Guest Blog Series

Profile: Interest Rate Swaps trader. 12+ years’ experience, European and cross markets focused

We open this week with an age old adage – what applies to one market does not and should not be applied to another.

This applies across the board, but seems particularly apt in terms of trade reporting. Let’s make an example of Sterling markets and use the SDRView API to extract date for July 2014 for OIS, Cross Currency Basis and IRS markets.

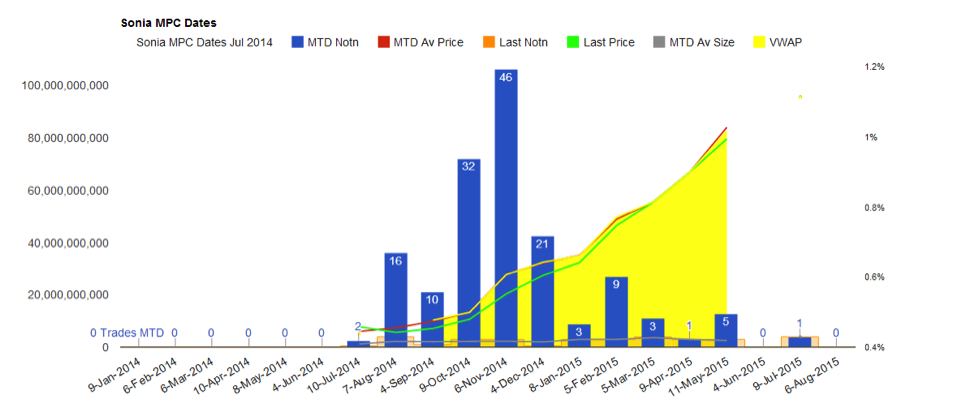

GBP OIS

First up, and following on from the Sonia blog a couple of weeks back – OIS:

We’ve intentionally crammed this graph FULL of data to highlight that a lot of different trade metrics are relevant across markets. You can’t get a full “flavour” for a market without considering at least:

- Trade count

- Trade notional volume (and subsequently translated into DV01)

- Average volume

- Average price

- Volume Weighted Average Price

- Last Price

- Last Volume

For something like MPC-dated SONIA trades, looking at notional traded is as equally instructive as my normal DV01-centred analysis. Big picture, we can immediately see that:

- November saw the highest volume of trades by both number and notional

- VWAP and simple average price are virtually the same for all tenors throughout the sample period (July 14). This highlights the homogeneous nature of the trades – trading in a tight range of sizes throughout the month.

- VWAP is consistently higher than the last trade, particularly evident for November. This suggests trading was concentrated towards the beginning of the month and prices have moved lower with smaller volumes going through. This fits well with our previous analysis of Sonia’s Mansion, when we looked at the impact of Governor Carney’s speech on GBP OIS activity.

- 66% of trades occur across just 3 meeting dates. Of course, this activity is centred around Inflation Report months, but also the fact Mr Carney highlighted rates may move this year. This concentration of liquidity highlights how difficult it is to run a short-end book. When providing prices on longer-dated structures – eg 2015 meeting dates – trader’s do not know where the liquidity is going to be centred. Add in the digital nature of OIS trading (+/- 25bp or unch) and it means liquidity only becomes available after the market has begun to move in price and attracted attention of end-users.

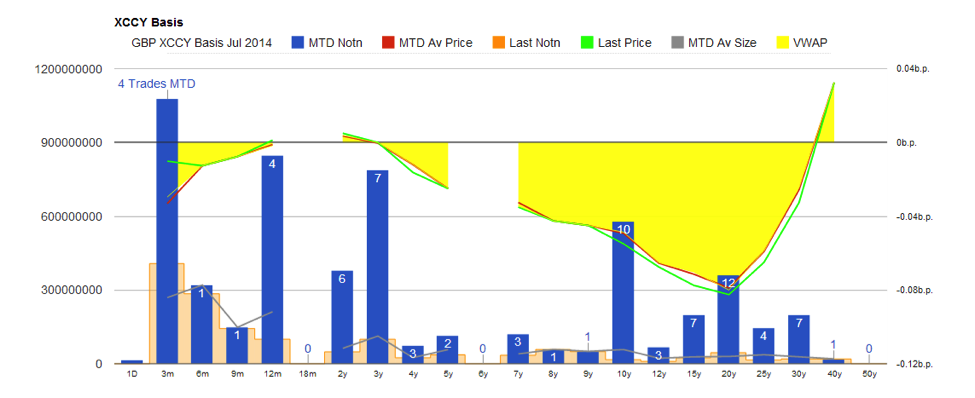

GBP CCS

From a market where liquidity becomes concentrated upon maturities that move the most, to a completely different beast – Cross Currency Basis Swaps. Just compare and contrast:

In summary:

- Discontinuities in liquidity exist – despite sampling a whole month’s worth of data, we fail to see a single 18 month or 6 year trade.

- Notionals are shown which is a little more misleading when comparing such disparate maturities. 20 years actually sees the highest risk-weighted activity.

- Last trade sizes and average trade sizes are almost identical – trading activity appears to be lethargic but at least consistent.

- Again, VWAP and simple average price are very similar – reinforcing the idea that cross currency basis is an asset-class that trades in well-defined “market” amounts.

- Last price is generally below the VWAP and average prices. With such a flow-driven structure and infrequent trades, this suggests that either receiving pressure entered the market at the end of the month, or that the main activity during the month (i.e. in 10 and 20y tenors) was a paying interest.

