- Ameribor is an index of overnight unsecured lending taking place across the CBOE platform AFX.

- It is mainly concerned with the interbank market between smaller, regional US banks.

- We take a look at the rate versus Fed Funds and some possible uses.

Introducing Ameribor

I will try to do Ameribor justice in this post. But it is sometimes best to go to the source, so if you’ve never seen Richard Sandor speak at a conference, I advise you to check out his introduction to Ameribor below:

What is Ameribor?

From Ameribor.net, we can distill the definition of Ameribor as;

Unsecured overnight lending taking place across the American Financial Exchange (AFX).

Ameribor.net

From that, it is probably fitting to name what this interest rate is NOT first.

- This is not LIBOR.

- It is not SOFR.

- It is not Fed Funds.

- So far, it is not a Risk Free Rate either.

What it is;

- Overnight loans from “small and mid-sized banks, broker-dealers, insurance companies, private equity firms, hedge funds, FCMs, asset managers and finance companies.”

- These loans are transacted across a CBOE platform called AFX.

- The loans are unsecured.

- The volume weighted average of these overnight loans is calculated.

- The rate is published each night by CBOE.

- From all of the materials, I think the rate will be limited to USD for the time being. I cannot see these smaller financial players being active in many other currencies?

- The underlying transaction data is also made available according to the methodology (although I couldn’t easily find this on the website).

- Whilst there is passing mention about 1 month and 3 month terms, the headline rate is an overnight tenor.

What problem does Ameribor solve?

With so many reference rates and so much press about RFRs around, it might be surprising to start talking about a potential competitor rate.

But I think Ameribor is designed to be more of a complement to existing rates rather than a competitor rate.

It is different because;

- Unlike USD LIBOR, it is 100% based on transparent transactions.

- Unlike USD SOFR, it is not based on Repo transactions. SOFR is a secured overnight rate; Ameribor is unsecured.

- USD Fed Funds includes Eurodollar transactions (i.e. offshore). Ameribor only has on-shore transactions by design (i.e those executed subject to the standardised loan terms of the AFX exchange).

