I last looked at this in Oct 2015 in my article MiFID II and the Trading Obligation for Derivatives and now that a year has passed there is a new ESMA Consultation. The accompanying discussion paper is here and in this article I will review the key elements of the consultation.

Background

Once a class of derivatives has been mandated as subject to the clearing obligation under EMIR, ESMA is required to determine whether those derivatives (or a sub-set of them) should be subject to the trading obligation, meaning they can only be traded on a regulated market (RM), MTF, OTF or a third-country trading venue deemed to be equivalent by the Commission.

Trading Obligation in Other Jurisdictions

The discussion paper provides a good overview of the status of the Trading Obligation for Derivatives in Other Jurisdictions and lists the US, Japan, Switzerland, Mexico, Argentina and China as having enacted legislation to mandate trading through a specific facility for interest rate derivatives that meet certain characteristics.

It then lists for each jurisdiction the specific characteristics of derivatives that are currently subject to a trading obligation or will be in future.

Given the global liquidity pool for Derivatives, the CFTC tables are of particular relevance to Europe.

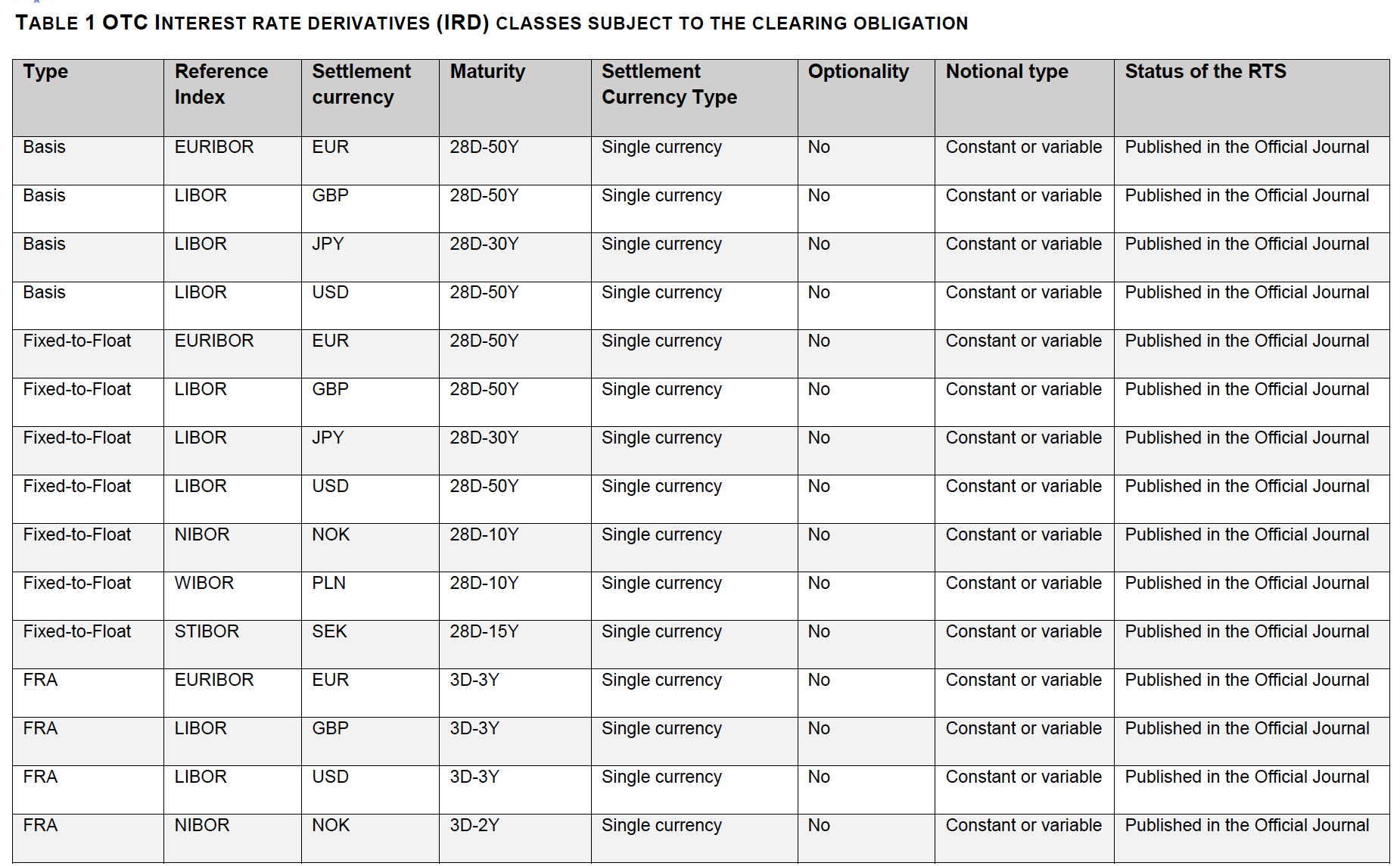

Clearing Obligation in Europe

As a Trading Obligation is only possible for a class of derivative subject to a Clearing Obligation, the paper then provides an overview of this under EMIR and I have extracted the tables below.

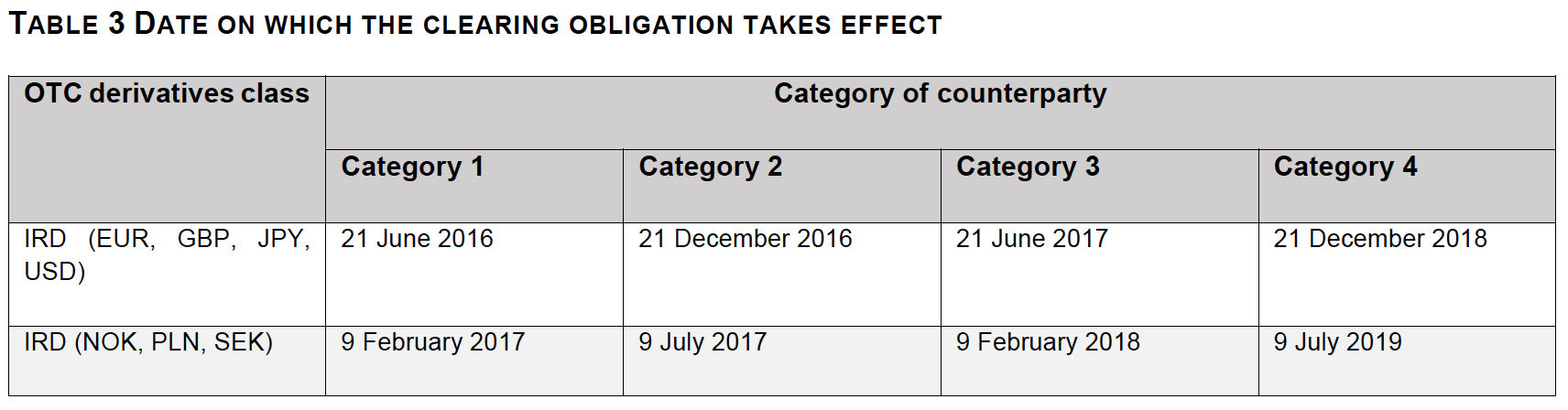

And as importantly the applicable dates.

Liquidity Assessment Overview

There then follows an overview of the Liquidity Assessment criteria:

- the average frequency of trades over a range of market conditions;

- the average size of trades over a range of market conditions;

- the number and type of active market participants; and

- the average size of spreads.

And an interesting discussion on ensuring consistency between the transparency regime and the trading obligation. ESMA considers applying the same or similar dynamic yearly liquidity test for the transparency regime to the trading obligation but assess that it is does not have the legal empowerment to do so and proposes a static approach specifying those classes of derivatives that were sufficiently liquid at the time of carrying out the liquidity assessment for the trading obligation.

Liquidity Analysis – preliminary analysis

There then follows the key part of the document; details of the preliminary analysis of liquidity based on transaction level data reported to European Trade Repositories as provided in daily activity reports.

The dataset used covers a time period from 01/07/2015 to 31/12/2015 and includes the classes of derivatives that are subject to the clearing obligation, i.e. basis interest rate swaps, fixed-to-float interest rate swaps, forward rate agreements (FRAs) and overnight indexed swaps (OIS) and chosen CDS indices but covers contracts on all maturities and all currencies. It does however differentiate between those currently subject to the clearing obligation and other contracts/currencies.

