I’ve been optimistic about swap futures for a few years now. But every time I go look for evidence, I walk away thinking “maybe next year”.

We’ve written about swap futures a few times before. The quick bullet point list of why one would be optimistic on these products:

- They replicate Vanilla OTC swaps nicely

- They are exchange traded in an order book, complete with the ability to do block trades off-exchange

- As such they fit into every Bank, HFT, PTG, CTA etc technology stack today

- Margins are typically lower than the OTC swap equivalents, hence leverage can be larger

- There should be some capital advantages to firms impacted by the leverage ratio. The PFE notional addon for futures is 0.5% while OTC variants go up to 1.5% for IRD and 5% for Credit.

- And even if you are not impacted by the leverage ratio, your FCM is, and you are paying for it

The Data

There are a handful of swap futures that we monitor on Clarus CCPView:

- CME DSF (MAC swaps)

- Eris “Standard” MAC swaps, and “Flex” / bespoke swaps. USD contracts cleared at CME, while EUR and GBP cleared at ICE.

- Eris Credit Futures at ICE (HY & IG)

- Eurex IR Swap Futures, and Eurex-cleared GMEX CMS Futures

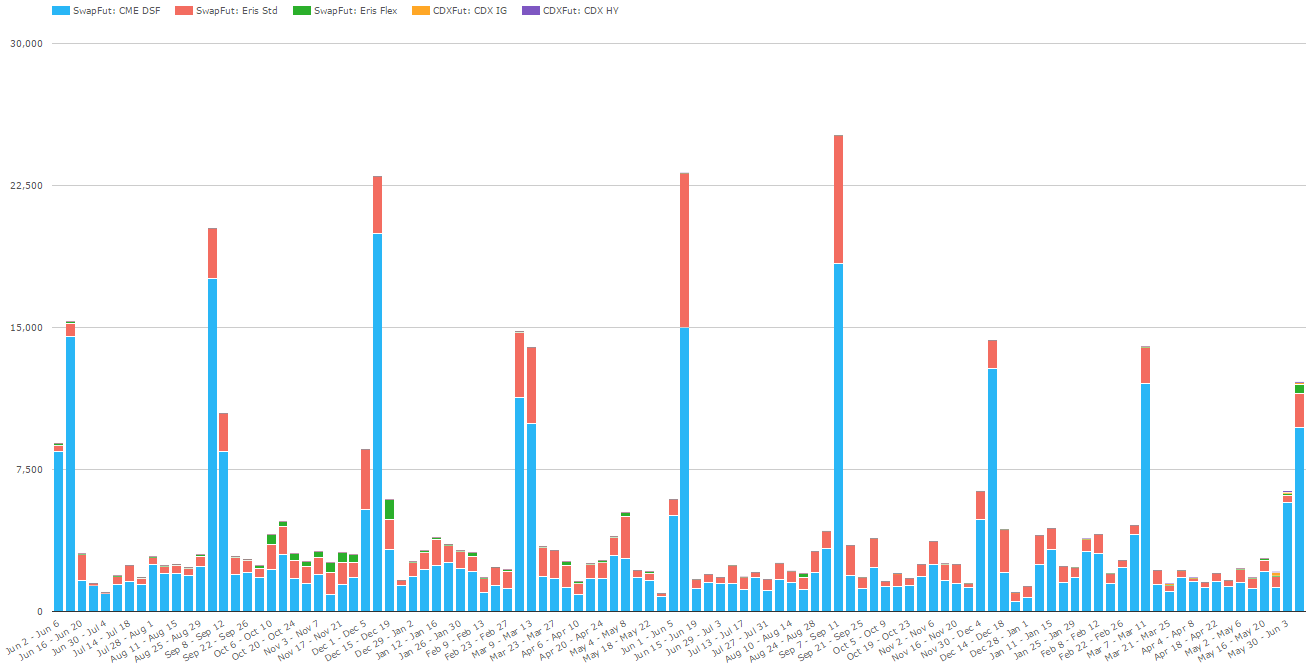

Of these, the CME and Eris rate swaps are the most notable, but we do see some activity now in the Credit futures. Here is a look at weekly cleared volume of these products over the past 2 years:

This shows CME DSF and Eris Standards as the primary active contracts, with the typical quarterly blips around the roll dates. But progress seems light.