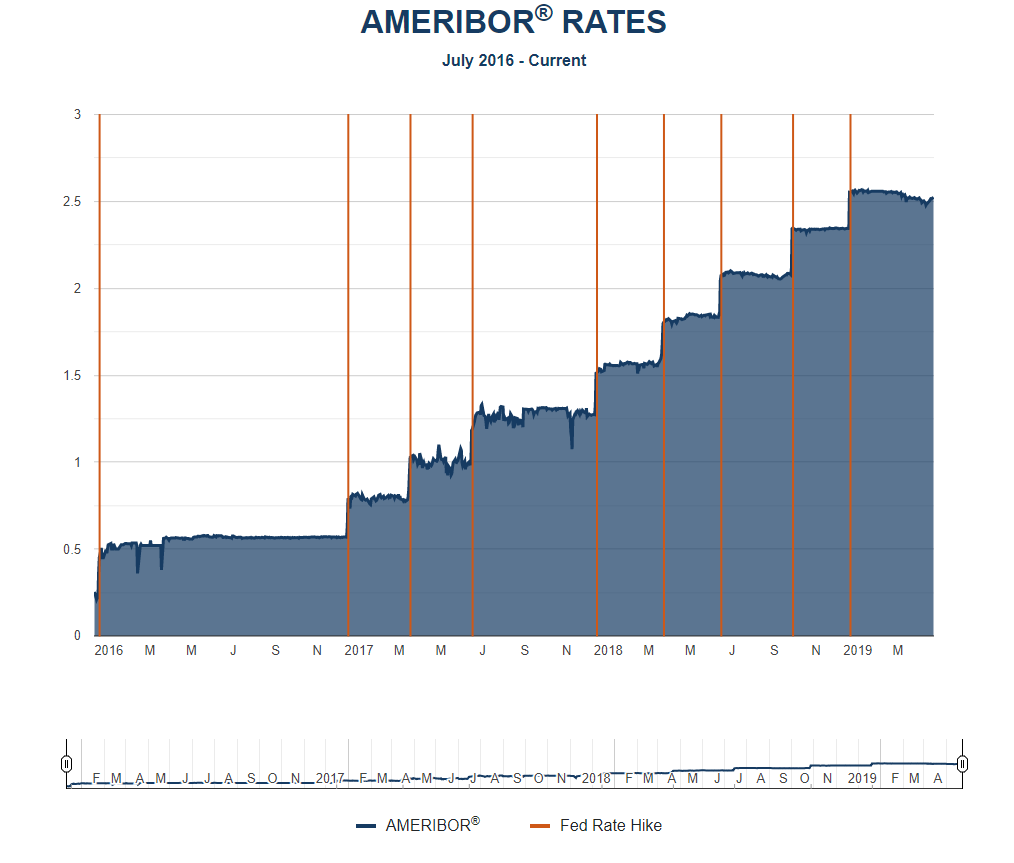

How has Ameribor Performed?

Courtesy of free registration on Ameribor.net, we can see the price history of Ameribor. Considering the volumes are pretty low (see below), the benchmark has been stable and predictable:

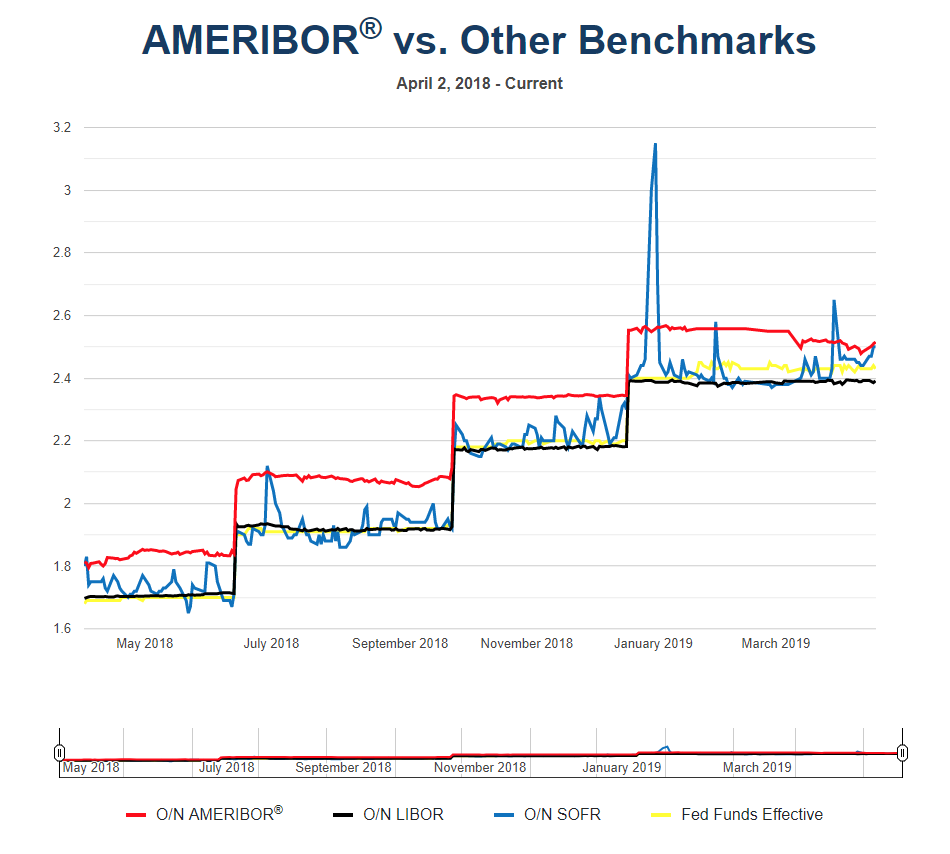

Possibly more relevant, however, is how Ameribor has performed relative to the other benchmarks:

Showing;

- Ameribor in red. It is pretty stable between Fed Dates.

