- Europe is deciding upon the Risk Free Rate to use in the future.

- There are three candidate rates – two are secured, and one is unsecured.

- We look at the details of the fixings and the volume data.

- There is an on-going public consultation which we would encourage our readers to respond to.

Background

Back in September 2017, the ECB announced that it will “develop a euro unsecured overnight interest rate”. Since then, this new rate has been christened “ESTER” (Euro short-term rate).

I (somewhat naïvely) assumed that ESTER would become the Risk Free Rate of choice in the Euro area. But hold on! The European Working Group on RFRs has just launched a public consultation to choose the best RFR for the Eurozone.

Let’s take a look at the candidate rates.

Criteria

There are three candidate rates. They will be “judged” versus the criteria outlined in April:

- Underpinned by broad-based and reliable market data.

- Representative of arm’s-length risk-free borrowing costs.

- Reactive to changes in policy rate.

- Clear and transparent measure of underlying interest.

- Transaction based where possible.

- Market data defined and understood.

- Market data reliable and accessible.

- Determination methodology clear and transparent.

I think these are the 8 criteria worth bearing in mind (there are 12 in total). The consultation document includes a history of the three rates over time:

Let’s go ahead and take a look at the three rates under consideration.

ESTER

ESTER sat alongside Euribor, EURONIA, EONIA and LIBOR as possible unsecured RFRs.

What we know about ESTER so far is that:

- It is not published yet. The ECB has stated that it will be “produced before 2020”. That doesn’t give us a lot of time to transition the whole swaps market to it if Libor (and Euribor and Eonia) may cease to exist in 2021. However, there is a history of the proposed fixing already available.

- It will be based on daily money market statistical reporting (MMSR) data provided by the 52 largest euro area banks. These are:

- Full details of the statistical reporting underlying these transactions can be found here. The information has been collected daily since 2016, and is split into Secured, Unsecured, FX and OIS.

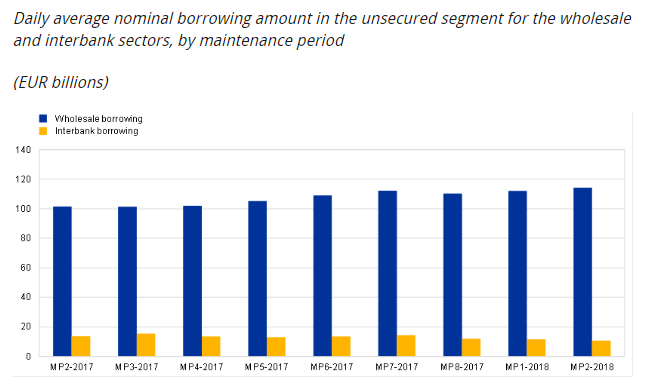

- Reports are currently published by the ECB using this data, covering each Maintenance Period. For example:

Showing;

Showing;

- Daily averages of unsecured lending during each six-week maintenance period.

- We can see that volumes are increasing recently, and are now €114bn.

- Not all of these are overnight transactions – they cover all tenors.

- The ECB state that average daily volume for the proposed ESTER fixing was €29.8bn between August 2016 and January 2018.

- The data is downloadable via the ECB Statistical Warehouse.

- Further details on ESTER can be found in the Second Consultation from March 2018. For example, the ECB describes why transactions of less than €1m are to be excluded from the final calculations.