In April 2014, I looked at EMIR Trade Reporting and Public Data and came to the conclusion that there was little of value in this data and more than two years later, I have not seen any evidence to change my opinion. 🙁

ESMA however has access to the private data reported to European Trade Repositories and so has a much deeper insight; lets see what it gleaned from this data.

OTC Only

ESMA notes that analysis is based on OTC data only (based on transactions which have as venue of execution ‘XXXX’ or ‘XOFF’) and does not include transactions executed on Registered Markets (RMs) as the trading obligation will apply only to OTC-derivatives. ESMA then states that, the assessment of liquidity may not cover all transactions in a particular derivative or class of derivatives.

This is worrying paragraph in itself as it seems to imply that trades executed on existing MTF platforms operated by the IDBs are excluded from the dataset. Surely not as that would make no sense!

Duplicative reporting of Cleared Trades

ESMA then notes the following;

Under EMIR, a bilateral trade that is subsequently cleared can be reported several times, each time under a new Trade ID. As an illustration, a bilateral trade between a Counterparty 1 (CT1) and Counterparty 2 (CT2), both within the EEA, which is subsequently cleared, can be reported several times with several trade IDs that cannot be easily matched. It could be reported first as a bilateral trade between CT1 and CT2, and then as two cleared trades, one between CT1 and its CCP and one between CT2 and its CCP, with both sides of the trades reporting in each case. This can be further complicated when counterparties use the services of clearing members, thus adding further reports to the dataset.

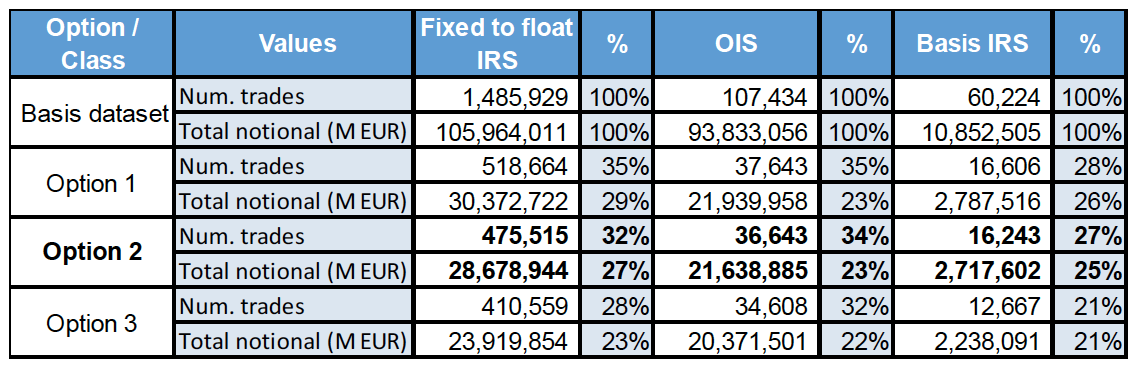

And then explores three options to exclude duplicate trades. I won’t bore you with the details but the resulting trade populations are certainly of interest.

So for example starting with a base dataset of 1,485,929 IRS, under Option 2 we are left with 475,515 or 32% of the population.

ESMA then choses Option 2 because it removes a number of records that is in between Option 1 and 3 and allows a more precise data selection.

Now all this causes alarm bells to start ringing and I wonder does it make sense to apply liquidity assessment tests like the average notional per day when our dataset may be significantly lower or higher than reality?

Is there a control dataset we can use to know whether the above trade counts are reasonable?