- It is higher than both Fed Funds and O/N Libor.

Both Fed Funds and Ameribor are unsecured rates, so I wanted to do some analysis into their relationship.

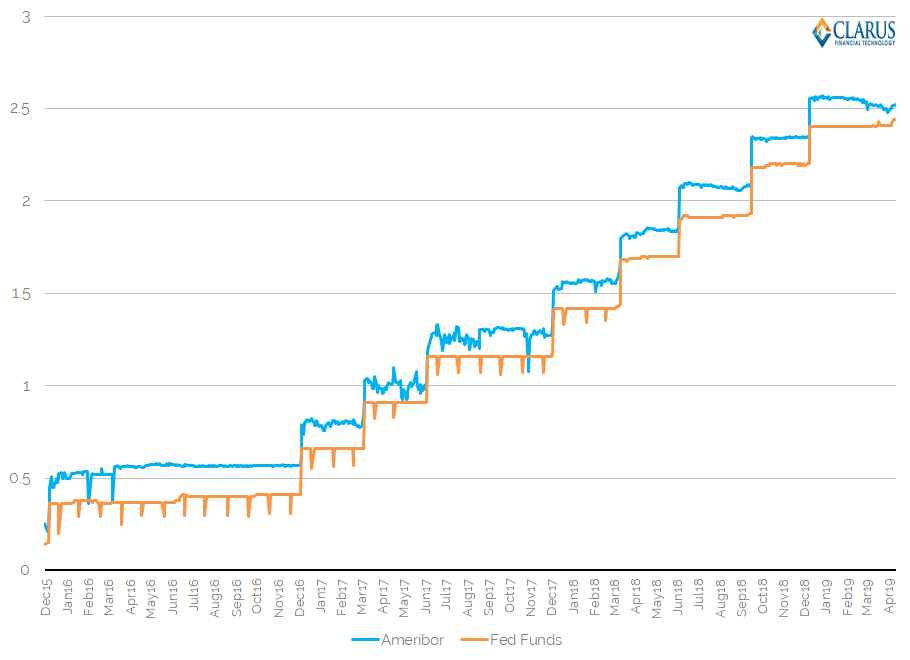

Ameribor vs Fed Funds

Having downloaded the Ameribor rates here and the Fed Funds rates here, I see the following time-series since 2016:

Showing;

- The Fed Funds rate has displayed a rhythmic heartbeat pattern for some time. The rate dips (by about 9 basis points) on each month end. This behaviour has virtually disappeared this year.

- This is news to me. I’ve noted the EONIA heartbeat previously but I didn’t know it existed in USD as well.