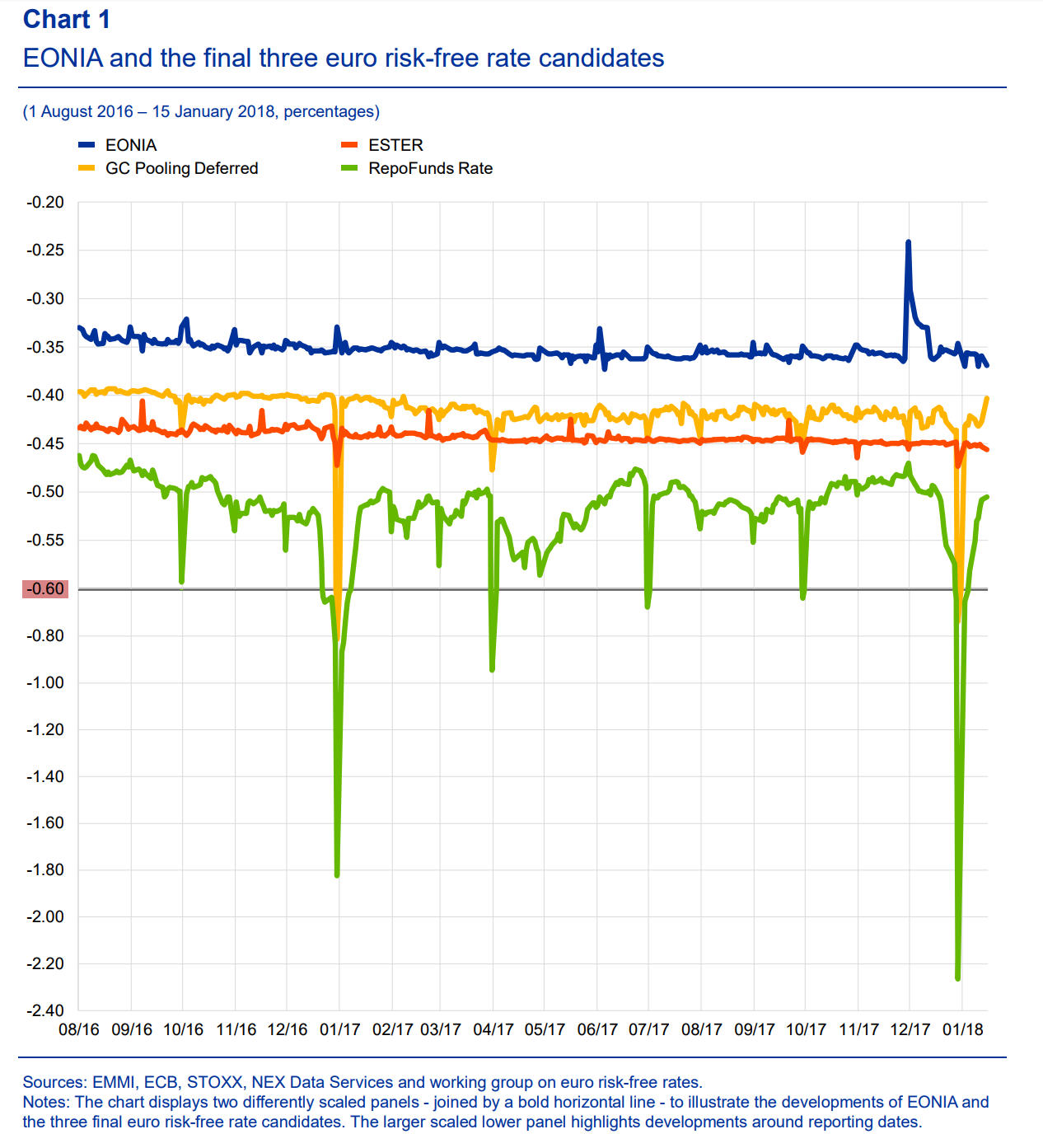

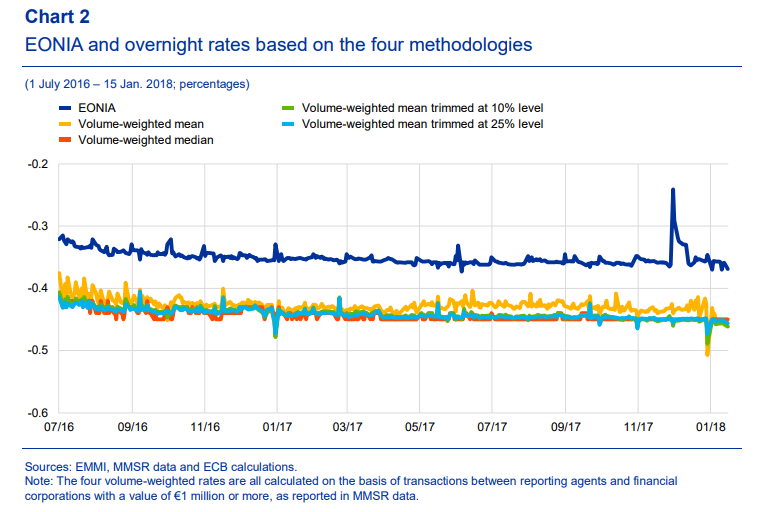

- The final calculation will be a volume-weighted trimmed mean, with the trimming level set at 25%. You can see how this compares to EONIA below:

Showing;

- An average spread to Eonia of 9.1 basis points (always lower).

- A maximum spread of 21.5 basis points.

- Eonia’s typical “heartbeat”, where it spikes at regular Maintenance Period start dates due to reserve requirement front-loading, is not so apparent in ESTER.

