- The VM Big Bang deadline is on March 1st 2017.

- We explain how a CSA governs Variation Margin for OTC Derivatives.

- ISDA are providing a Variation Margin protocol, allowing industry participants to efficiently amend their bilateral margin agreements (CSAs).

- We analyse what some of the changes could mean from a pricing perspective.

- Using a simple example, we highlight why the industry preference should be towards single (and fairly standard) CSAs governing both old and new trades.

Variation Margin

We have written a number of posts that help give you the low-down on the Uncleared Margin Rules (UMRs). For example here, here and here. In addition, I would recommend watching the series of (very short) ISDA videos to refresh your memory:

Changing Margin Agreements

The legal document that covers the exchange of margin on an OTC Derivative is typically the ISDA Credit Support Annex (CSA). This document defines the terms that govern the exchange of collateral, including but not exclusive to:

- Type of collateral acceptable – cash, bonds, liquid securities etc.

- Currencies – this can be single or a basket.

- Valuation and Calculation Counterparty – who will calculate and call the collateral amount. Normally one of the two counterparties to the trade (e.g. the dealer).

- When the collateral will move.

- Frequency of valuation.

- Independent Amount – effectively Initial Margin demanded in some trading relationships prior to the UMRs becoming effective.

- Substitutions – can the existing collateral be substituted with other eligible collateral?

- The Minimum Transfer Amount (MTA). Changes in the Mark to Market of the portfolio that are below this amount will not exchange hands.

- Interest Rates payable on the collateral held by the receiving counterparty.

The upcoming UMRs generally demand that eligible collateral is exchanged on a T+1 basis. This means that existing CSAs must be analysed to check that their terms are compliant with the new regulatory regime. ISDA has therefore enabled a “protocol”, which is described on their website as:

An ISDA protocol is a multilateral contractual amendment mechanism that allows for various standardized amendments to be deemed to be made to the relevant Protocol Covered Agreements between any two adhering parties.

I think that means the protocol allows multiple industry participants to consent to particular document changes as part of an efficient industry-wide review process. Sounds very sensible to me.

So, anyone wishing to continue to trade uncleared derivatives and who has to post margin as a result of the regulatory changes will have to go through this process. The protocol provides for three options:

- Amend method – take your existing CSA and make it compliant with the new rules.

- Replicate and amend method – take your existing (non-compliant) CSA and then change it so that any new trades after 1st March will be governed by a new, compliant CSA. Your old trades will stay on their old CSA.

- New CSA method – ISDA will generate a new CSA based on the protocol process above for all of your new trades. It looks like you can either have a new CSA with your existing Master Agreement or go the whole hog and create a new Master Agreement too. The intricacies of this are a bit beyond a blog post I feel.

Onto the Numbers

I haven’t yet seen any discourse about which of the 3 options are sensible. So I thought I would put some numbers on it. My main thoughts are:

- Should your CSA apply to both legacy and new transactions, or do you want them segregated?

- If they are segregated, what happens if you move collateral for the same Mark-to-Market moves at different times?

- Does it make sense to have a Minimum Transfer Amount?

For this analysis, I turn to CHARM, and use our VM Buffer sizing tool. If you recall from Amir’s blog, this looks at a given history of market moves to calculate the size of margin that is sensible to keep on-hand at a given confidence interval. Just in case we have one of those Brexit margin calls….

For this exercise I will take a single swap – a pay fixed 10y USD swap in $100m. Over the past two years, CHARM shows us our daily VM calls:

Showing;

- Over the past two years, the maximum daily swing in Mark to Market that we have seen is $2.891m. This was a loss.

- The maximum gain was $2.784m. So fairly symmetrical.

- As expected, many of the movements are clustered around zero….

- …but what are the chances of a large negative move on day 1 being followed by a bounce-back and a large positive move on day 2? Let’s look at the numbers.

