Summary:

- Initial Margin requirements for OTC Derivatives are large and increasing at CCPs

- IM Optimization is a periodic or trade by trade analysis that seeks to reduce overall IM

- Clearing members can achieve significant cost and capital benefits

- Similar techniques can be extended to UMR and ISDA SIMM

- Client IM is growing much more rapidly than House IM

- Clients can also achieve significant cost and capital benefits

Background

IM is collected by a Clearing House from each Member firm to cover potential losses on event of that Member defaulting. For OTC Derivatives given the large size and long maturity profile of trades, IM is a large number.

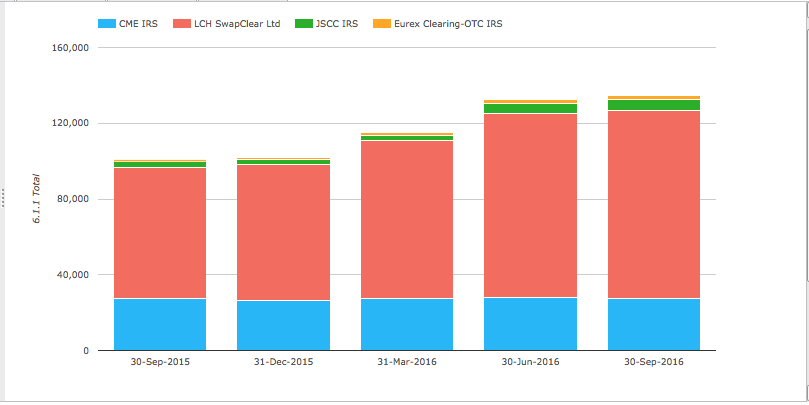

In CCPView, we see that on 30-Sep-2016, the total IM held for Interest Rate Swaps by four CCPs is $134 billion.

This is up 33% over the year in USD terms and even higher in local currency terms (as LCH IM is in GBP).

So large numbers and increasing over the past year.

What is IM Optimization?

I define IM Optimization to mean a process that seeks to reduce the overall IM of a firm (within reason) by consciously deciding where trades should be cleared (which account, which CCP) or for bilateral trades subject to Uncleared Margin Rules, which counterparts to book them with.

This may be a periodic exercise performed by a central desk (e.g. weekly or monthly) or it may be done on a trade by trade basis, prior to or post execution.

By “within reason” I mean to imply that there may be prudent risk reasons that a firm may not want to select the solution with the lowest possible overall IM option (e.g. moving all trades to one Clearing Broker), nevertheless it should search for an optimal or better solution than the status quo.

So my definition involves re-organising where trades are booked, including transferring between accounts as well as entering into new trades that do not change the overall market risk.

The means performing an analysis that provides a number of recommendations to be actioned.

In CHARM the IM Optimize menu does precisely this.

Note my definition does not include compression, which is commonly a risk-neutral exercise for an account and so does not change IM and neither does it include collateral optimisation, which is about deciding the collateral that is cheapest to deliver against a margin requirement.

Benefits of Optimizing IM

Reducing IM can provide the following benefits:

- Lowering the funding cost of IM for members and clients

- Reducing capital requirements for banks (e.g. from Default fund exposures)

- Reducing the variability and size of daily VM flows

- Reducing the size of a margin buffer

- Reduction in clearing fees, where these are linked to IM

No doubt there are others.

Lets now move onto looking at specific types of IM optimization.

Clearing Members and multiple CCPs

Starting with Clearing members and their house positions.

Global firms are members of more than one CCP for the same product.

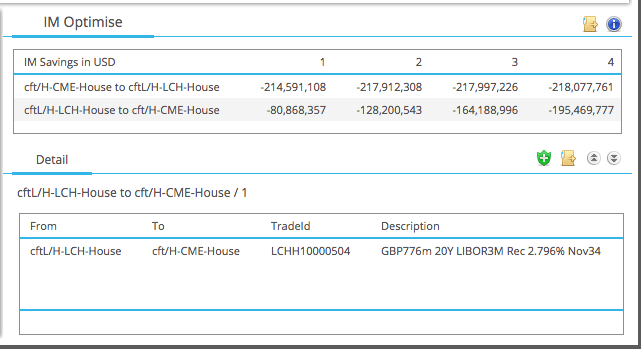

Using the CHARM IM Optimise function, we can come up with possible IM reductions for two hypothetical house accounts at CME and LCH with a gross IM sum of $500 million.

Showing that it is possible to reduce the IM by between $80 million to $218 million, depending on the direction of transfer and number of trades. So a reduction of between 16% and 40%. Very significant indeed!

Selecting just the $80 million reduction, we see one trade, a GBP 776m 20Y IRS, that would provide this benefit, if it were to be transferred from the LCH House to the CME House account.

This could not be done as a direct transfer across CCPs, but would be done as a CCP Switch trade brokered by a SEF. A topic I have covered a few times in the past, see here and here.