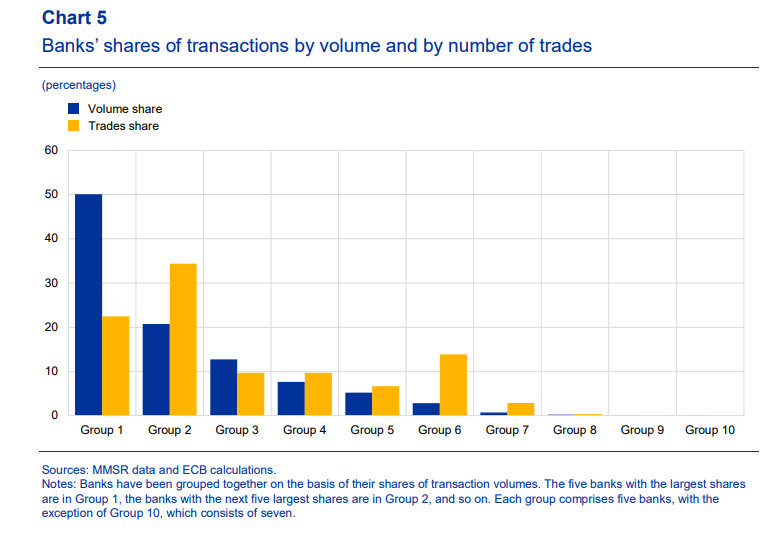

Finally, it is worth noting that the five largest banks in the ESTER data pool have tended to account for 50% of notional volume:

On ESTER, I think that is pretty much it. It seems a strong contender to me!

On ESTER, I think that is pretty much it. It seems a strong contender to me!

STOXX GC Pooling Indices

The first of the secured rates under consideration is published by STOXX, based on repo transactions cleared through Eurex. The Working Group has considered the widest possible source of transactions for this index, which is called the “GC Pooling Deferred”. This includes repos that are transacted for value tomorrow, as well as one day tenors covering tom/next and spot/next from previous days trading.

As with SOFR in the US, the transactions underlying the index are general collateral repos, defined thus by Eurex:

There is an in-depth look at the index here. Of note:

There is an in-depth look at the index here. Of note:

- The repos are centrally cleared, anonymously transacted and cover 14,000 ISINs of ECB eligible High Quality Liquid Assets (HQLA).

- 118 active participants.

- 43% of volume via top 5 participants.

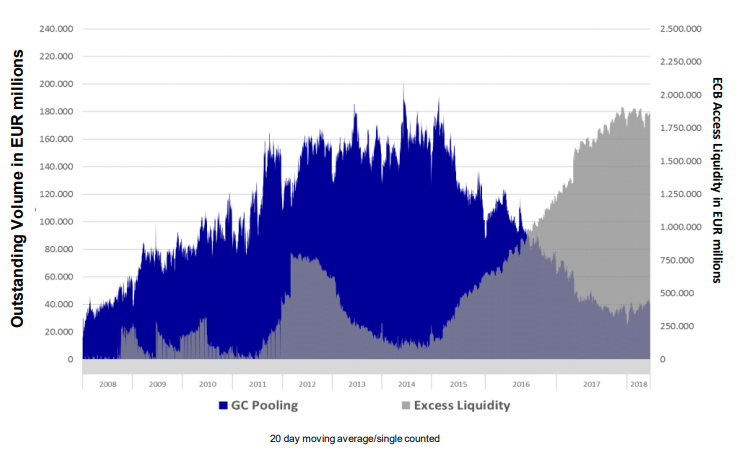

- Volumes are strongly correlated to Excess Liquidity at ECB (correlation of -90%!):

- Volumes have started to increase again in the past 18 months, even as EONIA volume has continued to dwindle.

- Average Daily volume €8.9bn.

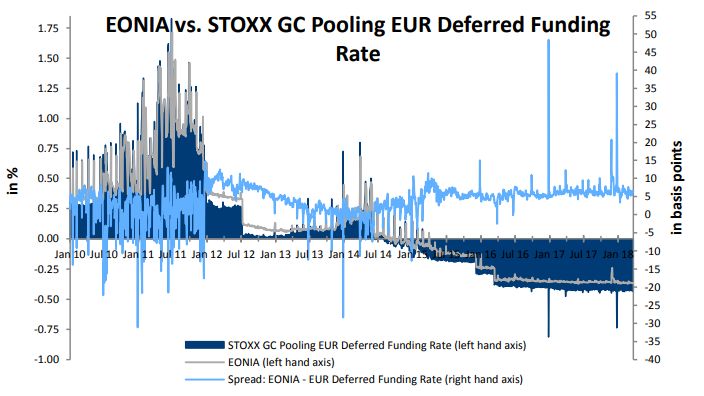

- The average spread to EONIA has been 6bp since January 2015:

From my brief look at this, the STOXX GC rate performs particularly well during times of stress, when central clearing is most attractive. I’m surprised that volumes are not significantly higher than EONIA. For example, in the US SOFR volumes are much higher than Fed Funds.