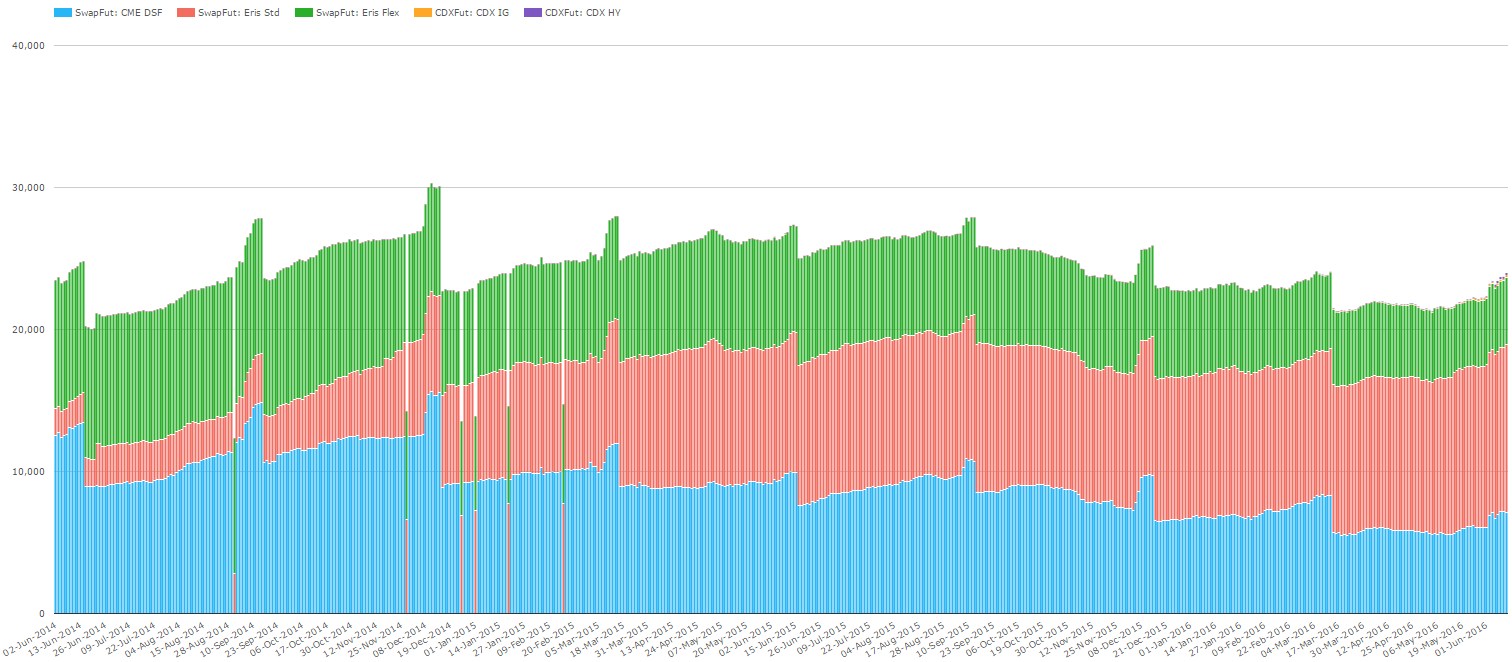

Now onto Open Interest. Blue bars are CME DSF, Red is Eris Standards, and Green is Erix Flex:

This too does not shout success in swap futures quite yet. However I would encourage you to look at just the blue and red lines, and exclude the Green Eris Flex contracts, as these are very bespoke, and hence easily inflated.

Now, roughly 20+ billion in futures open interest might sound like a big number, but it amounts to not even a rounding error when you compare it to the 27 trillion of open interest for USD Vanilla IRS at CME and LCH. Cleared OTC is 3 orders of magnitude larger.