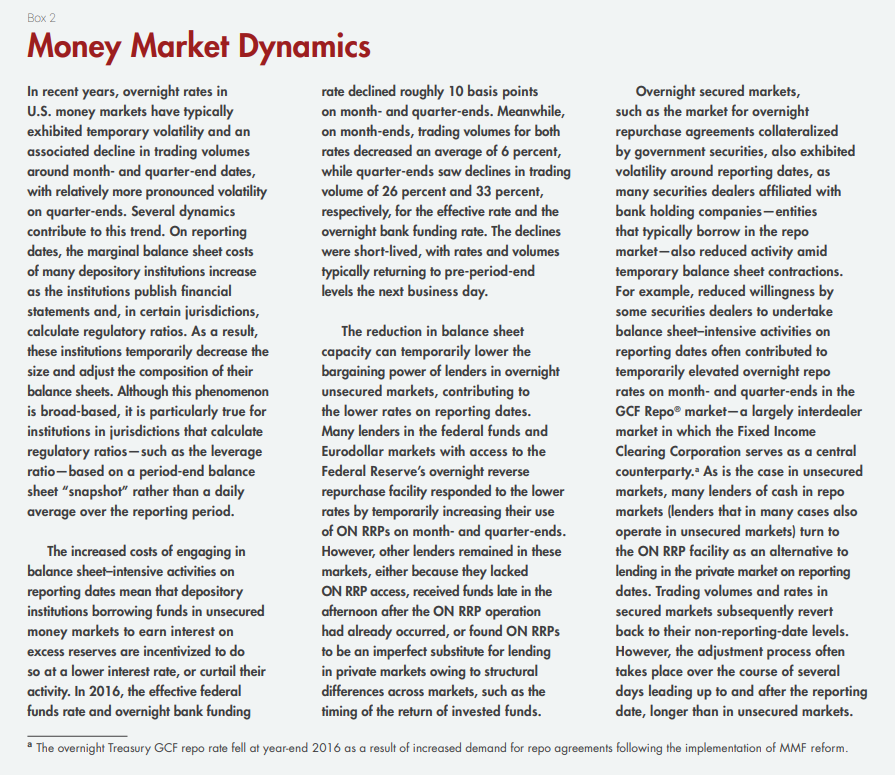

- Fortunately, the New York Fed has a great explainer for this behaviour. The text below explains that it is mainly caused by some jurisdictions demanding regulatory ratios (i.e. capital vs exposure measures) based on period-end balances rather than averages over the reporting period.

Whilst EONIA still showed this heartbeat pattern even with averages over the maintenance periods, it is exacerbated when it is a point-in-time calculation. Interesting stuff, particularly as the text above also explains the behaviour we see in SOFR rates. It should be required reading these days!

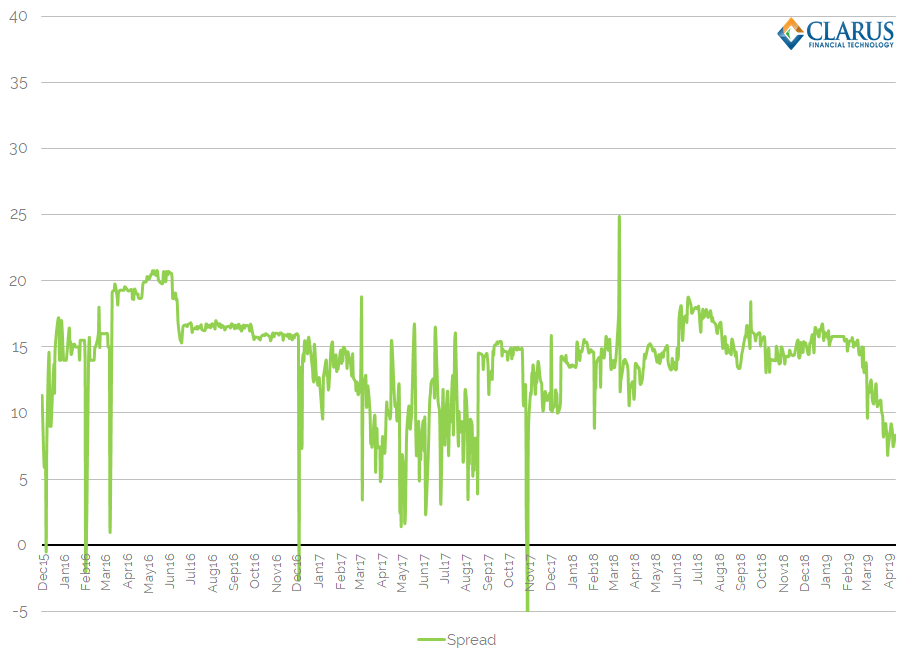

The Spread

Now that we know the cause of the Fed Funds month-end volatility, it is worth noting how eerily constant the Fed Funds rate has otherwise been. For 59 fixings in a row (excluding month/quarter/year-ends), from 20th Dec 2018 until 19th March 2019, the Fed Funds rate fixed at 2.40%.

This is unusual and doesn’t really feel like a “market” rate any more.

Ameribor is more variable.