RepoFunds Rate

I recently came across this fixing when I was looking at collateral optimisation (contact us to see this in CHARM). Their website is very transparent, and well worth checking out:

The index is based on centrally cleared repos executed across both BrokerTec and MTS (RepoFunds Rate is produced by NEX and BrokerTec is part of NEX. MTS is part of LSEG).

NEX produced an in-depth look at the fixing for the Working Group. Of note;

- Based upon transactions versus sovereign government bonds. They may be either GC or versus specific bonds.

- 25% of trades are filtered to avoid “specials” having too much of an impact.

- The index is a Volume Weighted Average Price (VWAP) on the remaining trades.

- 80 trading participants across 9 countries, but 34 are in the UK…..

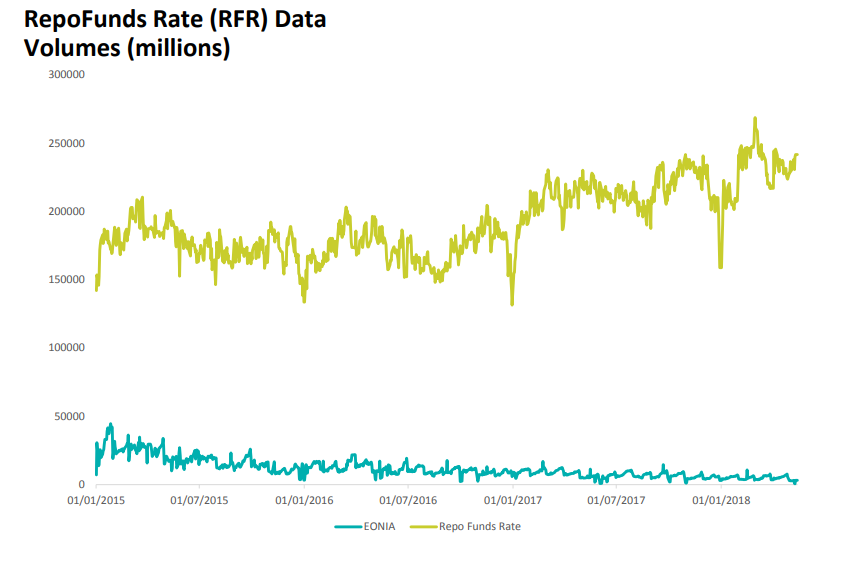

- Impressive volumes:

Showing;

- Volumes are €200.6bn on average per day for the fixing (25% are trimmed).

- You might need to remove 18% of that volume (~€43bn) as French repo trades are calculated as a spread to Eonia. That must change in the future I guess?

- I think it’s a shame they don’t split the volumes by BrokerTec and MTS volumes. What if MTS pull out of the licensing agreement?

- That said, just look at those volumes! It’s huge…..much more in line with SOFR volumes.

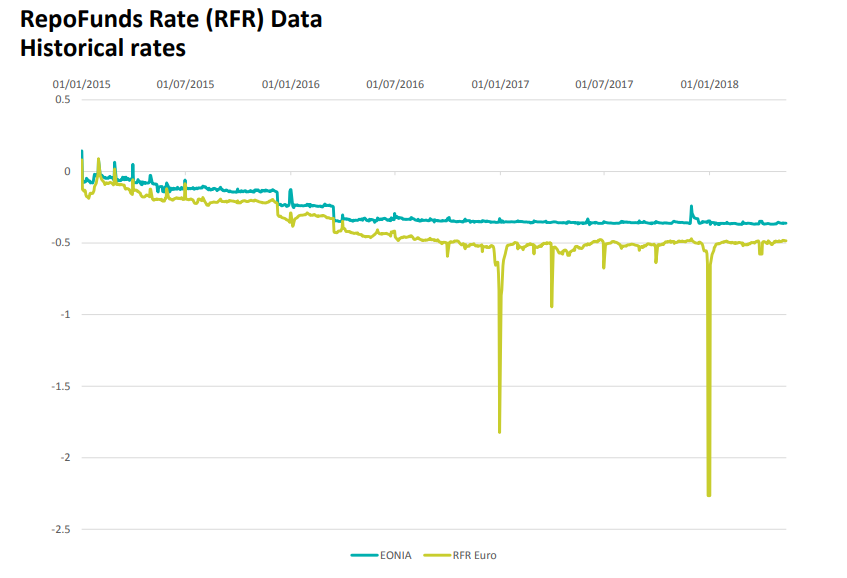

Of course, we need to see the history versus EONIA as well:

Which does highlight why some people do not like secured rates:

Which does highlight why some people do not like secured rates:

- The turn of year effect is huge compared to EONIA. Something like 150-200bp lower than a “normal” fixing. Smaller spikes lower are also seen at quarter ends – I guess due to “balance sheet dressing”.

