Recently I noticed that the view statistics for my June 2014 blog on LCH-CME Switch Trades were running at 5 times their weekly average, which I thought was odd. Then on 15-May, I read the Risk article, Bank swap books suffer as CME-LCH basis explodes (subs required) and I understood why. So a good time to re-visit this topic.

First for the time pressed folks, a concise summary:

- Recently the price difference between the same USD Swap Cleared at LCH or CME has increased significantly

- Pay Fix is now up to 2bps lower at LCH (tenor dependent)

- Receive Fix is now up to 2bps higher at CME (tenor dependent)

- Supply and Demand of Rec vs Pay at CME has driven the change

- Economic theory tells us that price change should stabilise supply and demand

- However Liquidity is difficult to move or split

- Dealers have suffered losses resulting from the imperfect hedge between CME and LCH Swaps

- This has driven an increase in volumes of CCP Switch trades to hedge exposure

- More than $20 billion of these trades have traded since 30 April

- Tradition and ICAP are the stand-out leaders in CME-LCH Basis trades

Then for those of you interested in data and discussion; the detail.

Background

An Interest Rate Swap whether cleared at LCH or CME is economically the same instrument. There has been a small difference in the price of these Swaps, called the “basis” and referred to in the market as the CME-LCH Spread or the LCH/CME Basis. This basis has been small enough (0.15bps) to be inconsequential to most of the market.

However in recent weeks the CME-LCH Basis for USD IRS has risen significantly, exhibiting a term structure with values up to 2bps; much larger than the typical bid-offer spread of 0.25 bps. There are now reference pages provided by ICAP and Tradition, where market participants can see indicative basis spread values.

The CME-LCH basis increase has resulted in a rise in volumes of CME-LCH Switch trades, which allow firms to reduce their exposure to this basis. So if a firm has been hedging a CME Cleared Swap with an LCH Cleared Swap than that hedge has not performed as expected in the last few weeks as the spread has widened.

While some firms may have included the CME-LCH basis spread in their PL, we expect many will not have and just taken the Variation Margin statements from CME. This situation will now change and impact everyone as CME put out an Advisory Note on 13-May for CME OTC IRS USD Valuation Curves. This states that within 30-days CME specific swap observations will be incorporated into end-of-day curves.

Impact on Price Quotes

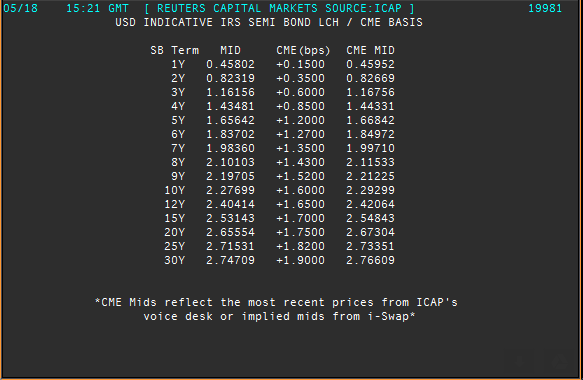

Lets first look at what the basis means for Swap prices by using the ICAP indicative quotes from Reuters 19981.

The Mid columns shows LCH Mids, then the CME Basis and then the resulting CME Mid.

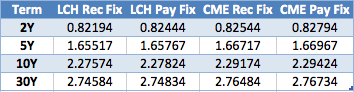

Lets assume a 0.25 bps Bid-Offer Spread for both LCH and CME and for all tenors and create a table of Bid Offers for the major tenors.

This shows that if we want to:

- Receive Fixed 30Y, we get 2.74584 at LCH or 2.76484 at CME

- Pay Fixed 30Y, we get 2.74834 at LCH or 2.76734 at CME.

Which may not sound large differences, but in-fact are very significant. For example the standard size on a USD 30Y IRS is $25 million and for this the difference in value is $95,000.

Meaning that if we want to:

- Pay Fixed, we should do this trade at LCH

- Rec Fixed, we should do this trade at CME

The only reasons for a firm not to do so, would be:

- only eligible to clear on one of CME or LCH (as a client or a member)

- lower risk and margin on our swaps portfolio at the other CCP, which compensates the worse price

- cross-margin benefits against futures position, which is only available at CME

- price difference is in-consequential on the trade (small size?)

- as a market maker, we need to provide a price to our client

Of these, I would think that 2 would not be common for an end-user but for a dealer is effectively the CCP Switch trade and 4 is less relevant, but the other three will be pertinent to many market participants.

Impact on Portfolios

Lets now look at the impact of the CME-LCH Basis on portfolios.

The first is that when CME move to using CME specific swap observations there will be a change in Variation Margin (VM) on that day, which will be a gain for some and a loss for others. The higher and steeper CME Swap Curve means that firms that are net receivers (particularly at long maturities) will have a negative impact on their PL.

However as moves of +2bps are well within the daily moves seen in the Swap market, this in itself would not be significant, were it not for the fact that there will be significant inter-dealer hedges on LCH for client-dealer swaps cleared at CME.

Meaning that the client-dealer trade will now move by up to +2bps, while the hedge trade will not, resulting in a likely loss (or gain?) for the dealer, which the Risk article puts at up to as much as a $20 million loss at each dealer(?).

