Major markets across our industry are looking to transition (some) liquidity away from Libor-based products and towards Risk Free Rates. We’ve variously looked at Libor Reform, Euribor, SONIA and SARON but so far have not done a deep dive into new RFRs in the US.

SOFR – What is it?

As we reported in our review on Libor Reform, the US ARRC (Alternative Reference Rates Committee) identified a “broad Treasuries repo refinancing rate” as their preferred Risk Free Rate. Now known as SOFR (the Secured Overnight Financing Rate), it has been officially published since early April 2018. It is an overnight interest rate, calculated using actual transactions in repurchase agreements versus US Treasuries.

As a preferred Risk Free Rate, it is expected that some trading liquidity of interest rate derivatives will transition to SOFR-based contracts as we move away from a LIBOR-dominated world.

In the words of ARRC:

The ARRC accomplished its first set of objectives and has identified the Secured Overnight Financing Rate (SOFR) as the rate that represents best practice for use in certain new U.S. dollar derivatives and other financial contracts.

SOFR is published and administered by the Federal Reserve Bank of New York (FRBNY, or New York Fed to you and I).

Included Transactions

The SOFR rate is calculated using a very broad spectrum of repo trades (repurchase agreements).

Generally, a repo trade means that Counterparty One lends a bond to Counterparty Two in exchange for cash. For the purposes of the SOFR fixing, the maturity of these repo trades is overnight. Therefore, on the following day, Counterparty One receives the bonds back and Counterparty Two receives their cash back (plus or minus interest).

The SOFR fix includes all “flavours” of Repo trades:

- GCF Repo Transactions – A repo trade may be done versus a “basket” of bonds, where the person lending cash doesn’t necessarily know (or care) what bond they get in return. These are repos versus “General Collateral” (i.e. the specific securities provided as collateral are not identified at the point of trade execution). “GCF Repos” are specifically cleared through the FICC’s GCF repo service (as opposed to the FICC DvP service – see below).

- Repos cleared through the FICC DvP repo service (FICC = Fixed Income Clearing Corporation, which I think is part of DTCC, and DvP = delivery versus payment). These “cleared repos” are versus specific securities, rather than versus “GC”.

- All tri-party repos transacted with Bank of New York Mellon (BoNY) as the third-party – i.e. even if not cleared by any part of FICC.

The rates on all of these repo trades are used to calculate the fix except for FICC DvP trades that have rates falling below the 25th percentile of the whole FICC DvP data each day. These are deemed to be too “special” and hence excluded from the calculation.

(Note: Bonds that are “special” may see repo trades executed at rates below those for general collateral repos if cash providers are willing to accept a lesser return on their cash in order to obtain that particular bond. That’s the law of supply and demand if a particular bond is scarce for whatever reason – think futures rolls, one large holder who does not participate in repo markets etc).

Data Sources

The New York Fed is the administrator of the SOFR fixing and publishes it each day on the website here. However, it is not the NY Fed (FRBNY) that generates the transaction level data itself. The transactions are sourced from different places:

- BoNY – the Bank of New York provides transaction level tri-party data to the NY Fed.

- DTCC – I guess transaction level data is provided for all GCF Repos to the NY Fed.

- FICC – (part of DTCC) I guess DTCC provides the trade level details to the NY Fed for all repos done DvP as well.

That’s a lot of reliance on the DTCC. I’m a bit surprised that DTCC are not therefore the administrator of this rate…..although it is common amongst other markets to see regulators stepping into that role (Australia, Japan, UK).

Calculating the fixing

The fixing is the “volume-weighted median”. According to the NY Fed:

“a volume-weighted median approach.., compared to a volume-weighted mean approach, is more robust to erroneous data and outliers and more frequently reflects a transacted rate.”

What does this mean? It’s a three step methodology;

- We order the transactions from lowest to highest RATE.

- We take the cumulative sum of volumes of all of these transactions.

- We identify the rate at which the trades at the 50th percentile of dollar volume were transacted.

