- ICE are planning to change the calculation methodology for LIBOR.

- LIBOR is not currently (April 2018) transaction based – it remains a survey.

- ICE would like to change this so that it can be based on transactions, but not all Libor tenors see transactions every day.

- There is therefore a new suggested “waterfall” methodology to allow all tenors to be calculated.

- ICE have published data comparing LIBOR using both new and old methodologies.

What is LIBOR?

Um, you might be on the wrong blog. Zerohedge is over here ->.

Okay, we all think we know what LIBOR is. But amongst the crises, the law-suits, the manipulation, the thousands of words written about it, it is pretty easy to forget that LIBOR does have an actual definition.

Kudos to ICE for a most excellent website, that I won’t really be able to do justice to on a short blog. So please check out “Calculating ICE LIBOR” from ICE here.

My short summary of the current LIBOR definition is as follows:

- Banks are asked: “At what rate could you borrow money at 11am London time?” (I paraphrase…).

- ICE then throw away the highest 25% of rates and the lowest 25% of rates – i.e. if 16 banks send a rate, ICE use the “middle” 8 rates that have been submitted.

- The arithmetic mean (the “AVERAGE” function in Excel) is then calculated and published.

The ICE LIBOR Roadmap

It should surprise nobody reading this blog that there is a strong preference to transition towards a transaction based methodology for LIBOR. Instead of answering a question from ICE, banks should send proof of eligible trades to ICE and ICE can go off and calculate the rate using whatever methodology they deem appropriate.

This only works if there are actual transactions though. An existential problem for LIBOR is that very little (i.e. close to zero) trading activity takes place in some LIBOR currencies in some tenors.

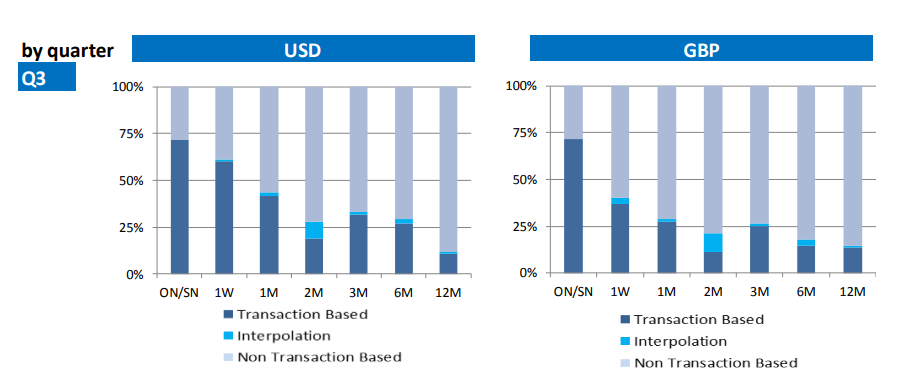

ICE themselves have made this explicitly clear in their roadmap document. Their charts nicely illustrate this point (and are available for more recent periods here, under “Quarterly Volume Reports”).

Showing;

- For USD and GBP Libor submissions during Q3 2015, the percentage generated via transactions, interpolation or not based on transactions at all.

- The results are both currency and tenor dependant.

- Transactions are far more common at short tenors (less than 1 month) than longer tenors.

- Checking versus the most recent report for Q1 2018, the charts have been consistent over time.

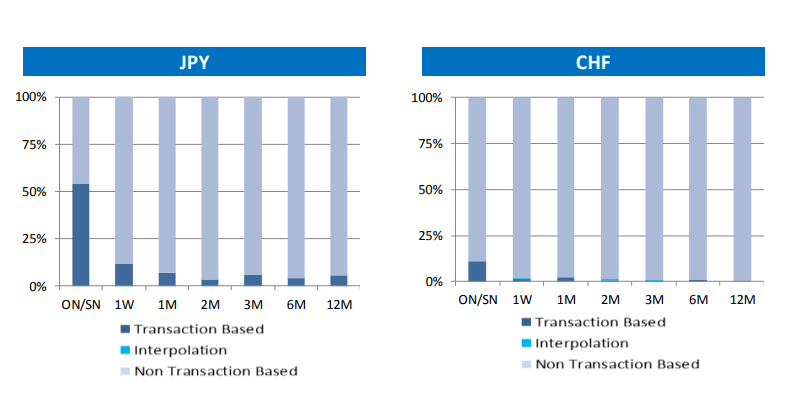

These charts suggest that LIBOR would not be published for some days and tenors if it were solely based on transactions in the underlying. The charts for CHF and JPY highlight this in particular:

Showing;

Showing;

- Most LIBOR submissions are not based on transactions for CHF and JPY.

- This raises the question of what should be published?

The LIBOR Waterfall

To account for the potential lack of transactions, ICE have suggested three methodologies that form a “waterfall”. My understanding is that banks will have three ways to submit LIBOR, but they must only revert to method 2 if method 1 isn’t possible that day (and method 3 if 1 and 2 are not possible).

The waterfall that is being proposed is defined by the “LIBOR Output Statement” here:

- 1. Transactions. Banks submit trades done in the past 24 hours and the volume weighted average price is calculated. Trades with trade date of today carry a higher weighting in the calculation than trades done yesterday.

- 2. Derived Rates. If no trades were done in the past 24 hours, I can use historic trades plus the movement in an underlying rate (e.g. OIS swap rates) to evidence where I think trades would have taken place. I cannot use this methodology every day however – only 3 days in a row for short tenors, and up to 15 days in a row for e.g. 12 month CHF. Equally, I could apply a parallel shift to e.g. 6 month tenors based on how much the 3 month has moved, or interpolate the tenor based on actual trades in adjacent maturities.