More importantly it will now become necessary to actively mange this CME-LCH basis risk, either by not taking on the client trades that cause the risk or by hedging the basis risk, much like one hedges Libor 1m vs 3m Basis.

Assuming that saying no to clients is not palatable to market making firms then hedging basis risk becomes the only open path and this could act as a driver of increased volumes in CCP Switch trades; which is what has seemed to have happened. (More on volumes later).

The CCP Switch trade means that one Dealer on the trade is willing to pay away the basis in order to reduce exposure.

Using our earlier 30Y example this would mean this Dealer is willing to pay fixed on a CME Swap at 2.76734 and receive fixed on an LCH Swap at 2.74584. In effect losing the basis plus the bid-offer (unless transacted at mid), so 2.15 bps over the life of the deal. Or put another away around $100,000 on our $25m of 30Y and $1 million on a $250m 30Y! Also until CME change their curves, these deals would show a PV loss in that dealers book.

Reason for the Basis

Now lets turn to possible reasons for why the Basis has come about.

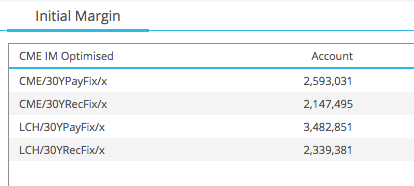

Starting with the margin models as an obvious place, we use CHARM to estimate the Initial margin for 30Y Swaps on CME and LCH.

This does show that CME Pay Fix requires much less margin than LCH Pay Fix, something we have noted before see CME IRS Margin Model Change. However that would the make the cost of holding a 30Y Pay Fixed Swap higher at LCH, even if only by 0.1 bps or so, which does not serve to explain why the CME Pay Fix rate should be higher.

So we must look else where for our explanation.

The one we hear most often and the one mentioned in the Risk article, I would put in my own words as follows:

- CME cleared volume is mostly driven by clients that are fixed income asset managers

- These clients generally look to swap the fixed coupons on their bond holdings into floating coupons via swaps

- Meaning they generally pay fixed on swaps

- So on the client-dealer swap trade, the dealer is receiving fixed

- To lay-off this risk the dealer generally looks for a dealer-to-dealer swap

- The dealer may hedge for a time with futures until the swap is found

- However he needs to pay fixed on a swap and find another dealer willing to receive fix

- When he finds that trade, he now has two offsetting trades in his house account

- Which means there is no interest rate risk and no margin requirement

- However as all/most dealers are in the same direction at CME, it is not easy to find the hedge trade

- Consequently the dealer does the hedge with another dealer at LCH

- Which means that there is interest rate risk and margin required at both CME and LCH

- Or put another way the difference between zero and two times gross margin

- Which for our 30Y $25m trade would be zero margin or $5.5 million of margin

- The cost to fund this margin and the capital cost are significant

- Somewhere between 0.50 bps and 1.5bps

- Which is the reason for the CME-LCH Basis

Sound plausible?

Without seeing the data to verify the assumptions, I cannot be sure.

But it does seem the best explanation.

It would also seem to explain why firms willing to Receive Fix at CME would get attractive and better rates than at LCH.

So a supply and demand argument, to which an economist would reply that prices will change until supply and demand are again balanced. That is indeed what we are seeing and perhaps this price change will result in more supply on the receive fixed side at CME.

However as an economist that also studies markets will tell you, liquidity also tends to be difficult to move or split. I am not aware of a major Futures contract on the same underlying that has volume split across two Exchanges.

(A recent JP Morgan US Fixed Income Strategy Note on May 1 2015, attempted to put an upper bound on the size of the CME-LCH Basis by looking at the financial benefits to clients from cross margin of Futures vs Swaps and came up with a 1.5 bps maximum. If you have access to that, I would encourage you to read.)

Volumes of CME-LCH Switch Trades

Continuing with the theme from the Impact on Portfolios section above, we know that the recent increase in the basis spread will have caused firms to limit their losses and exposure by looking to hedge this basis risk. Lets look at the numbers to see what the data shows.

Using SEFView we can look at the volumes published by the SEFs between 30 April and 15 May 2015 and then drill-down to the daily instrument volumes published by the SEFs to see whether they breakout CME from LCH volume.

Neither BBG or TW breakout their Swap volumes in this way, however that may not be important as we would expect Dealers to go to IDBs to do these trades.