While there is a cost to executing CCP Switch trades, a difference in the par fixed rate at CME compared to LCH and a resulting change in CCP Basis Risk, these costs are often more than compensated for by the lower IM.

In addition large house accounts at one CCP, are likely to be subject to Liquidity Add Ons and these charges can massively increase the IM requirement at that CCP. Consequently there may be a much greater benefit than expected by transferring risk. (A case where one account to net everything is not the optimal solution).

Clearing Members and Multiple House Accounts

A Clearing member may have more than one house account at a Clearing House and a quick scan of the LCH member list on their website, shows a number of firms where this is true.

These may have been created for legal or operational reasons and particularly for the latter it may be possible to move or enter into internal trades between the entities of the holding group to reduce the overall IM, while still allocating internal cost and capital to each entity and the benefit to the group.

Clearing Members and Client Clearing

Clearing members are required to capitalise their Client Clearing exposures and have generally moved to charging customers for the use of their balance sheet. In specific situations they may be able to advice their client on how to reduce IM in a way that benefits both parties.

Swap Dealers and UMR

From 1 Sep 2016, major Swap Dealers have been required to calculate and require IM for new OTC Derivative trades from other major Swap Dealers and are doing so using ISDA SIMM.

Where an OTC Derivative is eligible for clearing but not mandatory, a firm could decide between a bi-lateral trade or a cleared one. Indeed we have seen that since 1 Sep 2016, a significant chunk of Non Deliverable Forwards and Inflation Swaps have moved to Cleared. (see NDF Volumes and Margin Rules are pushing Swaps to Clearing).

Generally given the efficiency of multi-lateral netting at a CCP over bi-lateral netting at each dealer, the choice will invariably be to use Clearing, so probably not a great scope for IM Optimization between the two.

However there is definitely an IM optimisation opportunity across Swap Dealer counterparts.

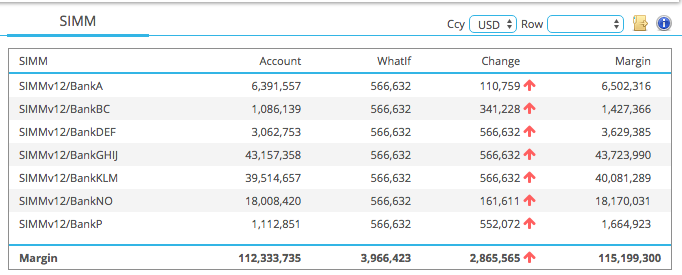

The CHARM screen below shows SIMM margin for seven counterparties.

And shows a WhatIf test of a proposed trade, which would have a stand-alone SIMM IM of $566k.

However the lowest increase in SIMM IM would be if we executed this trade with BankA, which we should do provided BankA was offering a price that was materially equivalent to the best price from any of the others.

So in this case we have a pre-trade optimisation.

Similarly it would be possible to run periodic post-trade portfolio level optimisation recommendations.

Swap Dealers and Backloading

Where a Dealer has legacy bilateral trades which are eligible for clearing (and not subject to UMR) it would be useful to determine which of these trades could be backloaded into clearing and reduce IM.

I would assume that most firms have completed such exercises with their major counterparts, however there may well be smaller counterparts where worthwhile gains are still to be had.

Client Clearing

Clients also have many opportunities for IM Optimization, as they generally have two or more FCMs and while historically the priority has been to get the operational plumbing of clearing working, now that is done and dusted, the focus should be on improving efficiencies.

Working with real customer portfolios, we see significant IM reduction by transferring just a handful of trades from one FCM account to an other.

We covered this in Optimizing Swaps Margin across Brokers and I would encourage you to read that.

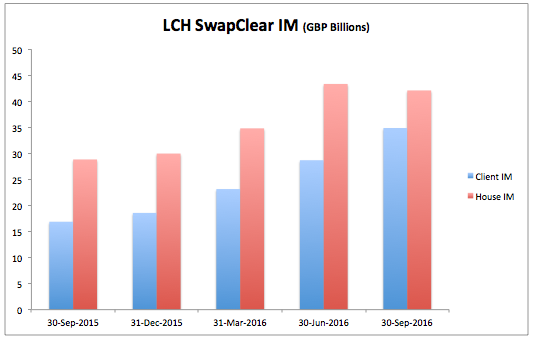

And a chart to show how client clearing has been the real growth story in the last year or two.

Showing that at LCH SwapClear Client IM was £35b on 30-Sep-2016 or 83% of House IM, having grown from £17b or 59% of House IM over the course of the year.

So very large amounts of Client IM that would benefit from IM Optimisation techniques.

Finally lets not forget that in either Sep 2018, Sep 2019 or Sep 2020, clients will also be subject to Uncleared Margin Rules and be required to post IM, so further opportunities for Optimization.

I plan to cover this and other aspects in future articles.