- 3. Expert Judgement. The ultimate fallback is to effectively revert back to the underlying survey question. “Where is Libor”?

As I understand the methodology, the waterfall results in a single LIBOR submission per bank per tenor (per currency). The published LIBOR rate for that tenor will be the trimmed mean of the bank submissions. What I mean by this is that I believe that the VWAP is calculated per bank, not across the whole market.

What Transactions?

If we fast-forward to a perfect world, then methods 2 and 3 will be rarely used. So what types of transactions will be included in the VWAP calculation? The ICE documentation states:

Transactions in unsecured deposits and primary issuance of commercial paper and certificates of deposit versus eligible counterparties, including:

- Banks

- Central banks

- Governmental entities

- Multilateral development banks

- non-bank financial institutions

- sovereign wealth funds

- supranationals, and

- corporations for maturities longer than 35 days.

Remember the wobble we had in Euribor futures last year when the panel decided to cancel/postpone the reform efforts? The market seems to think that transitioning to a transaction-based LIBOR covering such a wide range of counterparties will generally lead to lower rates.

Old vs New

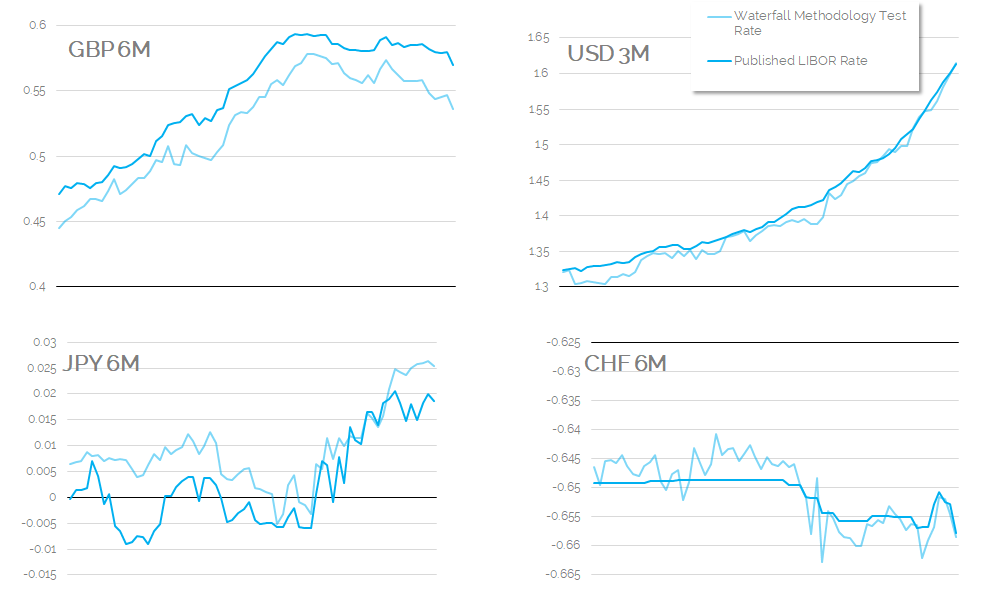

Fortunately, in this very transparent space, we don’t need to rely upon what the market thinks may happen to LIBOR. ICE have published the results for Q4 2017 where they ran both methodologies in parallel – i.e. the published rate was still based on the survey question, and they also calculated the rate using the new waterfall methodology.

The results? Given our focus on Swaps data, I’ve looked at the four LIBOR tenors mainly traded in IRS markets:

Complete data is available from ICE here.

My comments:

- GBP 6m LIBOR would have been consistently lower using the waterfall. Bravo market!

- USD 3m LIBOR sees very little change, although the move higher via the waterfall methodology was not as “smooth”.

- JPY 6m LIBOR saw some large differences, but then seemed to converge. Weird.

- CHF 6m LIBOR would be a lot more volatile using the waterfall methodology. Interestingly, the SNB still use LIBOR to target monetary policy, so I wonder what their thoughts on a more volatile rate are?

Trying to tie these charts back to the original ICE paper, it looks like LIBORs which are based mainly on expert judgement (rather than transactions) will see more volatile rates under the new waterfall methodology. I really should go back and calculate the realised volatility to be sure.

New RFRs

There is a push to transition away from LIBOR for new derivatives traded. The SOFR rate is now being published, but unfortunately has experienced a small hiccup in its’ early days. Fortunately, we’ve not yet seen any swaps vs SOFR reported to the SDRs. I guess we’ll need to wait for the CCPs to get involved first?

Unfortunately, Europe remains a long way behind. We’ll revisit Euribor reform in due course, but I did notice in the MIFID data this week that some CHF TOIS swaps have been reported. TOIS?! Really! It doesn’t even exist anymore. MIFID data remains a weak spot in the global push towards transparency.

In Summary

- LIBOR is currently survey based.

- ICE are planning to change this to a new waterfall methodology for calculations.

- This will allow LIBOR to be rooted in transctions where possible.

- ICE have made data available to compare the “new” and “old” fixings.

From my research, the only thing I haven’t been able to work out is when the methodology will change. Answers in the comments section below if you know please!

A very good write up on the most talked about topic. Thank you for sharing. The open question still remains -when will the change take place? Also, I wonder how comfortable people would be to use these different methodologies! Libor has been so prevalent with its old way of working that its almost a “who moved my cheese” moment whenever the change takes place !