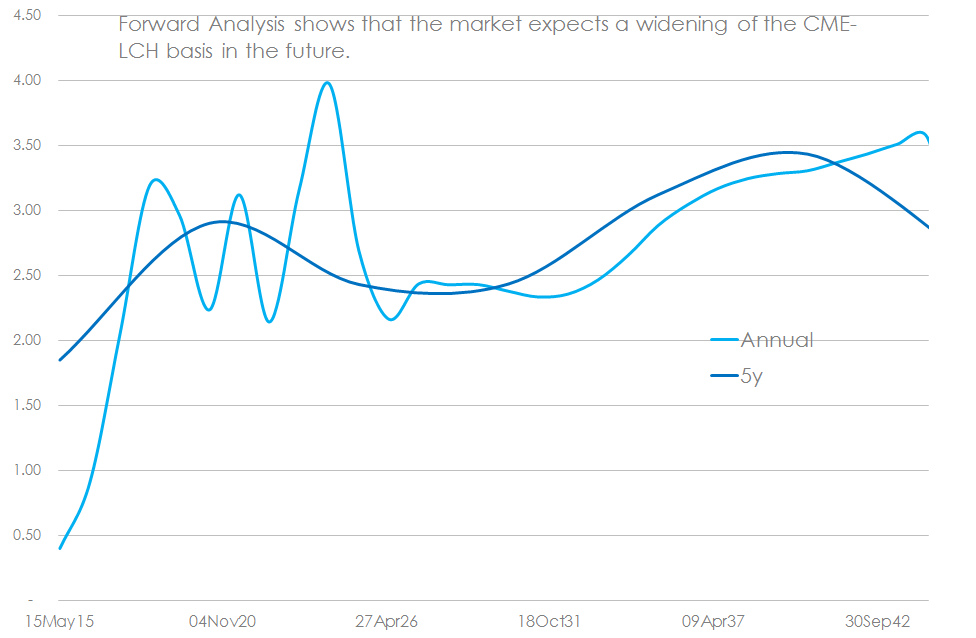

When I plug this into my curve model, I see an upward sloping curve in forward space that shows the market is not expecting this basis to revert to zero:

Two things of note:

- It looks like long-term payers of fixed rates at CME are causing the basis to be widest in the longest tenors of the curve. This results in an upward sloping curve. For example, 5y5y forward is at +2.9bp versus a spot level of “only” +1.85bp.

