What are MAC Swaps?

A brief reminder that a MAC swap is a particular flavour of forward starting interest rate swap, starting on an IMM date (third Wednesday of Mar, Jun, Sep, Dec) and has a Market Agreed Coupon. This coupon, rounded to the nearest 25 basis points, is virtually at par at the time of first issue. MAC swaps are available in USD, EUR, GBP, JPY, CAD and AUD.

The swaps trade on an NPV-basis (a cash fee is exchanged) and are very simple for CCPs to net down into single swaps.

CCPs may argue that coupon blending for vanilla IRS makes MAC largely redundant, but that doesn’t stop people trading them 🙂

Talking of CCPs, CME became the administrator of MAC swaps back in March this year, taking over from SIFMA. This is good, because the links to MAC coupons were dead on the SIFMA website when I checked, but the CME is all working well!

What Currencies Trade?

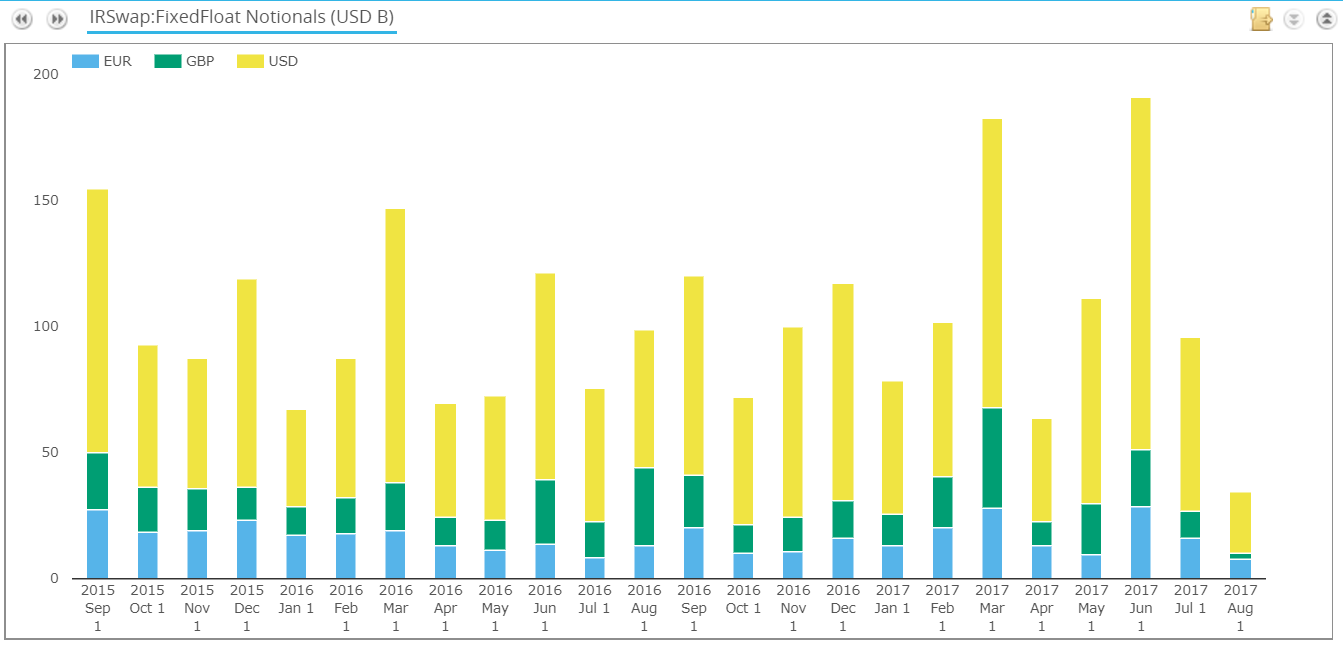

Between 2015 to 2017, SDRView shows a steady pace of activity in MAC Swaps;

Showing;

- MAC swaps traded in the three most active currencies, USD, EUR and GBP.

- USD contracts are by far the most active amongst accounts reporting to the US SDRs. This is also true of vanilla contracts. In MAC swaps, they make up over two-thirds of volume (nearly 70%).

- EUR is the second most active currency, followed by GBP.

- CAD MAC swaps have traded less than 500 times this year, with no CAD MAC swaps reported to the Canadian DTCC.

- JPY MAC swaps have traded fewer than 150 times in 2017, and AUD just 88 times.