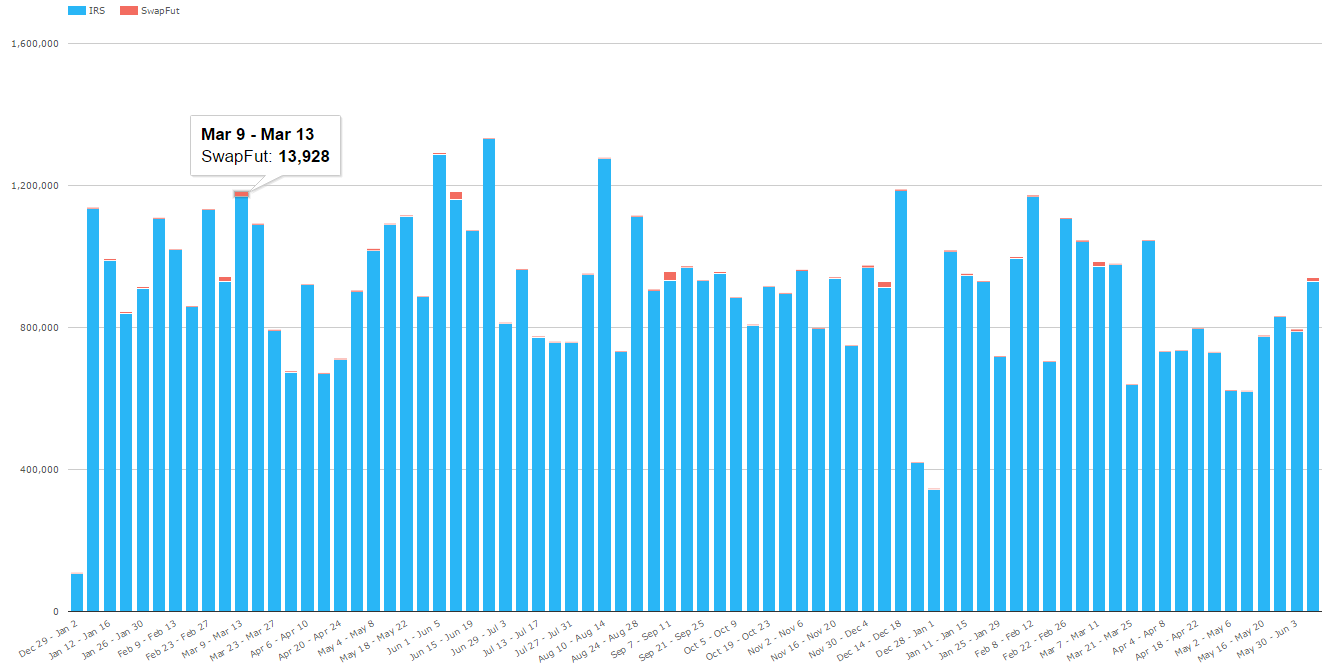

To get swap futures to show up on the same chart as OTC, I had to look at weekly volume vs USD-only, vanilla IRS cleared volume for the past 18 months. Note the very small red blips, which on the most optimistic weeks account for just 1% of the USD swap market:

Looking for an Inkling

I still contend the way the swap futures market will unfold is:

- Step 1 – Firms to find reasons to move to standardized OTC contracts (IMM & MAC). The reasons should include the ease of unwinding at the CCP, but arguably could include things like solid liquidity.

- Step 2 – Firms realize that swap futures replicate these standardized contracts and transition to them

So if growth in standardized contracts is the predecessor to swap futures, let’s go see how standardized contracts are doing.

