I think ESMA has got it wrong when it comes to Pre-Trade Credit Checking / Certainty of Clearing.

For starters, Pre-Trade credit checking is discussed under chapter 9 “Post-Trading issues” of both ESMA documents (consultation paper and draft RTS). I can see how it happened: the post-trading issue is that the clearing house does not accept the trade.

It’s like saying lung cancer is an elderly problem. Yes, that’s when the problem manifests itself, but it can be solved with behavior changes in the prior 60 years of one’s life.

TREE KILLERS

You’d have to get through 636 pages of the (645 page total) consultation paper before you even get to the topic of clearing certainty. And then within the proposed RTS Annex B you need to get through another 509 pages.

ISSUE SUMMARY

The paper and its annex, dated 19 December 2014, relates largely to feedback from the May 2014 Discussion Paper. I’ll try to summarize what I glean as the proposals:

Overall:

- Regulated markets (referred to as “venues”, ala US “SEFs”) need to have all of their consummated transactions cleared

Certainty of Clearing:

- To avoid a failure of clearing, there needs to be a pre-execution credit check

- The clearing member would provide credit limits for all of their clients to the venue (and periodically update them)

- The venue would do the credit checking

- For trades that fail to clear:

- If dealt on a venue and mandatory cleared, ESMA wants the trade to be void (seems to be equivalent to DFA void ab initio).

- If dealt on a venue and not mandatory cleared, ESMA wants the venue to have a rule which could involve the venue calculating the breakage cost.

- If not dealt on a venue and mandatory cleared, counterparties figure it out.

- ESMA only allows re-submission when failure is due to a technical problem, and the trade is re-submitted within 10 seconds.

Venue-related Timeframes:

- Venues have 1 minute to do a credit check of electronic, mandatory trades

- Venues have 10 minutes to do a credit check of non-electronic (and I glean also electronic but clearable, non-mandatory cleared trades)

- Venues have 10 seconds to send electronically-executed trades for clearing

- Venues have 10 minutes to send non-electronic trades for clearing

- CCPs have 10 seconds to accept venue-executed trades

Bilaterally executed Timeframes:

- Clearing Members have 30 minutes to send bilateral, mandatory-cleared trades to the CCP (I admit I haven’t read all 1200+ pages, but is a “bilateral, mandatory-cleared trade” mean it is above a venue-block threshold and hence can be dealt bilaterally?)

- CCPs have 60 seconds to correspond with the Clearing Member on credit checks

- Clearing members have 60 seconds to accept or reject

- The Consultation paper had language for Clearing Members to ensure trades are sent for clearing “as quickly as technologically practicable”, similar to Dodd Frank in America (where this means 10 seconds). However I can’t find that language in RTS, it seems they have managed to quantify everything.

SO WHAT’S WRONG WITH ALL OF THIS

Largely, ESMA has seemed to copy much of what was eventually settled upon with DFA, but they have done a better job at acknowledging the different execution methods up front and quantifying the timeframes better than “do it quickly”. (No offense, but they’ve had 2 extra years).

However I do have a problem with the pre-deal credit checking mantra which seems to state:

- Clearing firms carve out limits to each venue

- Venue’s do the credit checking

This notion of venues doing credit checking irks me. We are so hyper-critical of clearing firms and their extension of credit, yet we proceed to tell them to outsource that exact function to a trading venue.

The model of “Carve up your limits and send it to every venue” has, in my opinion, the following problems:

- Clearing firms are exposed to the initial margin (and uncollected variation margin). Initial margin is a portfolio measure and hence cannot be computed by a venue for a client. So venues use notional or DV01 measures as a proxy.

- As such, asking Clearing Firms to carve up credit requires an imperfect science of translating real limits they manage (margin) to notional and DV01. This requires many assumptions, for example assume every trade will be risk-increasing.

- A viable “solution” to the imperfect science is to just be horrifically conservative in the limits carved out (for example assume full notional). However this then:

- Negatively impacts the Clearing Firm as they are not able to extend their designed amount of credit

- Negatively impacts the Clients, as their limit is bifurcated across multiple venues, reducing their ability to reliably execute large size.

- What happens when a venue has a problem with credit checking? A failure is one thing, but what about a silent error? Errors happen, and if I am a Clearing Firm, I’d at least want to be the one making the error (and have the power to address it).

- Add all of the above into a blender at a time of stress (when it really matters). Now what have you got?

THIS IS 2015 (JUST ASK)

Carving out limits is nothing new, and I get it – it’s been used successfully in others markets in the past. However I would argue that it’s been used in a more credit-additive, higher paced market. Borrowing Commissioner Giancarlo’s terminology, liquidity in the swaps market is more “episodic” in nature and does not lend itself to this framework. I would venture to guess that if a single Clearing Firm saw 500 trades in one day, it would be massive. I might even go as far to say that many of the firms (outside of the big few) would be happy with 500 trades in a month! So why behave and write rules as if we’re catering for thousands order executions per second?

This is 2015. Technology has moved greatly. The better solution is for Clearing Firms to maintain their own credit limits, and require the venue, for every order/trade request: Just ask.

If a client places an order, the venue should simply needy to inform and request credit from the Clearing Firm. Conceptually this is the “Ping” method that I am referring to, that Amir wrote about in this article a while back.

Technologically, this is no different to the clearing credit checks that happen today already for bilaterally-executed trades, between the CCP and the Clearing Firm. RTS acknowledges that this is already an automated process.

BUT ITS GOTTA BE QUICK

I fear that much of the rule-writing of credit checks is premised on the false notion that a portfolio-based measure takes a long time to compute. However, there are clearing firms and vendor technologies today that are already handling this (of course Clarus is one of them). Whether a Clearing Firm has built the connectivity to each venue, or leveraged Traiana CreditLink (aka “Hub”) to streamline the process – the fact is that credit checks can be done in sub-second.

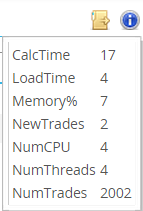

Take the example to the right. On a client portfolio with 2,000 trades, I can hit the CHARM margin engine over an API with 2 proposed trades and get a response back in 17 milliseconds. And this includes sending/receiving information over the WAN, so this is before we even begin talking about colocation, etc. And of course this is a portfolio measure, so taking into consideration all 2,002 trades.

SUMMARY

I feel that ESMA is being overly prescriptive in their RTS guidelines for credit checking. They have the premise correct: there must be pre-deal credit checks. However prescribing carve-outs is excessive, outdated, and would seem to be a contributor to systemic risk when the system is stressed.

Even if the RTS can be interpreted as guidelines which allow for ping-credit checks to take place, it is important to stress that technology exists and is in use today that accomplishes the basic goal. For those firms that lack the technology today, let’s not give them a development build for carving out venue-based limits. Rather they should be encouraged to deploy a technology that serves to build their own holistic risk framework where they are accountable and in control of their destiny.

NOTA BENE

In reading (portions of) the ESMA documents, I found myself questioning what is to come of the principal clearing model in Europe. My reading of the literature led me to believe, as is the case in the American Agency model, that the Clearing Firm is foreseen to only hear about the trade AFTER the trade has been cleared. After all, the trade will have been credit checked at the venue, so why bother asking again? The clearing member give-up has long been a pillar of the principal model – so as this gets thrown away, are there further changes to the operations and legality of the European clearing model? I solicited opinions from a select handful of participants, and I am glad to report…. nobody knew. Perhaps they had read less of it than I had.