T+1 versus T+2 Moves

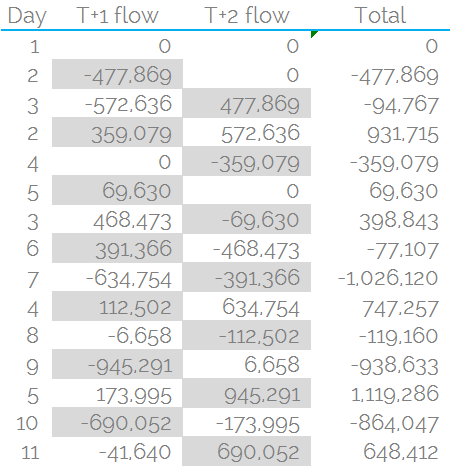

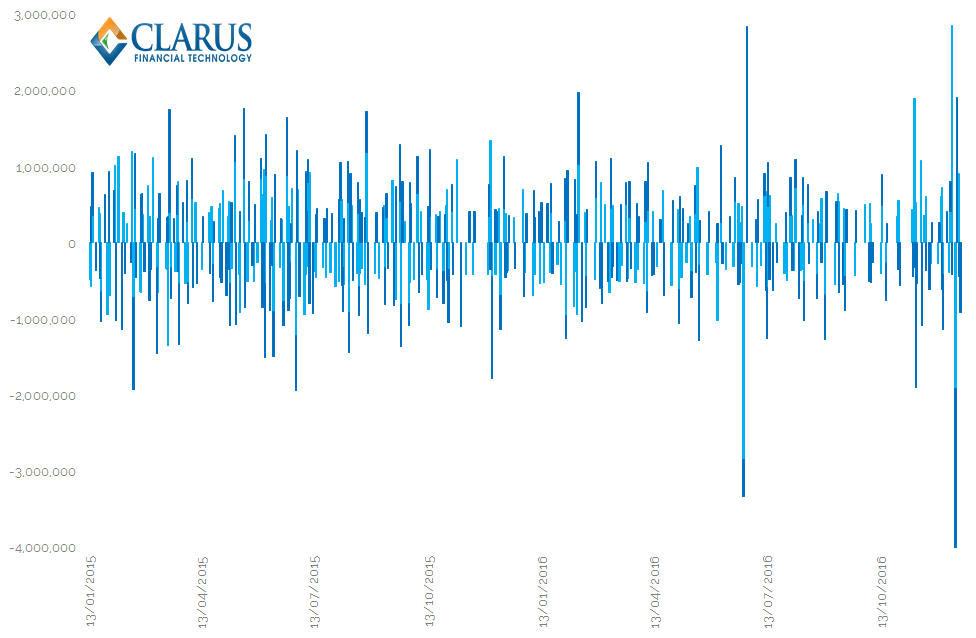

If you choose to transact your new transactions on a new CSA, how might a “hedged” portfolio look? Let’s imagine a very unlikely situation – you have an old 10 year receive fixed USD swap hedged with a new 10 year pay fixed USD swap. The old one has collateral called on a T+2 basis, and the new one needs to be compliant and exchange collateral on a T+1 basis. Your daily moves will be out of sync by one day (see table).

If you choose to transact your new transactions on a new CSA, how might a “hedged” portfolio look? Let’s imagine a very unlikely situation – you have an old 10 year receive fixed USD swap hedged with a new 10 year pay fixed USD swap. The old one has collateral called on a T+2 basis, and the new one needs to be compliant and exchange collateral on a T+1 basis. Your daily moves will be out of sync by one day (see table).