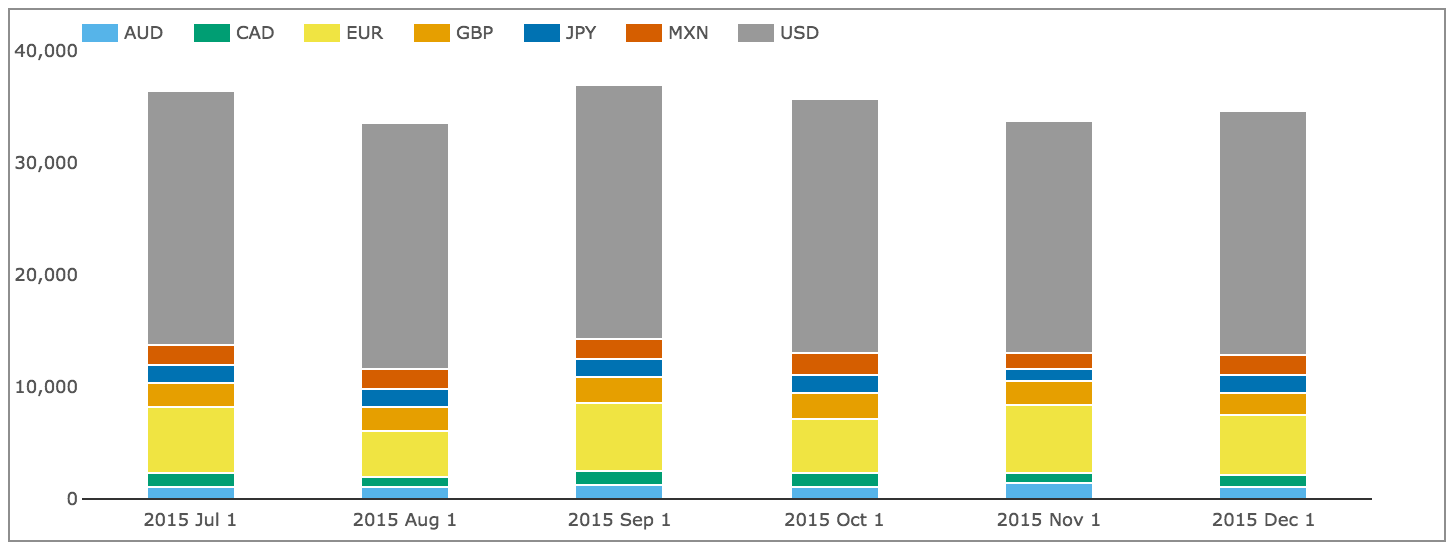

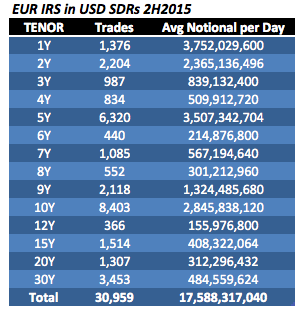

Lets try US Trade Repository data on the assumption that the US and EU Swap markets are comparable in size.

Using SDRView for the same six month period and the largest 7 IRS currencies, cleared and price forming trades only, we see the following:

An average of 35,000 trades a month, while other currencies only add 1,500 to this number.

Meaning that in the US, there were 220,000 trades reported in the same six month period that ESMA’s Option 2 dataset has 475,515 trades.

Anecdotally we would expect the EU market to be a bit larger than the US, but not more than twice as large. This leads me to doubt that the options considered by ESMA have been able to sufficiently filter the TR data appropriately, most likely due to the quality and assumptions in the daily activity reports themselves.

Tenors of Trades

ESMA then discuss computing tenors as the difference between the maturity and execution dates, and represent thus the time remaining to maturity at the outset of the contract. And present a table showing that 50% of trades are within +/- 10-days of benchmark tenors.

The flaw in this is that fact that many swaps are forward start, which are not distinguished from spot starting, so a 5Y into 5Y forward would end up in a 10Y tenor. This approach is carried down into the liquidity assessment by tenor further muddying the figures for liquidity in a vanilla swap for a benchmark tenor. The issue seems to be that the start date of the swap is not available in the TR data or at lease nto in the daily activity reports.

We know from US SDR data that Forward Start Swaps represent roughly 20% of the overall volume in USD IRS.

Types of Swaps and Packages

ESMA then go on to state that TR data does not provide sufficient information on a number of further specifications for the purpose of the trading obligation. For instance, TR data does not provide information on payment frequency, reset frequency, day count convention, and trade start type. ESMA is therefore interested in stakeholders’ view on possible sources for obtaining the necessary information on the most common terms for the classes shown as well as proposals on which specifications are considered necessary to specify the TO.