How active are they?

MAC swaps are clearly niche in CAD, JPY and AUD. How does their activity in USD, EUR and GBP compare with other subtypes traded?

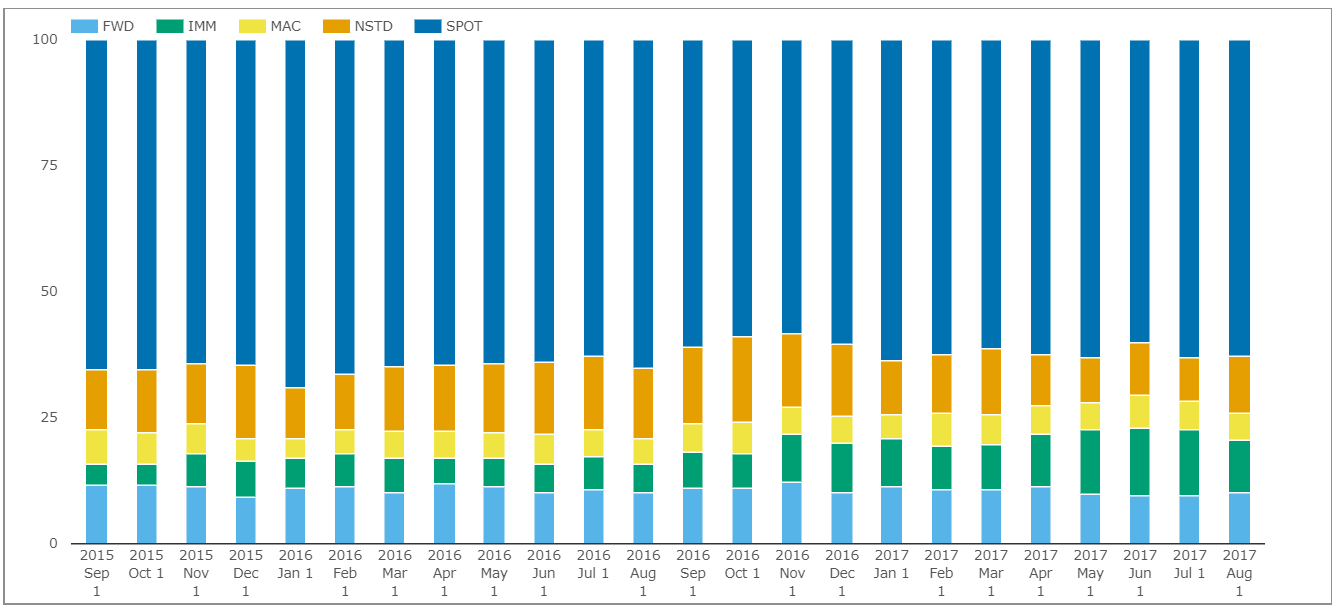

USD Swaps

- For USD swaps, the chart above shows that MAC swaps consistently account for 5-6% of trades each month.

- If we restate the above chart in notional terms, this drops fairly drastically to 3%.

- This suggests that the average trade size of MAC swaps is smaller than the industry average.