This means it exhibits a somewhat volatile spread to Fed Funds:

Showing;

- Excluding month ends, the spread has ranged from -8.5 basis points to 24.8 basis points.

- However, in 2019, now that volumes are larger (over $1bn a day, see below), the spread has been more stable.

- In 2019, the spread has averaged 13.3 basis points, with a range of 10 basis points.

- It is interesting to see the spread has contracted substantially to Fed Funds in the past two months (i.e. during March and April 2019) to now rest in single digits.

Volumes

Finally, we must mention volumes:

- Ameribor is based on a daily average of $1.452bn as of 29th March 2019.

- Fed Funds is based on a daily average of $71.95bn during March and April 2019.

That is a pretty big gulf in volumes that Ameribor needs to work on closing. The growth rate of Ameribor volumes has been impressive, but it still has a long way to go. Check out Richard Sandor’s post on Linkedin for some more numbers.

Uses

So what is the point of Ameribor? Where does it lie in the greater scheme of RFRs and benchmark reform?

That is a tough one to answer. From the research I did for this blog I am left thinking that:

- Volumes need to continue to increase to give Ameribor more relevance to the broad market.

- As a reference rate for lending, it must be useful for the banks who are active in the AFX market.

- As an overall market rate, could Fed Funds be expanded to include the AFX transactions? Fed Funds is calculated as a volume weighted median (order the transactions from lowest to highest rate, and identify the rate associated with the trade at the middle of the volume), so the $1.45bn a day is unlikely to shift the needle substantially.

- The biggest difference in Ameribor versus Fed Funds (ignoring month end behaviour) might be the inclusion of “government-sponsored enterprises” in Fed Funds data. My working assumption is that this is SallieMae/FreddieMac activity (let me know in comments if I am wrong). This might be very large by volume (I have no idea) and hence reduce the credit spread inherent in Fed Funds. Ameribor might be more representative of a broad “bank credit” market.

- How much value is there in the underlying Ameribor ecosystem, which standardizes loans and their documentation? This could certainly help the cash market during Libor fallbacks.

Summary

- Ameribor currently serves a very specific purpose – to measure unsecured overnight lending between regional banks in the US.

- It is therefore beneficial to the broader market to have Ameribor as a credible index.

For me, the Ameribor index also highlights that volatility in SOFR and Fed Funds isn’t inherent to bank credit and so could easily be fixed.

Why don’t regulators just assign each bank a random date between the 1st and 28th of each month to report regulatory ratios? Wouldn’t that remove the market behaviour that we saw at the end of 2018?

ETA 12th June 2019: Even better, a random average period. That should completely remove any herd behaviour.

As more banks seek a LIBOR substitute, AMERIBOR will increasingly be seen as the best index to give the banks the combination of things they need: reflective of trends in interest rates and containing the input of credit risk that SOFR lacks. That means the spreads on AMERIBOR will behave much more closely to the old LIBOR than will a secured rate like SOFR.

You are right that the government sponsored enterprises are Fannie/Freddie/Sallie but they are only lenders in the market so it does not explain the credit element as it is banks who are borrowing. I urge you to read the analysis of Zoltan Pozsar from Credit Suisse who explains in his Global Money Notes (GMN) the full workings of US Money Markets:

https://plus.csintra.net/ECP_S/app/container.html#loc=/MENU_RESEARCH_DETAIL?ldocid=1080850531

This is the link to the latest outing of his GMN series but the relevant info will be earlier in the series. Essentially though you need to ignore whether the transaction is secured or unsecured and focus on whether it is a lending or borrowing market for the supply of liquidity.

As a quick update, a reader has been in touch to advise that it is not Freddie/Fannie who are active in Fed Funds, but rather the FHLBs (Federal Home Loan Banks). Many thanks to Jumby and our readers for putting me straight. We will follow up with a more in-depth look at Fed Funds in a future blog.

Very helpful post. Look forward to the FF dive.

I think above link may not work.. but this might:

https://plus.credit-Suisse.com/r/V7eBCg2AF-Yoi3