For all those Category 1 Covered Entities in the US and Japan, the following few days should be interesting with the introduction of Bilateral Margin Rules. For all entities not yet covered by the rules, you have some time on your hands.

And this time should be used wisely.

As a brief reminder, all covered entities will be obliged to exchange Variation Margin (VM) effective March 1, 2017, but there is a fairly generous timeline for Initial Margin (IM):

- Category 2: EUR 2.250 trn + : Sep 1, 2017

- Category 3: EUR 1.500 trn + : Sep 1, 2018

- Category 4: EUR 0.750 trn + : Sep 1, 2019

- Category 5: EUR 0.008 trn + : Sep 1, 2020

So what do you do if you are currently a Category 2 entity? Well, you can build out all of the calculations and plumbing, and get ready to fund all of the required collateral. Or, you can get busy and try to downgrade yourself to a Category 3 entity.

Put Your Sales Team To Work

The general premise here is that most Category 2 firms (between 2.25 and 3.00 trn EUR of bilateral notional) have a world of low hanging fruit they simply need to pick off of the tree. It’s a conceptually easy problem to solve. Because the bilateral margin phases are based on notional amounts, every trade cleared will help. You simply need to find all of your bilateral client portfolios that:

- Are clearing eligible

- Reduce your cleared margin requirements

This might sound easy, but of course most client portfolios will consist of a mix of eligible/non-eligible trades, and Sods law says that many of these portfolios will not benefit your cleared positions. But let’s try anyhow.

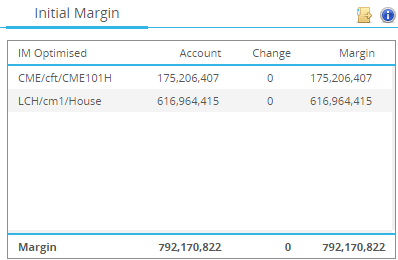

Let’s start with our sample banks CME and LCH cleared portfolios:

Showing:

- CME margins of 175 mm

- LCH margins of 616 mm

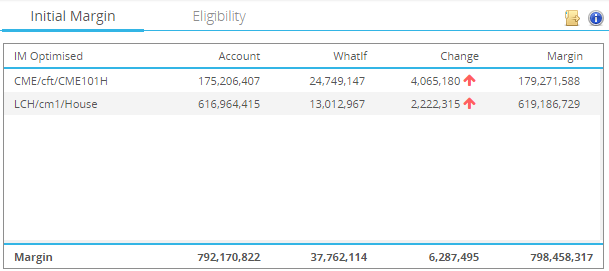

Now, let’s add a small client portfolio that has 20 trades in it, by uploading FpML or similar trade formats, and computing margin:

This tells us that both our CME and LCH accounts would be negatively impacted (margin increases) by asking the customer to backload. So, we could decide to give up and move onto the next client. Or, we can get a bit smarter.

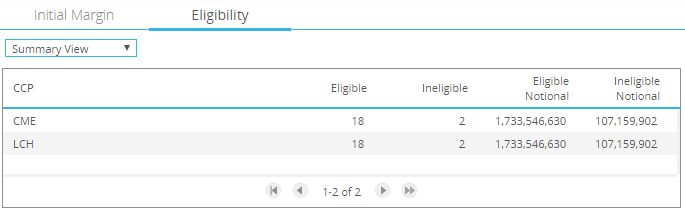

First, we need to determine, out of the portfolio of trades, just how many are clearing eligible:

So only 2 of the 20 trades are ineligible. OK fine, but we can also ask, if I happen to speak to this client, and I could ask him to backload one trade, which one would I ask for?

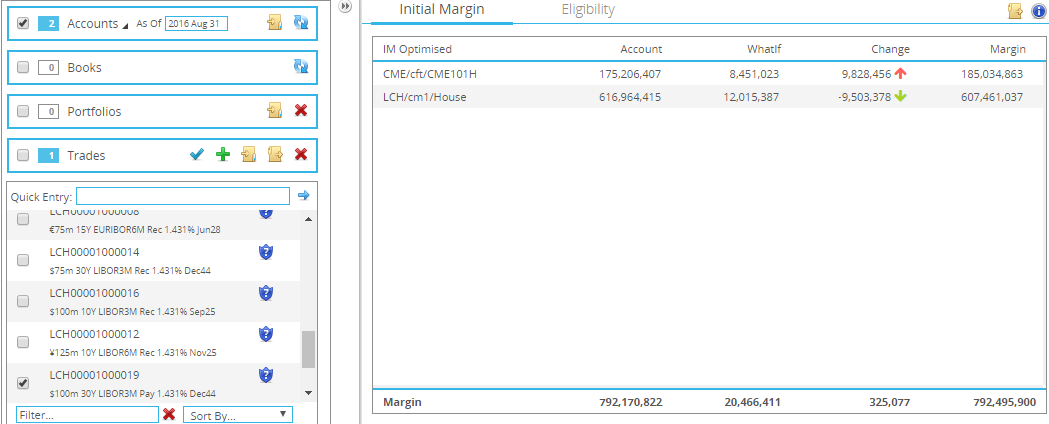

Of course you’ll get a unique answer for each clearing house. Assuming that LCH is where this particular client clears trades, we can look to optimize our LCH portfolio by asking for the best trade to backload:

This tells me that the single largest trade impact would be the $100m Dec-2044 payer, which would reduce my overall LCH margin by over 9mm.

Ideally however, I want to reduce as much bilateral notional as possible, while keeping the constraint of reducing cleared margins. Hence, I then ask for as many trades as possible:

This tells me that there exist 10 trades (out of 20) that meet eligibility requirements and reduce cleared margins. Adding any more of these clients’ trades would prove sub-optimal. If my client agrees to backload these 10 trades in this example:

- I can reduce my margins on the cleared side

- I can save over EUR 1bn of bilateral notional that goes towards the next tier.

1 billion might seem like a drop in the bucket when our bands are 750 billion in size, but this is a relatively small portfolio. Everyone has low hanging fruit out there.

Wash, rinse, and repeat for every client. This information should be at the fingertips of everyone who speaks to a client.

Fine Print

I should mention that these thresholds used to categorize firms by their outstanding notional (EUR 3 trn, 2.25, etc) is based on “aggregate month end average notional amounts” (AMEANA) in the months of March, April, and May of the relevant phase in year. So you really only have until March 2017 to have these numbers reduced.

Summary

There seems to be a lot of low-hanging fruit out there that can be optimized. If I were running a trading desk, I’d want each of my salesmen to have a list of backload-optimizing trades for each client, so that the next time anyone engages with them, we ask if they would like to clear the trades.

Of course, if you’ve followed any of our discussions on Margin Valuation Adjustment (MVA), you’d also be prepared to offer incentives to the customer to do so.

Ideally, everyone wins:

- The bank pushes out bilateral margin requirements (or reduces the more costly bilateral margin amounts)

- The client may see a benefit to their cleared portfolio, or may appreciate the incentives (or both)

- Regulators achieve their objectives of pushing more trades to clearing

It will be interesting to see if such portfolio maintenance operations such as this will impact cleared activity over the coming months.