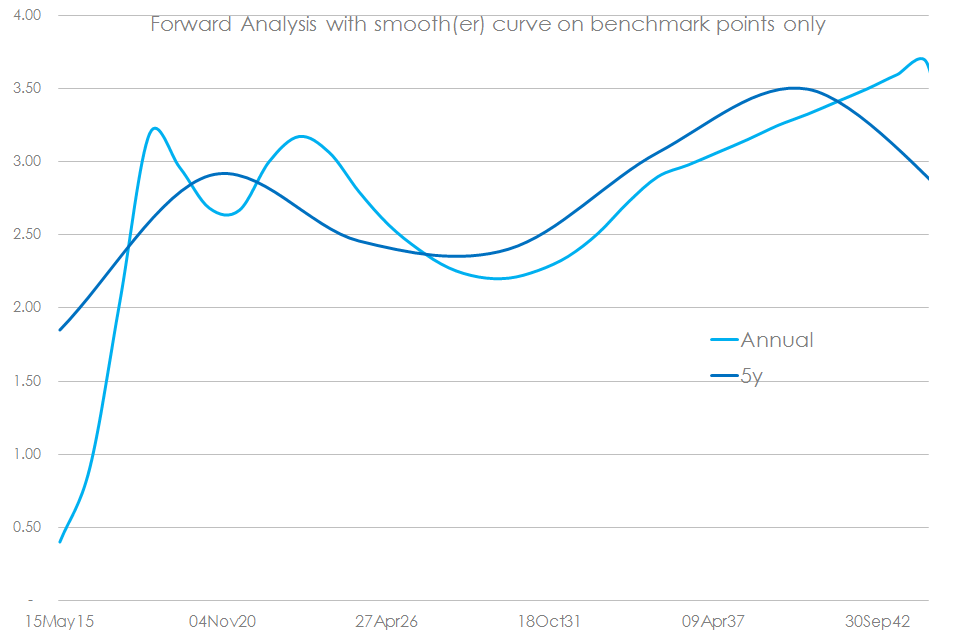

- Given that volumes have been very small in non-benchmark tenors, and because this is an evolving market, I would suggest taking only price information for benchmark maturities. We can therefore remove points such as 6yrs, 12yrs and 25yrs from the curve build to remove some of the noisy peaks and troughs:

This simple analysis already tells us a few things about the market:

- Most obviously, the first “hump” on the curve is 4 years. This corresponds with the point on the curve that has seen the largest increase in price (“widening of the basis”) in the past week (of +0.75bp). Maybe this is telling us that a lot of positions have an average maturity of 4 years, which is hence creating a concerted paying interest in this maturity. If this is the case, we may see the longer maturities moving even higher to remove this “hump”.

- Conversely, the “belly” of the curve is cheap compared to the wings, suggesting a relative lack of paying interest around 10 years. This may also help explain why volumes have been highest at this point in the curve. If there is a lack of paying pressure at this exact maturity, then offers will be “easier” to find and payers who need to hedge both 4 years and 30 years may choose this as an average maturity.

- Unfortunately, unlike Libor-OIS strategies back in 2008/9, there do not appear to be hugely compelling carry trades out there. The maximum roll-down for the 1 year forwards is just 1.1bp per year. That is unlikely to be enough to attract hedge funds into the market to provide speculative liquidity just yet.

Overall, it is telling that market participants do not expect this basis to be trading at zero in five years time – for any maturity. If I were a bond issuer I’d be telling my swap bank to price off the CME curve right now!

Other Currencies and Other CCPs

With this basis clearly a hot topic, it raises natural questions as to the evolution of other CCP-basis markets. For example:

- Does the same structural imbalance exist outside of USD swaps? Are all users of CME clearing naturally buy-side market participants who want to pay fixed against their asset base, even in EUR, GBP or JPY?

- Will other CCPs offering cross-margining versus bond futures suffer from the same structural imbalance in their customer base? Does this mean that fixed rates for EUR swaps cleared at Eurex are therefore higher than at LCH?

- With portfolio cross-margining, what are the benefits of paying fixed in non-USD currencies in your CME portfolio? Is this a “cheaper” hedge?

- If all interbank liquidity is concentrated at a single CCP, will there eventually be a “liquidity premium” (fee based, maybe?) for all trades conducted away from this CCP? Afterall, your IM requirement as a market-maker can be doubled irrespective of whether you are paying or receiving.

- As per the above, there is an intrinsic cost of carrying IM at two or more CCPs. This cost will probably increase as rates increase (in the same way that margin income increases for CCPs at higher rates). Is this why we have an upward sloping CCP basis curve (and therefore are we ready to model the correlation effect of outright rates on CCP basis?!).

- And taking that a step further, do we believe that long-only bond funds are naturally payers of negative swap spreads? By extension, does that also mean that our CCP-Basis curve has some kind of convexity versus swap spreads at a zero strike? Try modelling that….

- Given all of these potential market drivers, why did nobody think of this earlier?!

CHARM and CCP Basis

As a quick reminder, the reason Clarus are able to write in-depth about this market already is because of our margin optimisation software, CHARM. Amir has written today about how we monitor the risk at each CCP in CHARM, and I would implore all market participants to at least work out their intrinsic cost of carrying huge IM balances at different CCPs. That at least gives you a base-line for where theoretical CCP “bases” are for your exact portfolio.

So sign-up to our newsletter and get in touch!