Well, the types of Swaps are crucial to understand liquidity and the information on the conventions are necessary to distinguish types of Swaps. Standard Swaps trade with respect to a specific Index (e.g. Euribor, Libor) and Tenor as well as specific conventions on payment frequency, day count and calendars. Such Swaps are well traded and likely to be liquid, while Swaps with non-standard terms are less likely to be liquid.

The CFTC MAT table distinguishes between Spot starting par swaps, IMM Swaps, MAC Swaps, none of which has been possible for ESMA to do with TR data.

Then we have Packages for which the CFTC provided phased exemptions.

EU TR data provides little or no insight into this but we know that packages are common and broadly there are two types; ones where each leg is a Swap (e.g. Curve Spreads and Butterflies) and ones where one leg is a Swap (e.g. Invoice Spreads and Asset Swaps).

ESMA simply asks for respondents views on package types and whether they are standardised and sufficiently liquid.

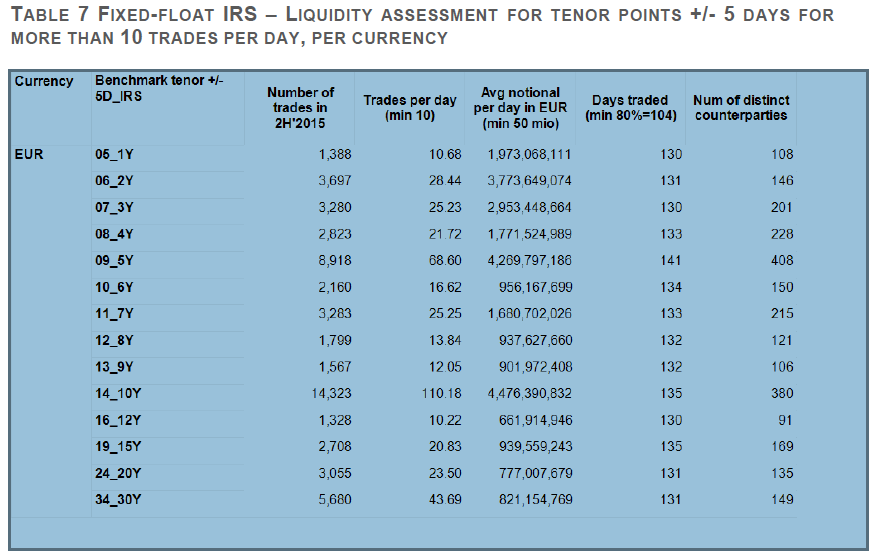

Results of ESMA’s Analysis

Next ESMA presents the results of its analysis on which products should be subject to the Trading Obligation.

Points to note on this are:

- Does not distinguish types of Swaps (e.g Spot or Forward) and conventions of Swaps (Index, Tenor, etc.)

- 1Y, 8Y, 9Y, 12Y have a much lower number of trades than the other tenors

- Checking the CFTC MAT tables we find that these tenors are not MAT

Again we need a control dataset to know whether the above is reasonable.

So lets turn again to SDRView on the assumption that EUR IRS traded by US persons are likely to be a fraction of the European, most likely less than half. The table below shows this data.

Comparing the two datasets:

- It is surprising that the ESMA counts and notionals are not much higher

- e.g. for 5Y SDRView has 6,320 trades while ESMA has 8,918.

- USD SDR data lends credence to the ESMA finding that 1Y and 9Y may be liquid enough

- But it does not support the ESMA finding on 8Y and 12Y

However the fact remains that in this case the ESMA numbers look lower compared to SDRView than I would expect. And the Sum of the ESMA EUR trade counts also looks a much smaller fraction of the overall IRS total in Option 2 of 475,515; a number I would expect to be dominated by EUR IRS in benchmark tenors.