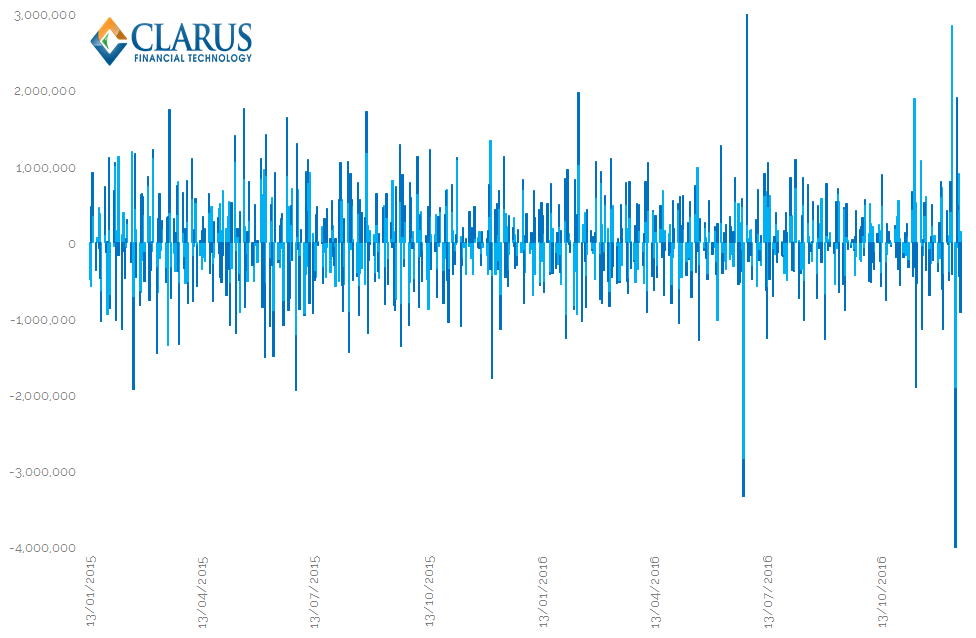

This “hedged” position (carrying zero market risk) can have some pretty wild swings in collateral as a result:

Showing:

- A maximum outflow of -$4.782m! Yes, that is right. Hedging a deal under a T+1 CSA with a T+2 CSA doubles the amount of collateral you might have to post! This is particularly likely if you have a “bad mark” on a single day of trading (causing a “whip-saw” of Mark-to-Market).

- A maximum inflow of $2.847m, which is more in-line with an unhedged position.

- It is a very noisy chart – there is a lot going on here for a market-neutral package.