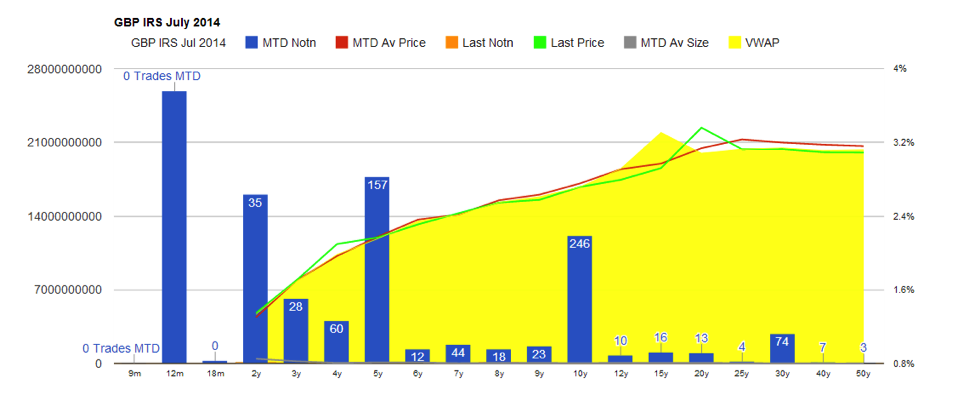

GBP IRS

Having looked at two minor markets, what now happens when we switch the analysis to the “typical” focus of trade reporting, vanilla IRS? GBP is one of the “super-major” currencies, therefore we expect to see a broad view of the market:

In reality, what we see is a far more distilled picture of the overall market:

- Last trade size and average trade size fall into insignificance compared to overall volumes through the month. Each individual trade therefore does not have such a price-forming impact

- As we continually highlight, benchmark tenors are few and far between. 2y, 5y and 10y are the key price-forming benchmarks.

- Despite a raft of”1 year” maturity trades, they were all forward starting, therefore price data about the short-end is extremely limited.

- Out of nearly 2000 trades reported, only 750 (38%) can be considered a true “price-forming” transaction – i.e. spot starting and vanilla. (Amir did a similar analysis for USD IRS back in May)

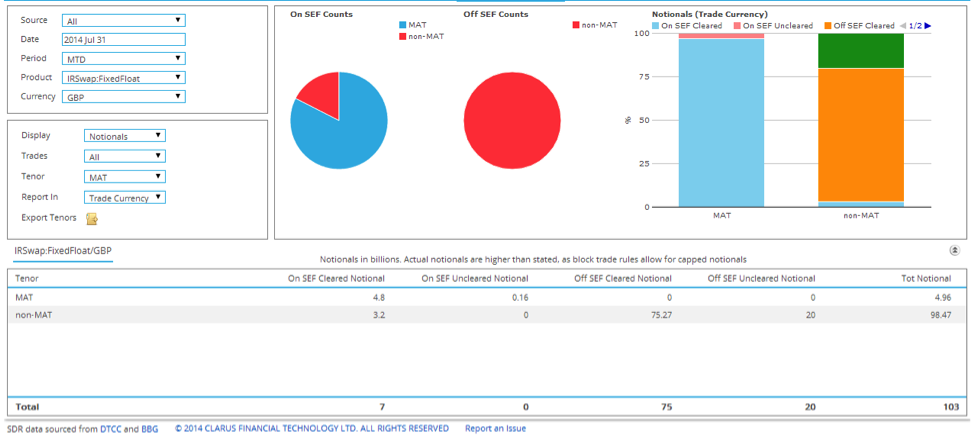

Only 38% are “vanilla” transactions! This is the fact I want to dwell upon. Looked at another way, what percentage of GBP IRS trades are “MAT-able”? Using SDRView Researcher, we see that not even 5% of trades by notional were MAT-able during July 2014:

Using SDRView Pro we can estimate why such a low volume of trades were considered “benchmark”. Of the near-2000 trades:

- 300 were IMM dated

- Nearly 700 were other forward starts

- Over 100 were broken tenors

- And of course US Persons are not that active in GBP – particularly when trading out of an Non-Guaranteed Affiliate

Conclusion

With the trade reporting data in “raw” form we therefore see that in the far less liquid markets, we are able to glean more information about price forming transactions. Ranking our three markets in July 2014 for transparency, we see the following:

- XCCY Basis – 64% (by number) of transactions are valid, vanilla price-forming transactions.

- GBP OIS – 58% (by number) are standardised MPC-dated, 1 month trades.

- GBP IRS – only 38% are pure vanilla.

This therefore creates a dichotomy in markets. The less-liquid, less traded markets are now more transparent and more readily accessible in terms of price discovery and trade activity than their “vanilla” pure-IRS equivalents.

Of course, there are reasons for this.

If you want vanilla exposure, trade a vanilla Rates instrument such as cash bonds or futures.

Equally, if you want leveraged positions, trade forwards in IRS space to minimise capital requirements – which are notional-based.

What is clear, however, is that understanding and accessing the granularity of the data for IRS is impossible by just looking at a list of trades.

This is one reason why the entrance of new market participants will be a key factor over the coming months.

We showed last week how market structure for USD Rates has not significantly changed since going electronic – and after this analysis, I feel it is unlikely to do so until we truly harness the power of the data.