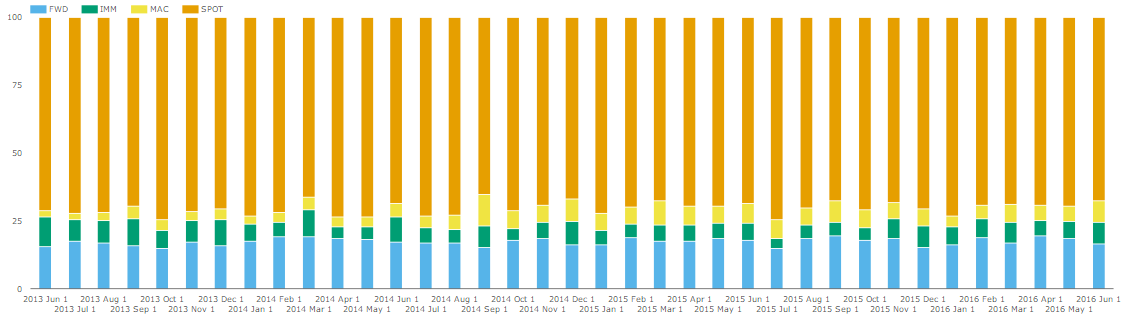

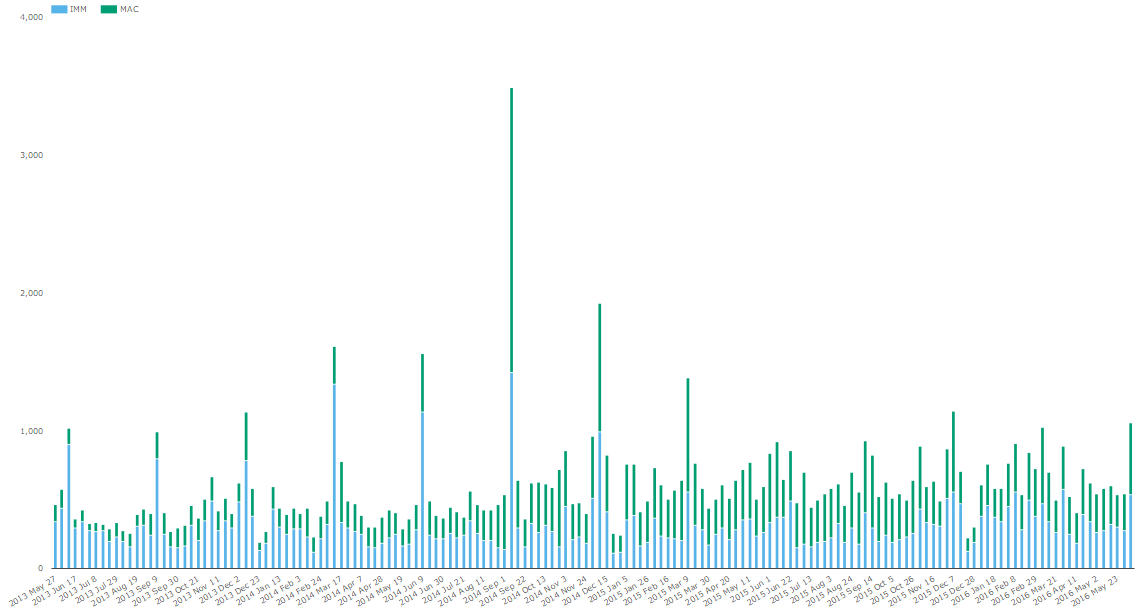

To give the data the best chance of painting a positive picture, I chose to look at just USD Fixed Float swaps, and I also chose just trade counts. Reason being DV01 and notional values might skew the picture if in fact there were more, yet smaller, trades being done in standardized contracts. (Or more appropriately, I have chosen to use trade counts in hope of skewing the results in favor of standardized swaps!). This looks at Spot, Fwd, IMM and MAC trading:

You can see that on a percentage basis, the Green (IMM) and Yellow (MAC) swaps are not greatly eating into the Orange (Spot starting) or Blue (Fwd Starting) swaps. On a percentage basis, we’re still taking maybe 10-15 percent of the USD swap market is IMM & MAC.

As for what these trade counts are:

This tells us that on a good week, there are maybe 1,000 standardized USD OTC swaps transacted.

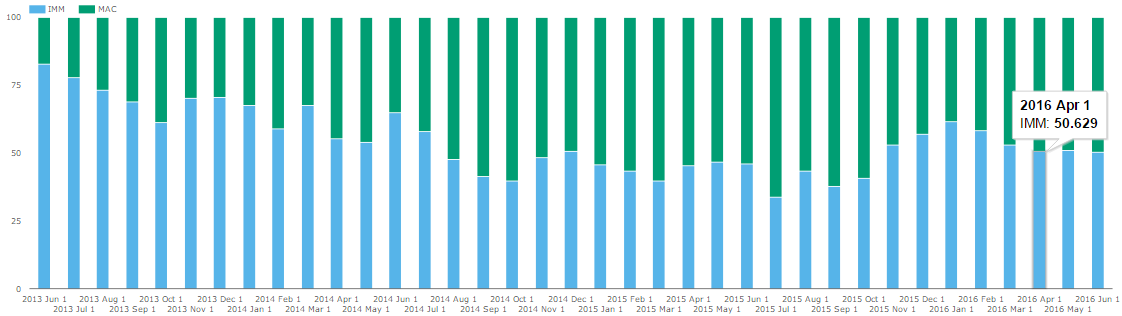

Lastly, on a positive note, we do see evidence that MAC swaps account for generally 50% of standardized swaps (vs par-rate IMM):