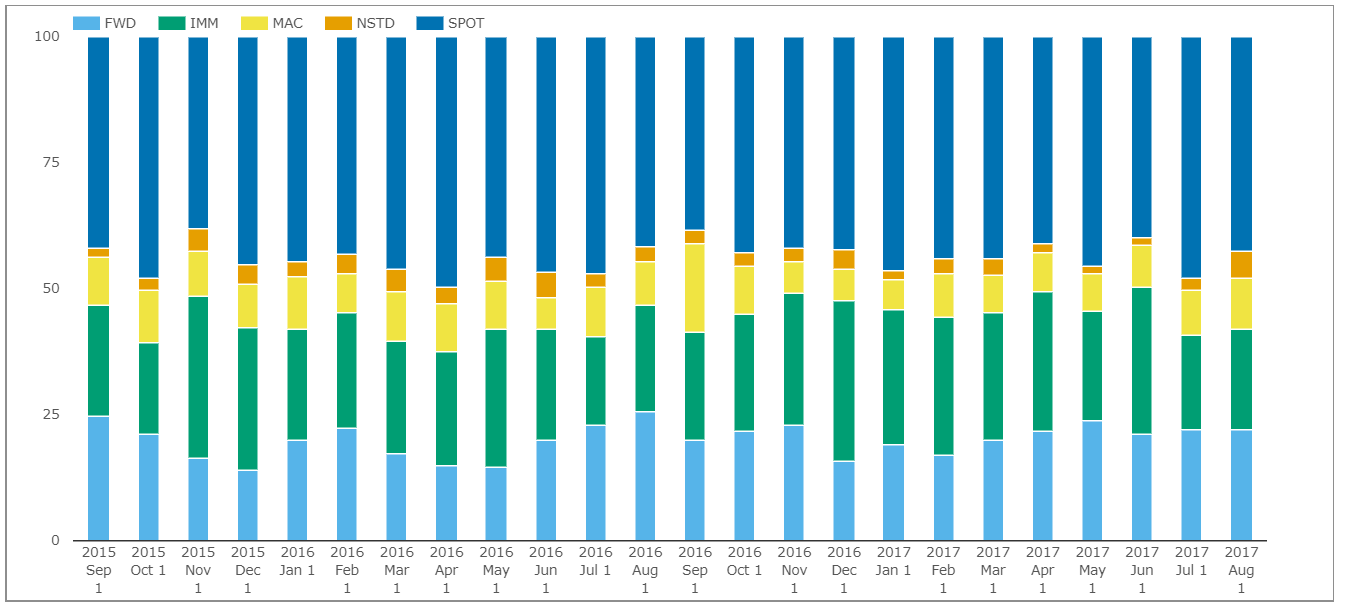

EUR Swaps

The story is consistent with Tod’s previous blog. Over 30% of swaps (by trade count) reported in EUR continue to be IMM starting – either MAC or “vanilla” IMM starts:

We are led to believe that this is due to reporting bias in the US SDR (i.e. an overweight of US hedge funds reporting rather than European swap dealers who trade spot in much larger size).

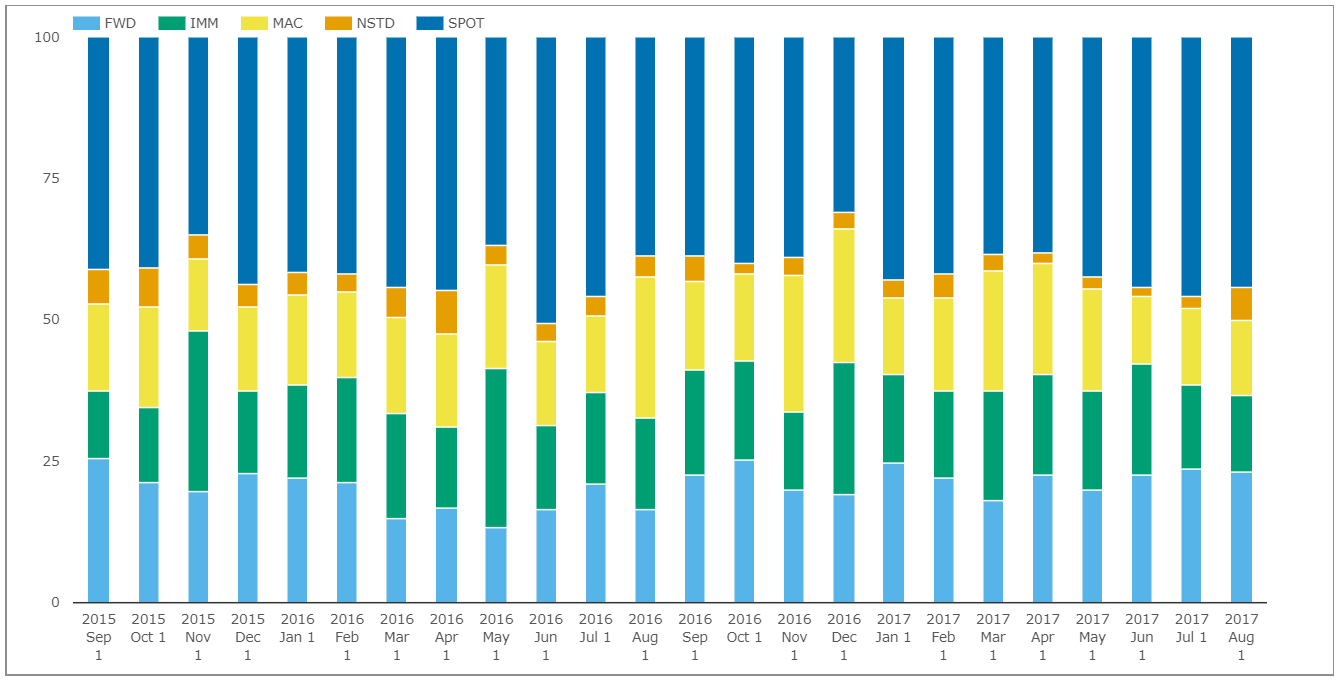

GBP Swaps

As we covered in GBP Swaps for Dummies, nearly half of GBP IRS reported to US SDRs are forward starting in some form or other. This is the same across notional, DV01 and trade count measures:

Due to the smaller sample size in GBP swaps, the proportion of trades that are MAC does vary more than in other currencies. For example, up to 25% of trades (by trade count) are MAC. But it can be as low as 13%.

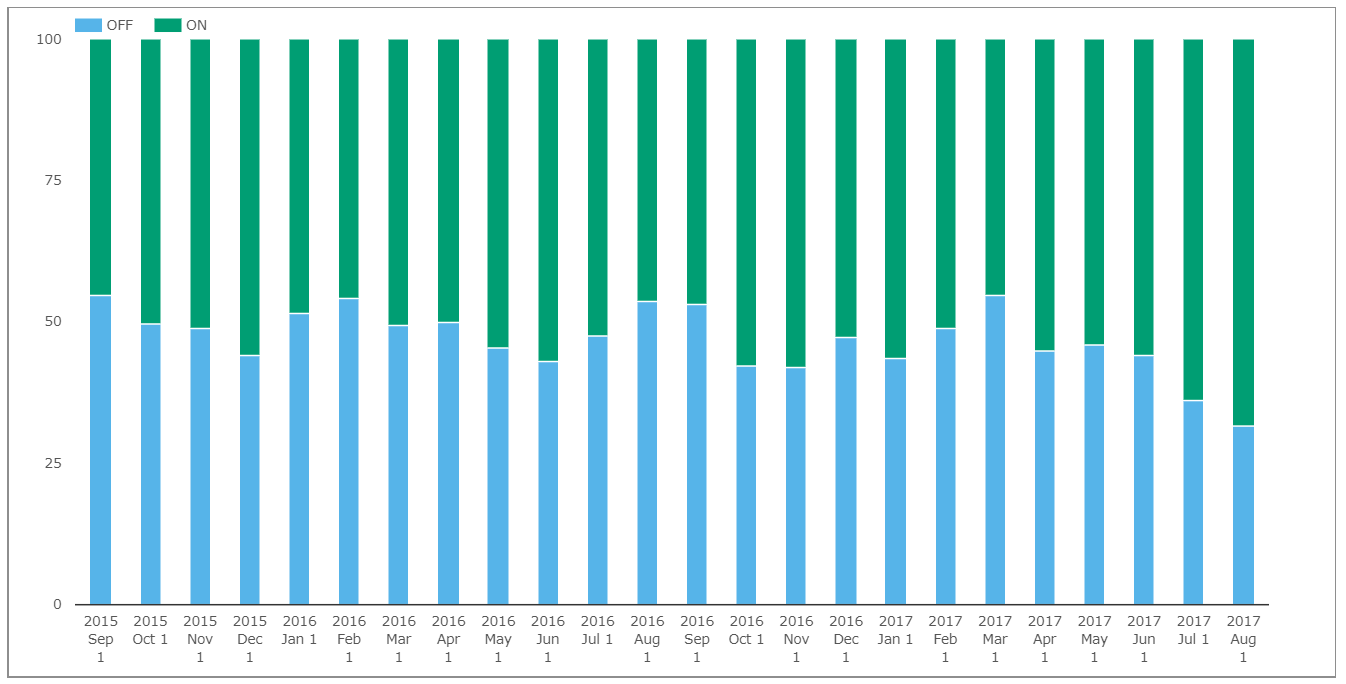

Where do they trade?