- I think the BoE witnessed something similar when looking at SONIA versus the LSEG secured rate (£SONET). The quarter-end volatility was not attractive for a “risk free rate” as it loses all relation to the central bank policy rate.

In Summary – Is Size Important?

So there you have it for a brief run-down of the three rates: ESTER vs GC Pooling vs RepoFunds.

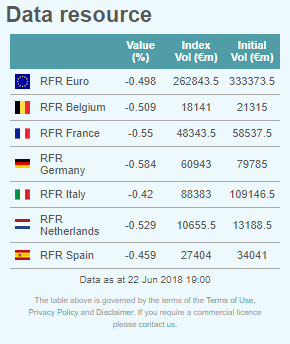

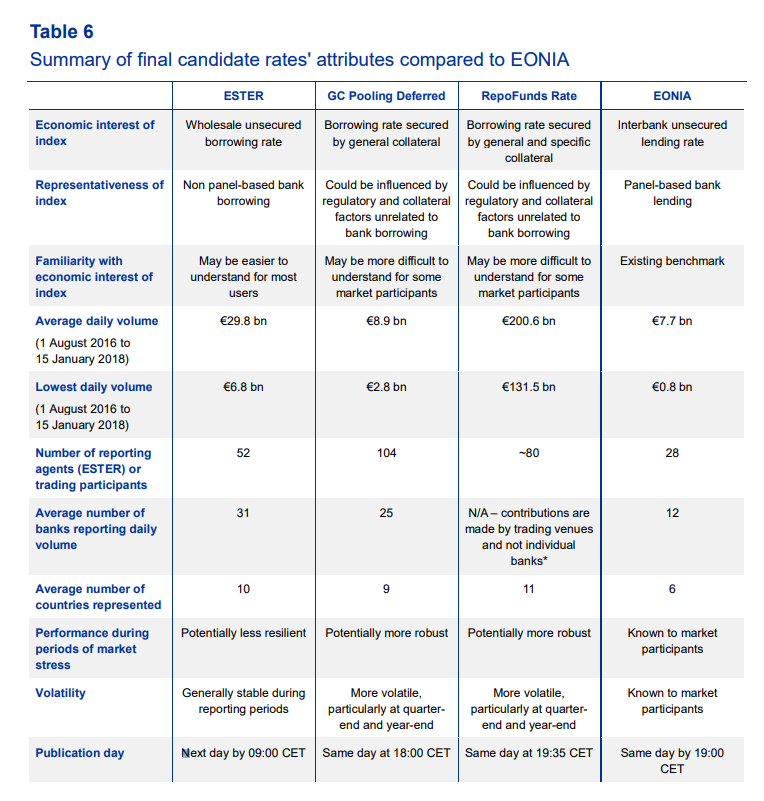

Here are the key facts in table form from the ECB:

Going purely on the numbers:

- SOFR (a secured rate) has volumes approaching $800bn per day. I am sure this was a huge factor in choosing this rate as the RFR in the US.

- SONIA (an unsecured rate) now has daily volumes around £50bn.

- ESTER (an unsecured rate) has volumes of ~€30bn.

- STOXX GC Pooling (a secured rate) has seen volumes as high as €60bn, but averaged €9bn.

- RepoFunds Rate (a secured rate) sees volumes of €200bn.

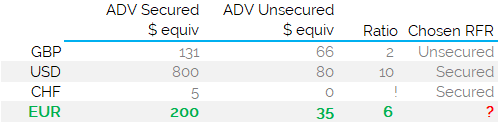

Therefore, size may be a driving factor in deciding whether Europe should go with a secured or unsecured RFR. However, the choice isn’t clear-cut. Look at the relative sizes of secured vs unsecured in four different markets. They are all very different!

The Working Group needs to decide whether European money markets are like the UK. Therefore the quarter end volatility of repo rates may be less attractive compared to a stable secured market with okay volumes.

Or, with EUR and USD swaps markets being roughly equal sizes, should we look to the US? The largest possible pool of transactions for a European RFR are in secured rates.

The market will help decide – responses to the consultation are due in by 13th July, and can be submitted here.

Please feel free to reach out to Clarus if you need any data or help with a submission. We’ll go through our data to see if there is anything further that we can add to the debate.