As well as publishing the 50th percentile rate (which is the fixing), the FRBNY website also includes the 1st percentile (i.e. lowest, and probably where the cut off for the FICC DvP “specials” inclusion is), the 25th percentile (which is NOT the aforementioned exclusion rate for FICC DvP trades), plus the 75th and 99th percentiles.

It is also possible for the NY Fed to use “expert judgement” to exclude trades from the calculation. I guess that helps with mis-booked trades as there doesn’t seem to be any automatic filtering of trades done at a level too high?

The rate is published on the FRBNY website by 8am Eastern Time the following day.

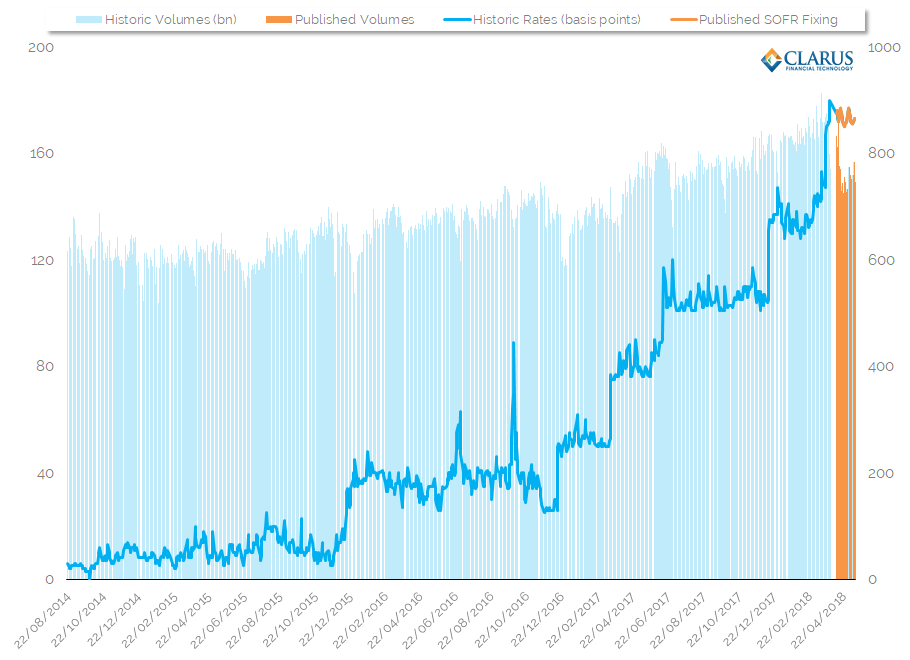

The SOFR Fixing

A theoretical history since 2014 is available on the FRBNY website, including the published SOFR fixings since April 2018. This is a great level of transparency:

Showing;

- Both volumes (bars) and rates (line chart) are available all the way back to 2014.

- Volumes for SOFR have been stable and have increased somewhat during that time period.

- With volumes approaching $800bn per day, you can see why this was a compelling index to choose as a Risk Free Rate.

- The published volumes (in orange) have been a little lower than the historic volumes reported up to the end of March. This seems to be because DTCC provided forward starting Repos in the data-set – see announcement here from the NY Fed.

In Summary

We have a new, transparent fixing to get to grips with in the US. If we were armed with the transaction level details (I wonder if DTCC make these available commercially?), we could replicate the fixing.

I wonder if the new SFTR (Securities Financing Transactions Reporting) in Europe will allow us to mirror these calculations? I fear not, as it appears these trades are being sent to the blackholes of transparency known as European Trade Repositories. The best we can probably hope for is some aggregated statistics, not the trade-level details that are actually useful.

- SOFR is a transaction based fixing, using repos versus US Treasuries.

- It is an overnight rate.

- Included transactions are GCF Repos and DvP repos cleared at FICC, part of DTCC.

- As well as tri-party repos with BoNY as the third-party.

- Volumes used to calculate the fixing can be as high as $800bn.

- We look forward to seeing the first swaps trading.

- No SOFR trades have so far been reported to US SDRs.

- CME have launched SOFR contracts.

- We are tracking daily volumes of these in CCPView and SEFView.