Optimistic Picture

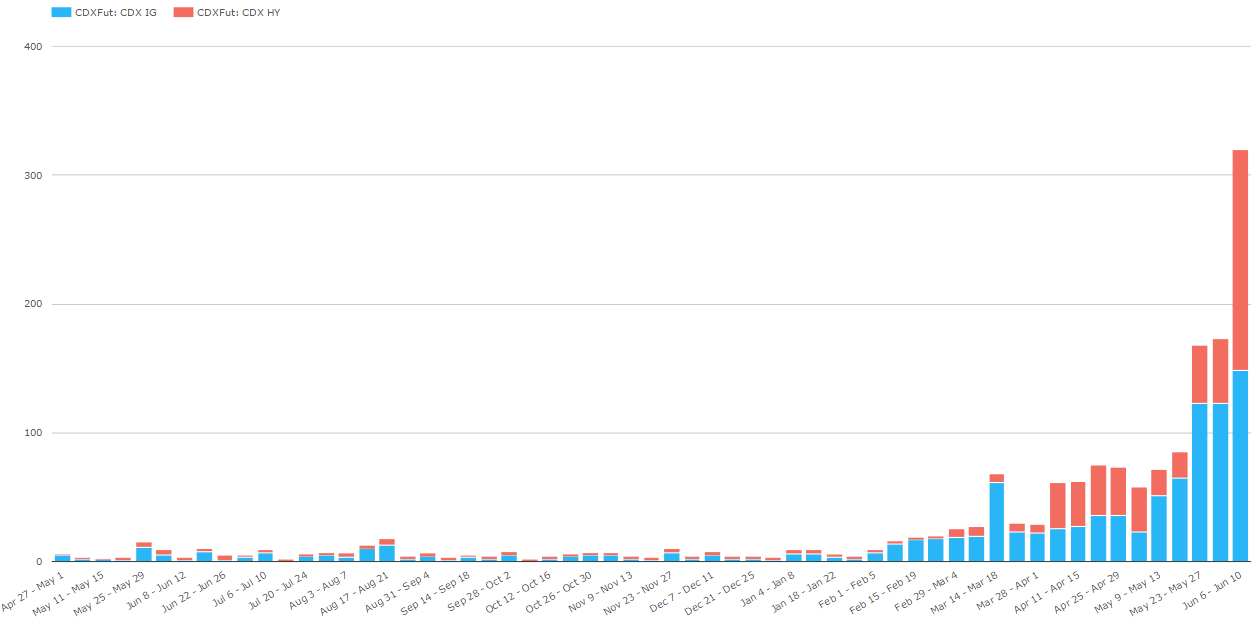

The best data I could find to paint a rosy picture was the recent uptick in activity for Eris Credit futures on ICE:

The scale here is in millions, so yes, that is 300 million USD of OI. Hey, its a start.

The CDS market fits in nicely with my theory. It long ago made the transition from bespoke to standardized OTC contracts. Surely a futures contract is a logical next progression.

Summary

The data seems to say there is some small overall progress in swap futures.

What got me to go look at this again was a few recent press articles about new partnerships and more entrants into this space. I’m sure you can find them with the appropriate google. Perhaps they will contribute to some growth here.

We’ll be keeping an eye on it.

Not sure that I agree that these swap futures replicate OTC swaps.

Just take a look at the Eris Contract settlement price. The settlement price includes a host of variables other than NPV. The NPV of a swap at maturity is 0. Not so with the Eris futures contract. Most of these variables are close to zero now because LIBOR is so low. Will this always be the case? If the value of these other variables deviate from zero, the impact to a firm relying on hedge accounting might be fatal.

GMEX is even more perplexing. It requires periodic adjustment to roll maturities down the yield curve. A benefit of an OTC swap is that such manual adjustments are not needd.

Thanks for the comment Barry.

The NPV of a swap future at maturity of the (underyling) swap will also go to zero, not to be confused with the maturity of the future, which delivers/transforms into a physical/underlying swap, based on whether we’re talking physical settlement (CME DSF) or the future-style (Eris).

I wouldnt want to give advice on hedge accounting, but the variables you are speaking about I believe are limited to:

1) Fixed and float coupons – which are collateralized under Eris-style as well as cleared OTC. In bilateral space are physically settled.

2) PAI – which is a cleared OTC and futures answer to replicate the interest on collateral.

Tod,

Thanks for your reply.

A NPV of a swap (cleared or otherwise) never includes the value of previous paid coupons (actually no fixed income instrument does. even stocks trade ex dividend). And the NPV of a swap equals the final settlement price. ERIS differs in that the settlement price and NPV are different. And they will diverge significantly over time. A company using an ERIS contract must report gains/losses based on the settlement price — not the NPV.

And the margin savings apparently only apply to the ‘standards’ not the flexes — which is what most users want.

And as most swaps are amortizing — not sure how to execute quarterly amortizing swaps in ERIS without executing dozens of ‘flexes’ — each with e different PAI and accrued coupons! Euro$ futures are much easier to execute.

I think such details are what has limited liquidity in so-called ‘look-alike’ futures contracts.

Again, thanks for the opportunity to discuss.