We expected to see a large proportion of these swaps trading on-SEF given their standardised nature. Recently, we have seen SEF trading in these instruments begin to increase from the ~50% level:

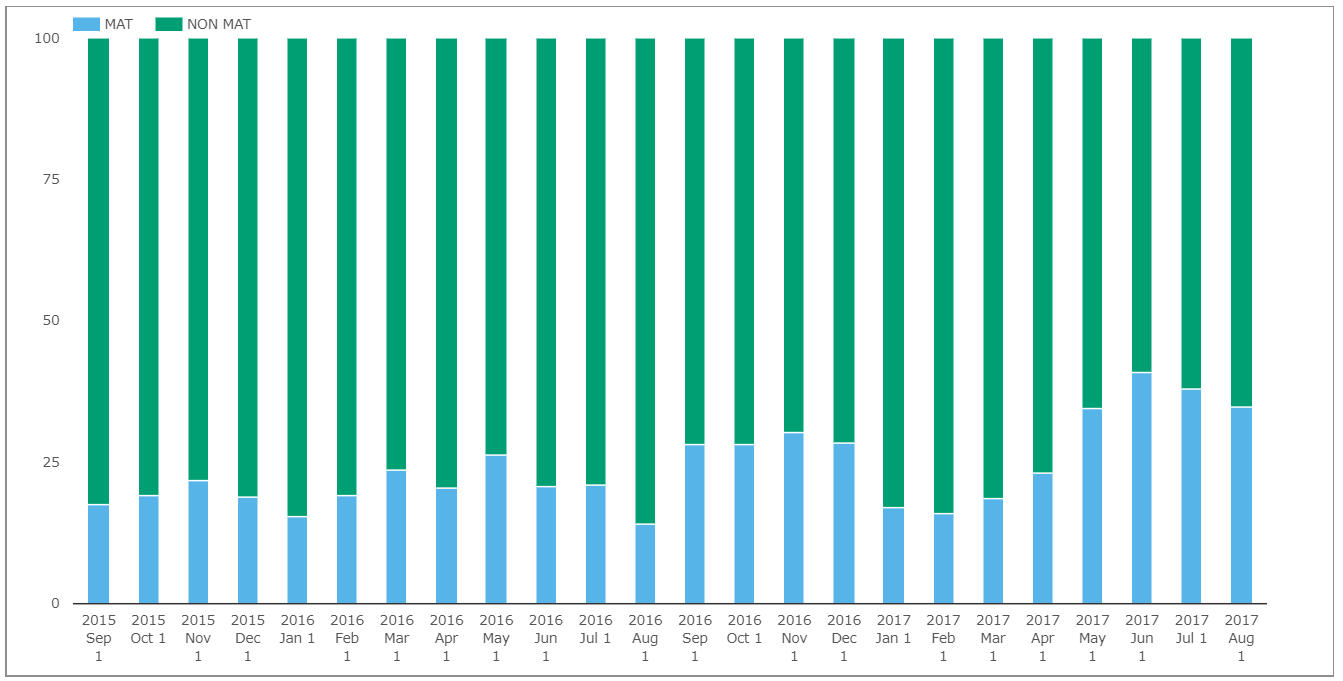

So what trades off-SEF?

Prepare yourself for a chart blitz as this is a little intriguing. We expected all MAC trades done off-SEF to be outside of the Execution Mandate. And yet the data shows some MAT trades executed off-SEF:

Basically, this chart tells us that around $15bn per month is trading in USD MAC swaps off-SEF. Around 15-20% are block trades (by trade number), but there remains a portion of USD MAC swaps traded off-SEF.

Whilst this has long been a curiosity in the overall SDR data universe (we looked at it here), it is even more curious in a standard contract such as a MAC swap. Is this bad data? Or counterparties who are not subject to the execution mandate reporting swaps?