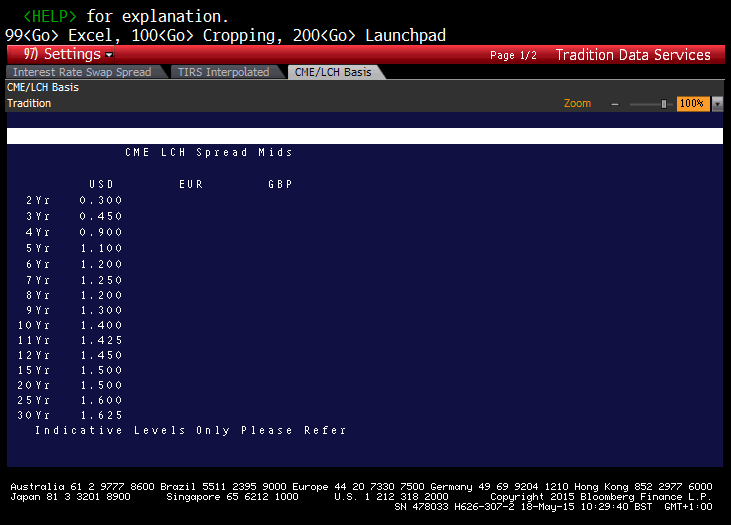

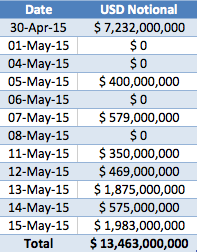

Tradition

Lets start with Tradition as we know they were early out of the gate with their CCP Position Switch Service, see their News from June 2014. Their CME LCH Spread reference page on Bloomberg is shown below.

Lets drill-down in SEFView on their numbers and sort by amount.

Showing that they do breakout CME volume, see the second line above, showing $4.7b of 5Y CME (on 30 April) and also $7b of 5Y LCH.

Now we do not know for sure whether all of this $4.7b is from CME-LCH Basis trades. We do know it is from 3 trades, which makes each $1.5 billion and so much larger than a standard market size trade of $70m, leading us to the conclusion that these are indeed CME-LCH Basis trades.

If we export all the daily volumes for Tradition and in Excel, sort by reporting date, tenor and amount, we can quickly find the pairs of CME and LCH volumes on the same day for the same tenor. Aggregating all this information gives us the following:

Now this is not 100% accurate as there must be some outright CME volume on Tradition, so the true figure is likely lower, but it should be ballpark.

So more than $10 billion traded over this 12 day period.

Three bigs days; 30 April with $7b, 13 May with $1.8b and 15 May with 1.9b.

Certainly much bigger volumes than I recall seeing in the past.

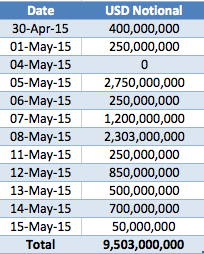

ICAP

Now onto IGDL and ICAP.

The bad news is that they do not breakout their CME cleared volumes in their SEF reporting.

The good news is that they have kindly agreed to share their volumes with us.

Again big numbers, almost $10 billion traded over the period, only one day out of twelve with no volume and two large days on 5 May with $2.7b and 8 May with $2.3b; the latter being particularly strong as a wide range of tenors.

And just a note on single counting vs double counting vs quadruple counting.

Both the ICAP and Tradition figures above are single-counted; meaning that if one $1 billion notional CME-LCH basis swap trade is agreed between two dealers, we call this $1 billion (single-counted). However this results in two $1 billion trades at CME (one in each dealers accounts) and two $1 billion trades at LCH (one in each account). So looking across CCPs we could say $ 2 billion of gross notional (double counting) and across CCP and account we may even say $4 billion gross notional (quadruple).

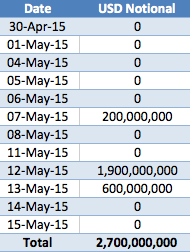

Tullets

Tullets do provide some breakout in their SEF reporting and we can follow a similar approach to that for Tradition, with the caveat that we are not aware that they have made public that they offer brokerage on CME-LCH Swaps. However given their position in the USD Swap market it is very likely that they have done some of these trades. Lets look at the data.

So hard to be sure but given the lumpy nature of the volume and the $1.9 billion on 12 May, you would imagine that some of this would be CME-LCH Basis.

BGC and GFI

The same approach for BGC reveals nothing in our date range but does show $500 million on CME cleared Swap on 14 April 2015. I have not had time to reach out to them (my bad).

GFI we know have done this trade before, see my old LCH-CME Switch Trade blog.

And the GFI data in SEFView shows $150 million of 7Y at CME and LCH on 13-May, plus some other CME volume but not with LCH on the same day, so that must be stand-alone CME Cleared Swaps.

The End

$20 billion of volume in 12 business days is pretty decent.

And certainly much higher than we have seen in prior periods.

It will be interesting to see whether the volume continues.

And indeed whether the basis moves.

Without volatility there is little volume.

And whether the basis will show in EUR too.

Even more fundamental, whether this is a decisive shift in the battle between CME and LCH.

A shift in which CCPs favour?

Only time and CCPView data will tell.

And the impact on client and dealer swap trading?

Only time and SDRView data will tell.

We live in interesting times indeed.

An alternate ending 🙂

The basis widened in the month of may,

20 billion of volume in 12 business days,

Will the basis move? will volume grow?

Without volatility it will surely be slow.

A shift in clearing venue, who is to know?

We’ll login to CCPView, for the truth it will show.

Client and dealer trading, what is the impact?

We’ll watch with SDRView, it reveals the facts.

Do we expect this basis in our regional CCP (i.e. Japan JSCC vs. LCH)?

We do expect a CCP Basis to become evident at some regional CCPs, though we have not looked specifically at JSCC in this context.