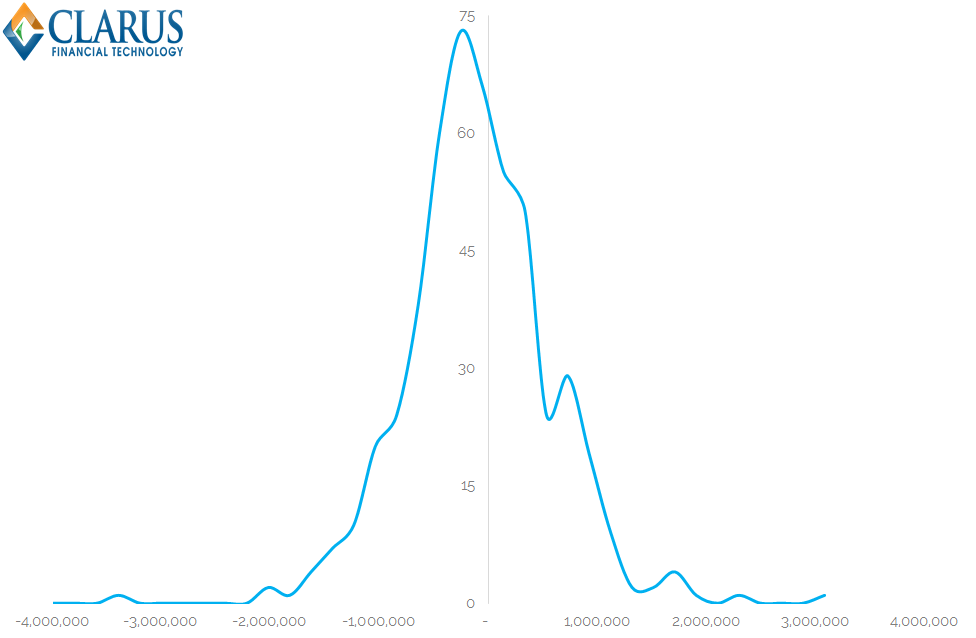

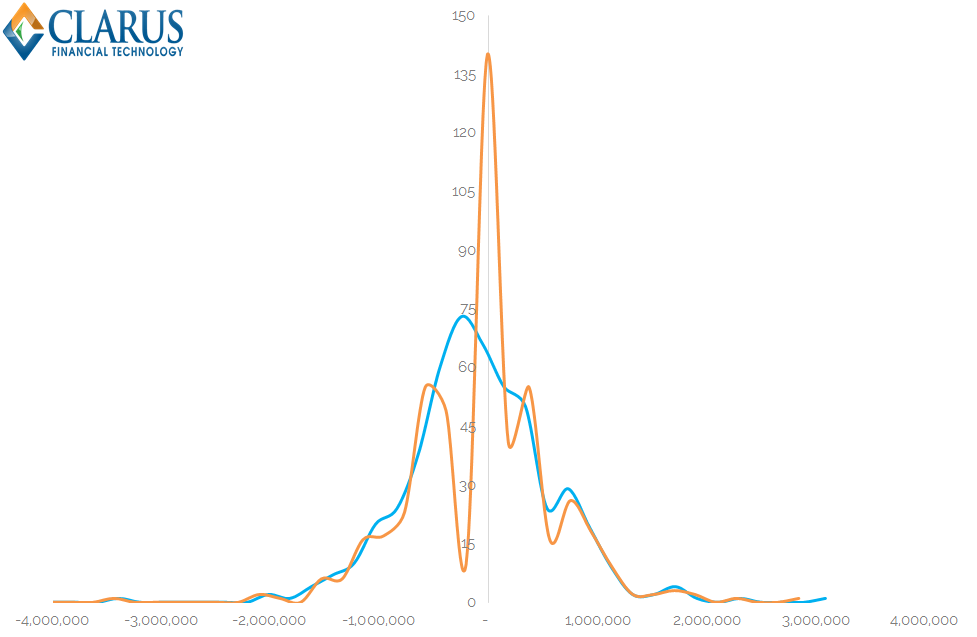

Intuitively, we would expect most of these moves to be clustered around zero. Let’s have a look at a histogram of moves:

- Generally symmetrical about zero

- A long negative tail with 3 very large calls

- Two large positive calls on a smaller tail to the right

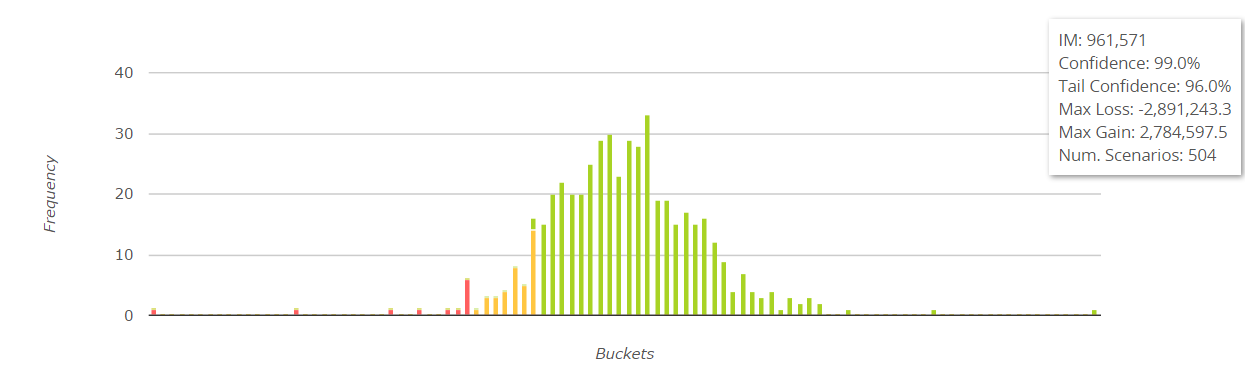

- Out of 504 observations, 438 are under $1m in size, but 310 calls are greater than $250,000.

