Back in August I wrote an article about how large, self-clearing firms can reduce the amount of capital required to support their cleared business by wisely choosing to backload margin-reducing bilateral trades.

Typical Trading Firm Account Structure

Trading firms tend to have multiple FCM relationships. This is slightly counter-intuitive, given that the most optimum use of funds would be to put everything through one FCM. Of course the issue there becomes that you have all of your eggs in one basket, which exposes you to:

- You are beholden to that FCM’s rules and fee structures

- If the FCM has trouble, all of your eggs are in a wobbly basket! (You better have a backup FCM)

Probably fair to say that firms might also get better execution services across a variety of FCMs. And don’t forget that most firms will have both a CME and LCH account at each FCM. Hence a typical firm might have 6 accounts spread across 3 FCM’s, which might look like the following:

- CME & LCH accounts at FCM 1

- CME & LCH accounts at FCM 2

- CME & LCH accounts at FCM 3

The Problem

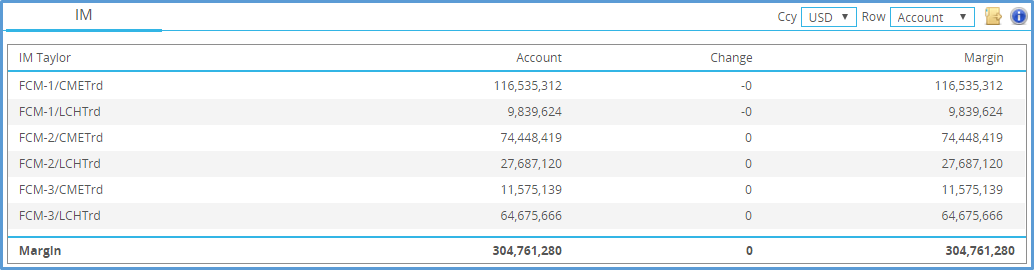

Let’s begin with an example of a firm with these 6 accounts. Starting with a simple calculation of margin for each account:

Showing that this firm has a total initial margin of $304 million pledged to their 3 FCM’s across all 6 accounts.

The question: how can you reduce this total margin requirement by doing nothing other than a simple operational procedure?

The answer is of course to move (aka port) trades from one FCM to the other. But how do you identify which trades to port?

You could attempt to identify risk profiles in each account and try to minimize any large concentrations, but there are multiple problems associated with such a simple approach:

- Large exposures on any one tenor or in any one currency might be risk (and margin) offsetting in that same account, hence a red-herring when trying to reduce margin.

- Often times, different FCMs will charge very different client multipliers. This might range from no multiplier to 100%. Hence porting trades to a high-multiplier account tends to have a larger impact.

- Liquidity addons complicate the picture.

On the other end of the spectrum, a thorough process of testing the margin impact of every trade is very iterative. If you had just 100 trades in 3 accounts, and wanted to test every permutation, it requires:

- 3 margin calculations PER TRADE. That is, you need to calculate the impact from removing the trade from the original account, and into each target account.

- This means 900 margin calculations in our small portfolio.

- And when you consider that every margin calculation on even such a small book requires 250,000 valuations, we quickly get to about 225 million MTM calculations.

- This scales exponentially: If instead you have just 300 trades per account, you are now talking over 2 billion calculations!

So, creative shortcuts are too short-sighted and may not consider some complexities; and iterative processes are very computationally intense.

Good Solution

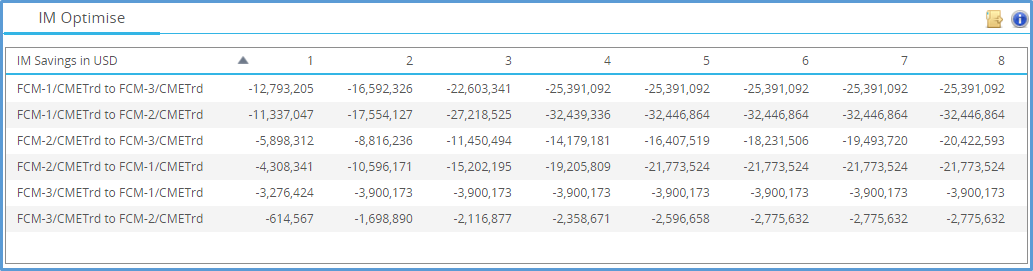

Of course I wouldn’t have written this if we hadn’t solved this problem. I won’t go into any detail on the secret sauce, but it involves a combination of smarts and computational efficiency. Having run the optimization on my sample CME accounts, I get the following:

This identifies cumulative margin efficiencies I can expect by porting trades between accounts. For example, the top left value tells me that there exists one trade at FCM-1 that I can port to FCM-3 that would immediately save me $12.7 million in margin. If I drill into this, I can see why:

Moving this trade would save $15.4 million at one account, and only increase the target account by $2.6 million.

However, I would think if you were going to go through the process of porting trades, you would want to do a handful for any single given FCM. Why not? Hence I might choose to move 4 trades from FCM-1 to FCM-2, as that seems to be the greatest single-account movement I can reduce margin by approximately $32 million. The service tells you the 4 trade ID’s you need to instruct to be ported:

By doing so, we have quickly saved 10% ($32 million out of $304 million) by doing one account transfer of 4 trades at one clearing house. I still have 2 other CME accounts and all 3 LCH accounts to attempt.

Couple final things to mention:

- It’s interesting to note how quickly an account can become optimized. My sample accounts have between 120 and 880 trades in them, and some accounts do not get any benefit after the 5th trade being moved. In all cases, by the 8th trade, the savings are minimal.

- The process can technically be done across Clearing Houses (eg between CME and LCH), however that would not constitute a simple porting of trades. Given the CCP basis, this would require a CCP switch trade to be put on, not to mention clearing and execution fees, etc. But possible if the savings are enough.

Summary

- Most firms have accounts at multiple clearing brokers / FCM’s

- This gives rise to possible margin savings which needs to be unlocked

- Firms should expect to achieve significant savings from a single operational task

- Determining the trades to be ported is complex

If you have interest in this process, we want to help you. Just contact us.