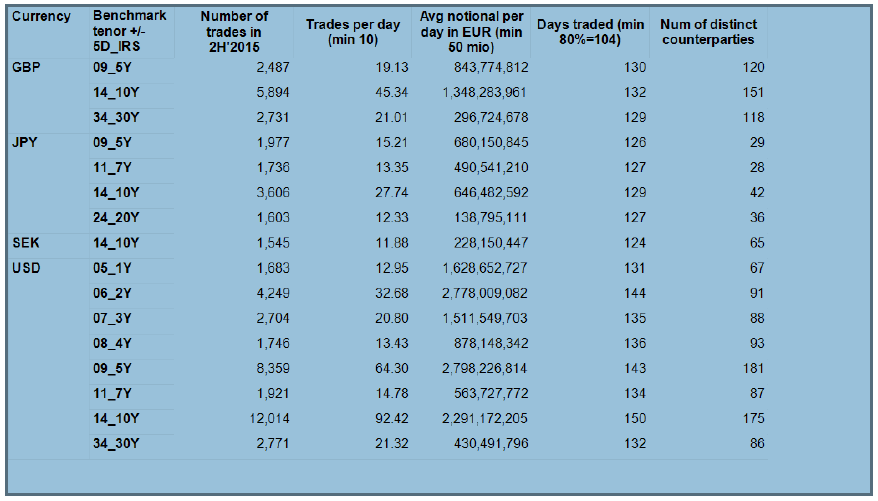

There are further ESMA tables for GBP, JPY, SEK & USD.

Notes on this:

- GBP only has 5Y, 10Y, 30Y as sufficiently liquid

- Contrast this with CFTC MAT which has 2Y, 3Y, 4Y, 5Y, 6Y, 7Y, 10Y, 15Y, 20Y, 30Y

- SDRView data shows that 1Y, 2Y, 3Y, 15Y should be considered

- JPY has 5Y, 7Y, 10Y, 20Y as sufficiently liquid

- CFTC does not have a MAT in place for JPY IRS

- Japan has 5Y, 7Y, 10Y as MAT

- SEK is not mandatory in any jurisdiction

- USD has 1Y as sufficiently liquid while it is not MAT for CFTC

- CFTC has 2Y, 3Y, 4Y, 5Y, 6Y, 7Y, 10Y, 12Y, 15Y, 20Y, 30Y

- SDRView data is higher than ESMA for USD IRS, as we would expect

- SDRView for 10Y has 34,876 trades while ESMA has 12,014

- SDRView for 7Y has 8,857 trades wile ESMA has 1,921

Moving swiftly on to other products.

Both Basis Interest Rate Swaps and Forward Rate Agreements (FRAs) have not met the criteria for the Trading Obligation.

While for CDS, ESMA states:

“TR data on CDS transactions does currently not allow ESMA to identify the underlying index. Therefore, ESMA could not carry out an initial liquidity assessment based on TR data. However, based on discussions with selected stakeholders, ESMA considers that the on-the-run series of both the iTraxx Europe Crossover index in EUR with 5Y tenor as well as the iTraxx Europe Main index in EUR with 5Y tenor can be considered sufficiently liquid. ESMA considers extending the TO to the first thirty working days of the 1st off-the-run-series, or the series that is immediately prior to the current on-the-run series.”

Really? Another body blow to the usefulness of EU TR data.

Lets wrap up the results analysis there.

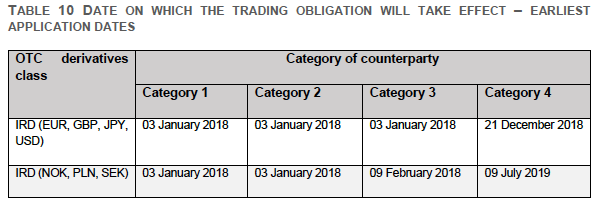

Deadlines

The crucial question is dates for the Trading Obligation to come into force, which the document shows:

![]()

So we are 15 months away from the first deadline and the last deadline is 18 months after that.

Final Thoughts

ESMA is consulting on the Trading Obligation for Derivatives.

ESMA’s analysis for this has used EU Trade Repository data.

This dataset has serious shortcomings.

It fails to distinguish between types of Interest Rate Swaps.

There are questions on the dataset being representative of the real world.

Our suggestion would be to not use EU TR data.

But look for other sources, e.g. Inter-Dealer Brokers and Clearing Houses.

Comments are due to ESMA by 21 November 2016.

I would encourage your firms to respond.

Derivatives trading is a global market, one with a global liquidity pool.

It needs regulations on trading obligations to be consistent between the EU, US and other jurisdictions.