Making daily collateral postings on a hedged trade is not a great position to be in! It increases operational complexity, funding costs and introduces potential pricing complexities.

Minimum Transfer Amounts

It is highly unlikely that I am the first market participant to recognise this complexity of hedging across multiple CSAs. In light of this, it is unsurprising to see that Credit Support Annexes have a provision for a Minimum Transfer Amount – i.e. if the daily swing in mark-to-market is too small, let’s just let that one pass and wait for it to get larger. This reduces operational complexity.

The New CSA under the ISDA protocol proposes an MTA of $250,000 to gain regulatory compliance with assorted jurisdictions around the world.. For the hedged package above, we may therefore expect our risk neutral package to now only have 383 collateral calls (out of a possible 504) i.e. those larger than $250,000.

However, the MTA does not act at a net level, but on each individual trade. The collateral calls are therefore somewhat different when applying an MTA at an individual CSA level:

Showing;

- A less dense blur of lines – there are indeed fewer collateral calls overall than without MTAs in place

- However, the general picture is still quite daunting. We still have very large collateral calls and they are still fairly frequent. Out of a possible 504 days, we have collateral movements on 379 of them.

It is therefore worth comparing exactly what has changed compared to having no MTAs:

Showing;

- Across 500+ observations, the distribution of calls are different with and without MTAs.

- The good news – there is a much higher peak at zero for the trades with an MTA.

- However, we have a few annoying dates that have net collateral calls lower than the MTA threshold (due to one positive, one negative).

- And from a pricing perspective, we still end up with the tail events – effectively having to fund meaningful amounts of collateral for a position that serves us no purpose.

Overall, I’ve been a little surprised at the magnitude of the net collateral calls, even with MTAs in place. Our CHARM users could use the above profile to calculate the historic funding costs that they will have incurred, putting a real world number on this issue.

To answer my original questions:

- Should your CSA apply to both legacy and new transactions, or do you want them segregated? You really want one CSA to govern all of your trades. Based on this analysis, segregation is a bad idea.

- If they are segregated, what happens if you move collateral for the same Mark-to-Market moves at different times? You end up with large net collateral movements that will introduce friction to the business and probably end up attracting some type of funding charge.

- Does it make sense to have a Minimum Transfer Amount? Probably not if you go down the multiple CSA route. It does reduce the number of movements, but it is a not a catch-all solution.

For now, I can only conclude that it is a dangerous assumption to leave legacy trades on different CSAs to new trades. Food for thought whilst the industry goes through their preparations.

On a final thought, the changes to CSAs considered here are relatively simple and should affect both sides of a trade equally. However, there are several elements of “optionality” in old CSAs that are very difficult to value. These include switch options between currencies, negative floors and trying to value a basket of eligible collateral. These intricacies are bound to introduce frictions to the re-papering exercise.

I cannot help thinking that rather than trying to monetise this optionality, the preference for the industry should be to make the markets operate more efficiently and transparently. In the long-run this should increase liquidity, decrease transaction costs and improve relations between clients and dealers.

In Summary

- The upcoming VM Big Bang will involve a large re-papering exercise to ensure documentation for new trades will be regulatory compliant across a number of jurisdictions.

- Having looked at a hypothetical example, it can be a dangerous decision to just “leave this to the lawyers”. Risk neutral packages that exist across different CSAs can result in high funding costs, operational complexity and reduce netting.

- Our example suggests that it could be a dangerous decision to leave legacy trades under old CSA agreements. Bifurcating portfolios like this will likely lead to an increase in collateral calls.

- This short blog only touches on the overall issue. There will be even more complexity in juggling T+1, T+2 and T+x CSAs, coupled with the decision to collateralise in cash or securities. Repo costs are therefore another input that we could model in the future for real world portfolios.

- Our analysis is powered by CHARM, our risk and analytics engine. Please contact us for a demo.