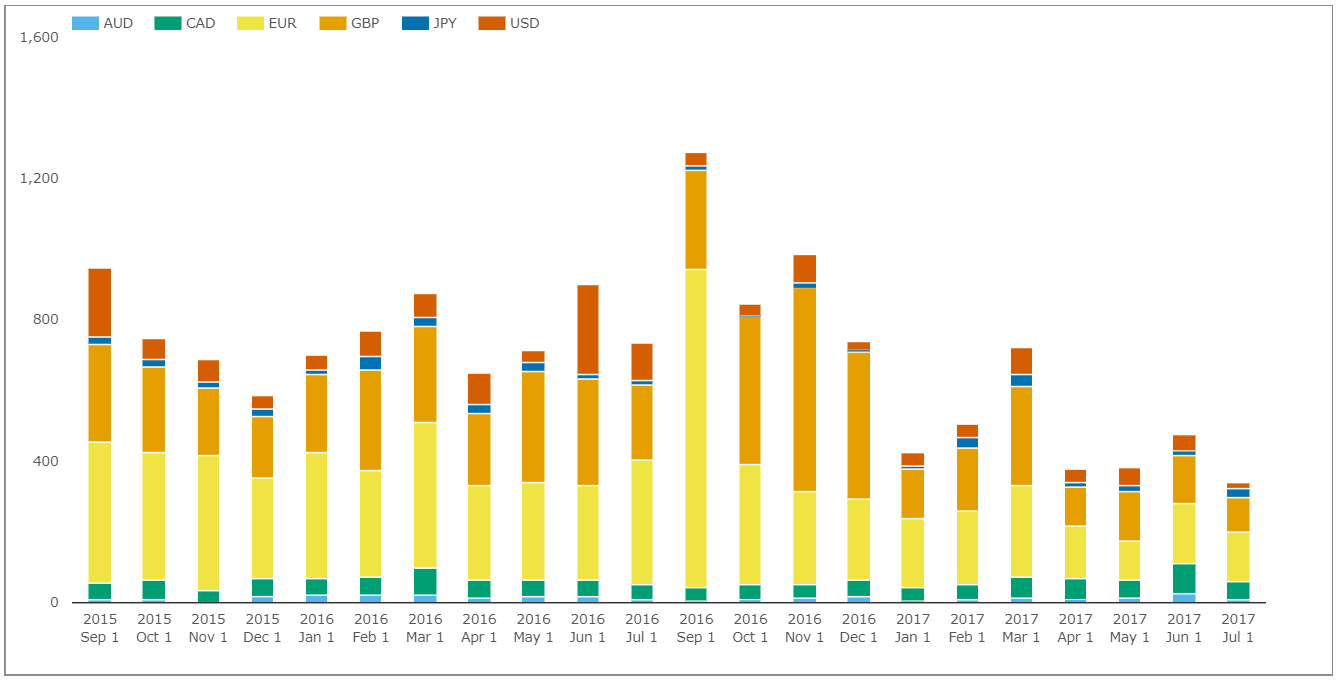

Let’s assume these MAT MAC swaps off-SEF are bad data. What we see is a rapidly shrinking number of non-USD trades off-SEF:

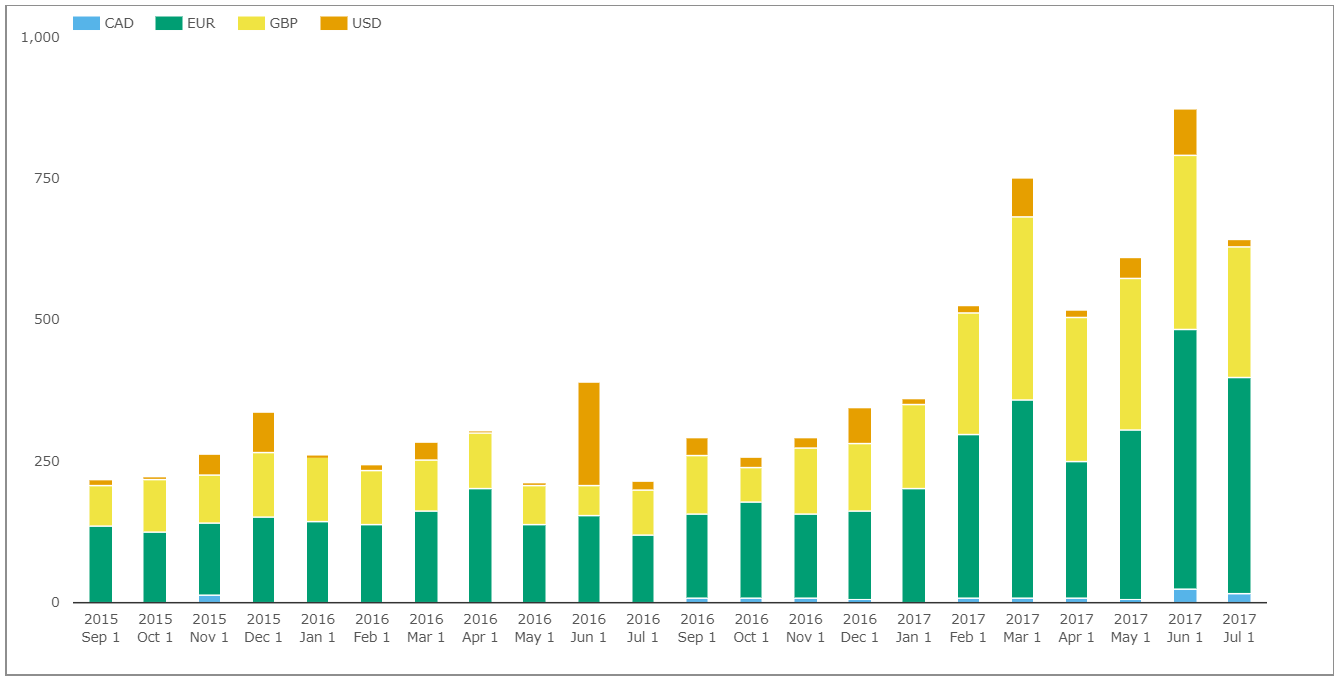

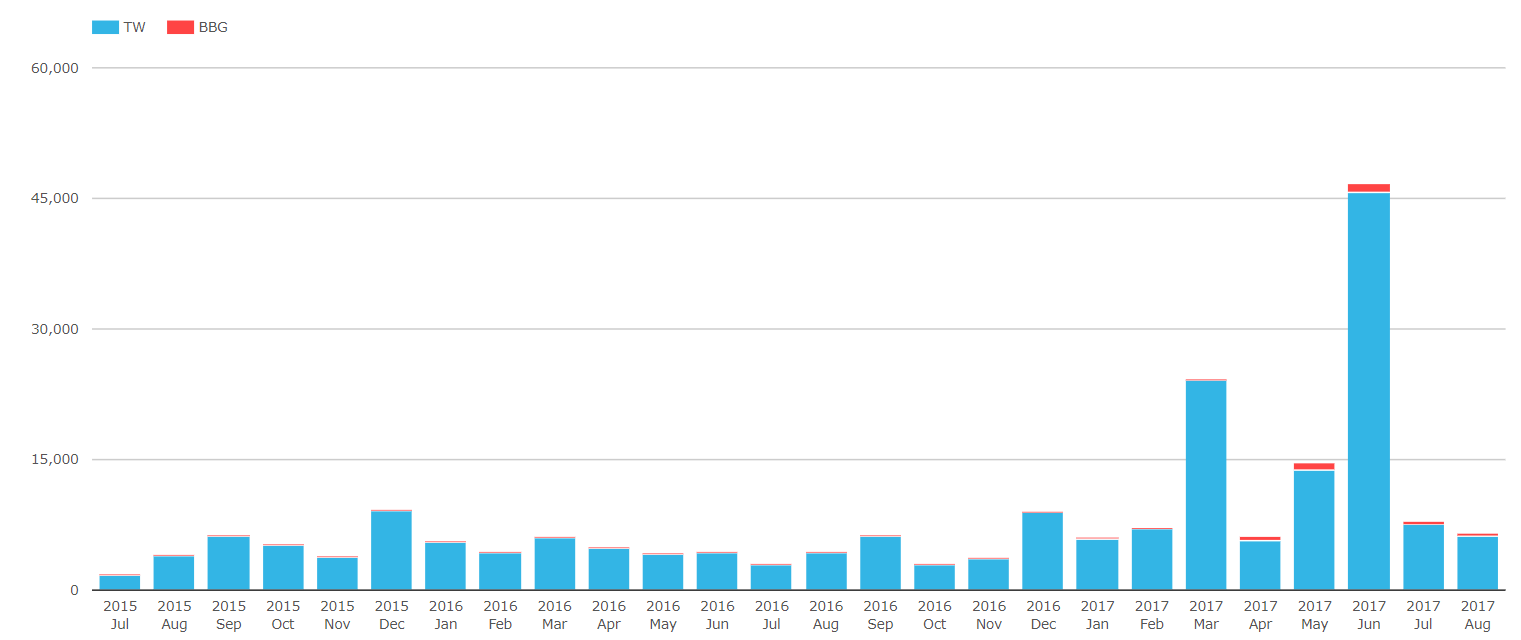

Flipping that chart on its head, and here for the headline hunters:

Non-USD MAC SEF trades have doubled since last year!

All MAC swaps traded on SEF are across D2C venues – either Bloomberg or Tradeweb. SEFView shows that growth in non-USD MAC swaps has largely been across Tradeweb:

Please take these numbers with a pinch of salt. These are small volumes we are talking about in the bigger picture of things.

How do they compare to Swap Futures?

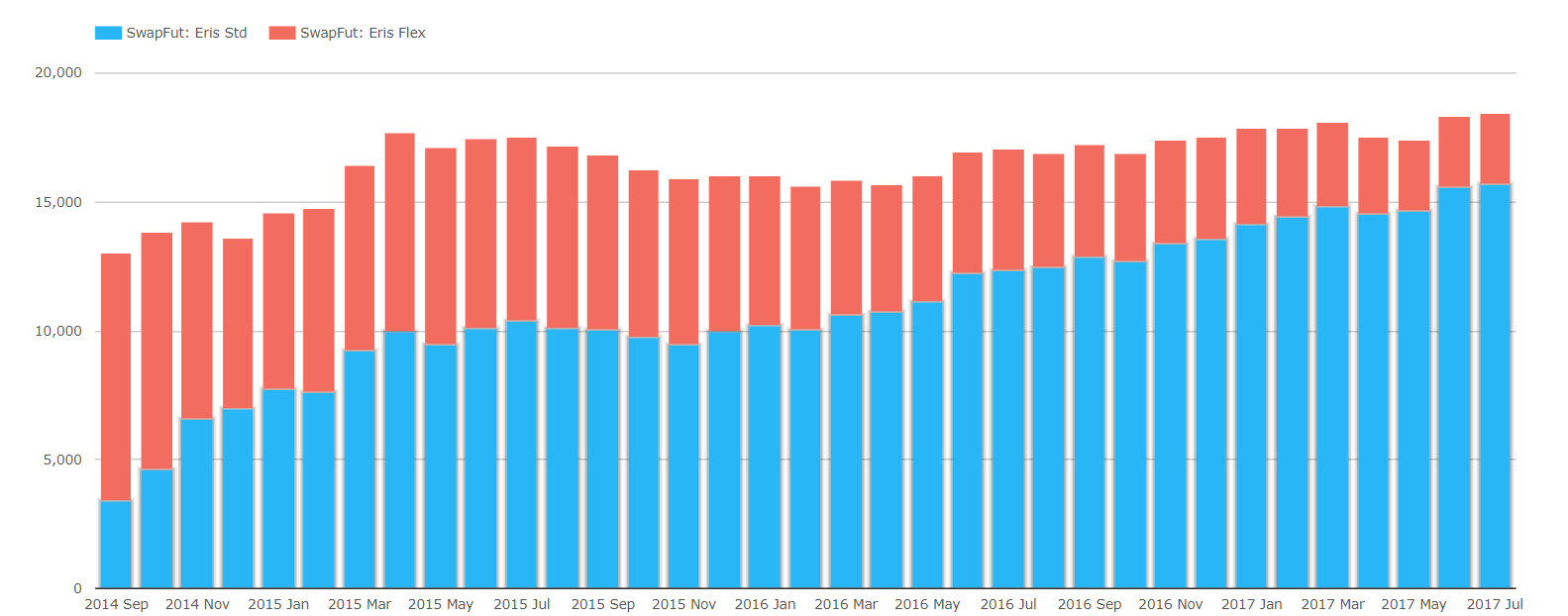

One of our incentives for revisiting MAC swaps is that ERIS futures have recently set new Open Interest Records. We can see this in CCPView:

Showing;

- Open Interest has grown in ERIS Standards whilst shrinking in ERIS Flex contracts.

- Total Open Interest has hit consecutive new highs in both June and July 2017.

- ERIS standards have MAC coupons, so are very similar to OTC MAC swaps.

- Open Interest can be a good measure of market uptake. It would be nice if CCPs provided Notional Outstanding for MAC swaps to give a fair comparison.

ERIS standards have averaged $3.7bn notional equivalent each month in 2017. For comparison, MAC swaps have averaged $120bn notional each month in 2017. It looks like ERIS standards have plenty of room for growth as the industry focuses on capital efficiencies. Just bear in mind that ERIS are cleared at CME, whilst we assume some of the OTC business is conducted at LCH (CCP Basis!).

In Summary

- Monthly volumes in OTC MAC swaps continue to be pretty consistent.

- Over 50% of MAC swaps now trade on D2C SEFs.

- The off-SEF MAC data is surprising.

- Tradeweb transact most of the non-USD MAC volumes that occur on-SEF.

- ERIS standards have seen significant growth. We will continue to monitor ERIS volumes versus MAC OTC volumes.